How Quant Funds Make Billions From The 5% Of A Stock Everyone Else Throws Away

Strip the market and the sector out of a stock and the sliver that is left looks like static

That sliver is the only part worth trading, and an entire style of fund is built on keeping it

But before reading

Bookmark this article and follow me @L1vsun for more Info

I am Erel, Quant Finance Researcher and Developer. Sharing information that I have learned in all my experience and found myself from various sources. Open for collabs and promo, Dm me

Every day a stock makes a move, and almost none of that move is about the company. It is about the market going up or down, and about the sector it happens to sit in

Those two forces do most of the pushing, and everyone who owns the stock is really just holding those forces with the company's name printed on the outside

Underneath, there is a thin leftover that the forces do not explain. It looks like noise. Retail throws it away without ever noticing it was there. That leftover is where a whole class of quant fund makes its money.

The last article showed that 500 stocks are really a handful of hidden forces plus a cloud of randomness. This one is about that cloud

Because it is not randomness. It is the one part of a stock that is genuinely about that company and nothing else, and it behaves in a way the forces never do

Learn to see it, hedge everything else away, and you are left holding the only slice of the market that is actually predictable

1: The Part Of A Stock Nobody Bothers To Trade

Take any stock's return on a given day and split it into two pieces. The first piece is its exposure to the shared forces: the market tide, the sector rotation, the style factors from the last article. The second piece is whatever is left after you subtract all of that

Quants write it as the stock's return equals its factor exposures plus a leftover, and they call that leftover the residual, or the idiosyncratic return. It is the part of the move that the forces cannot account for.

Here is the thing nobody tells you about that residual. When you buy a stock, you think you are making a bet on the company

You are mostly not. You are buying the market, leveraged by that stock's beta, plus a side bet on its sector, and only on top of all that a small wager on the company itself

The company-specific part, the earnings surprise, the block a fund had to dump, the knee-jerk to a downgrade, is a thin sliver riding on a much bigger systematic wave

Call it five percent

The exact figure moves around by stock and by window, but the shape never changes: a big block everyone is really trading, and a faint idiosyncratic cap on top that looks like static

img

Now watch what happens to that sliver when you diversify. Own thirty names and the company-specific leftovers start cancelling each other out, one stock's good surprise against another's bad one, until the residuals wash to almost nothing and you are left holding pure forces

That is not a bug. That is literally what diversification does, and it is why your carefully spread book feels exactly like the market. You spent all that effort to delete the only part that was ever about the companies, and kept the one part that is just the market wearing thirty costumes.

Quant stat-arb funds run the whole thing in reverse. They hedge the forces out and keep the residuals in. Instead of a book that cancels the leftovers and holds the market, they build a book that cancels the market and holds a giant basket of leftovers

The reason they go to that trouble is simple, and it is the entire point of the strategy: the forces are close to unpredictable, but the leftover is not

2: Why The Leftover Snaps Back

The systematic part of a stock, the market and sector piece, is about as close to a random walk as anything in finance. If you could reliably say where the market goes tomorrow you would not be reading this

Direction on the big forces is brutally hard, which is why almost nobody beats the index by timing it. The residual is a different animal entirely, and the difference is the whole edge

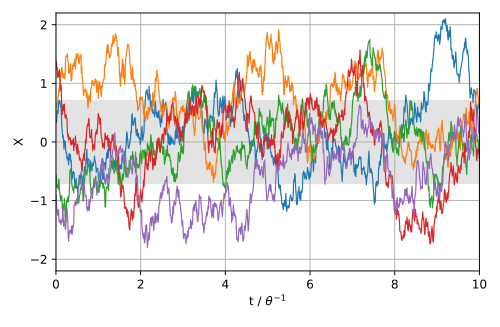

Once you have hedged the forces out, the leftover tends to be stationary. It wanders away from zero and then gets pulled back. The reason is human and mechanical, not mystical

A lot of what moves a single stock away from its factor-implied value is temporary: a fund unwinding a position and pushing the price past where it belongs, an overreaction to a headline, a buyer who simply had to be filled by the close

Those pressures fade, liquidity comes in against them, and the residual reverts. The forces do not revert like this because they are the aggregate of the whole market's information. A single name's idiosyncratic wobble is a local imbalance, and local imbalances get corrected.

Quants model that pull-back with an equation borrowed from physics, the Ornstein-Uhlenbeck process. It describes exactly this: a quantity that drifts randomly but is always tugged back toward a central value

Do not let the name scare you. It says the change in the residual each step is a spring pulling it toward its mean, plus some random jitter, and the strength of that spring is the only thing you really need to measure

The strength of the spring gives you the one number that matters, the half-life of the reversion, which is just how long it takes on average for half of a deviation to decay away

A residual with a five-day half-life that is stretched far from its mean today is a bet with a clock on it: the stretch is expected to close, and you know roughly how fast. To turn that into a signal quants standardize the deviation into what Avellaneda and Lee named the s-score, the residual's distance from its mean measured in its own standard deviations

When the s-score runs very positive the stock is rich against its own hedged fair value, so you short it. When it runs very negative the stock is cheap, so you go long. You close as the score comes back toward zero

A common rule opens a position past roughly 1.25 standard deviations and unwinds it near the middle. That standardized number, computed fresh across hundreds of names every day, is the machine

3: How To Actually Use This As A Trader

You are not going to run a stat-arb book from your kitchen. That is not the point. The point is that once you see a stock as forces plus a mean-reverting leftover, the whole game changes shape, and three things fall out of it.

First, the trade is market-neutral by construction, and that is a feature, not a limitation

You hold the stock against its factor exposures, so if the market rips or crashes you do not care, because both sides move together and cancel

What is left uncovered is only the residual, and the residual is the thing you actually have an opinion on. This is the pairs trade from the last article grown all the way up

A classic pair hedges one stock against one partner and prays the partner keeps behaving. Here you hedge one stock against the entire latent structure of the market and bet only on its own leftover snapping back

Same instinct, far more robust, because there is no single fragile partner to break

Second, the edge on any single one of these bets is tiny, and that is normal

You are not right ninety percent of the time. You are right a little more than half, the same thin statistical tilt that shows up everywhere in this world, and a single trade tells you almost nothing

The money is in scale and repetition: hundreds of these residual bets running at once, each one small, each one hedged, each sized so no single name can hurt you, the aggregate edge grinding out over thousands of trades. It is the opposite of the one heroic call. It is a casino running its slim house edge across a huge number of hands.

Third, and this is the honest part almost nobody selling you a strategy will say out loud, the edge decays

Residual mean reversion is real, and it has also been getting arbitraged away for two decades. The famous study of the plain pairs-trading version found it printed money for years and then faded as more capital crowded into the same trade

That is the pattern for all of it. The reversion is genuine, the capacity is limited, and the crowd competes it down. The desks that survive are not the ones that found the magic 200 lines of code

They are the ones that keep refreshing the factor model, rotating the universe, and moving faster than the crowd catching up. Anyone promising you a static residual signal that prints forever is selling the backtest, not the future.

And here is the reframe to sit with. Whatever your trading account did last year, most of it was the ninety-five percent you never meant to trade

If you held thirty names that all load on the market, your stock picking was drowned out by beta, and your P&L was mostly the tide moving your whole book at once

The residual is the only place your actual skill on a company could ever show up, the one part of a stock that answers to the business and not to the market's weather

Stat-arb funds figured out how to isolate exactly that part and trade nothing else. Retail spent the same years diversifying it out of existence and calling the leftover noise

None of the machinery is locked away

The factor model that produces the residuals is the same PCA from the last article, free in numpy

Fitting an Ornstein-Uhlenbeck process to a residual and reading off its half-life is a short script. The s-score is one line once you have the pieces. You can pull free daily data, hedge a single stock against a few factors, and watch its leftover oscillate around zero with your own eyes this afternoon. The barrier was never the tools. It was that nobody told you the only tradeable part of a stock was the part you were trained to throw away.

If you want to go deeper, start with three sources:

Statistical Arbitrage in the US Equities Market by Avellaneda and Lee, the clearest practical build of the whole idea, hedging out the factors, modeling the residual as a mean-reverting process, and trading the s-score.

Pairs Trading: Performance of a Relative-Value Arbitrage Rule by Gatev, Goetzmann and Rouwenhorst, the big empirical study that showed residual reversion made real money for decades, and was honest about how the edge thinned as the crowd arrived.

Pairs Trading: Quantitative Methods and Analysis by Ganapathy Vidyamurthy, the practitioner's walk through spreads, cointegration, and turning a mean-reverting leftover into an actual position.

Read those and you will understand why the part of a stock you were taught to ignore is the only part a serious desk ever looks at

Summary

A stock's daily move is mostly the market and the sector, with a thin company-specific leftover riding on top. That leftover is the residual, and it is the only part of the move that is genuinely about the business. Diversifying a normal book cancels those residuals out and leaves you holding pure forces, which is why your spread of names feels exactly like the index.

Stat-arb funds run it backwards. They hedge the forces away and keep a giant basket of residuals, because the forces are close to unpredictable and the residual is not

Once the factors are stripped out, the leftover is stationary: it drifts from its mean and gets pulled back, and an Ornstein-Uhlenbeck process measures how hard and how fast. Standardize that deviation into an s-score, short what is too rich, buy what is too cheap, close as it reverts.

The trade is market-neutral by construction, the edge on any single name is thin, and the money comes from running it small across hundreds of names at once. It also decays, and the honest desks know it, which is why they never stop refreshing the model.

So here is the question to sit with. The next time you are proud of a stock pick, ask how much of that gain was the company and how much was just the market carrying your whole book

Because the part that was actually about the business was the thin leftover you probably never looked at, and it is the only part the smartest money in the world bothers to trade at all.