Thread Truncated (Cap Enforced)

Only the first 20 tweets are unrolled into slides to ensure reliable PDF exporting and high server performance.

Canvas & Ratio

Choose your destination platform format

Layout Template

Choose a content structure for your slides

Preset Themes

Typography & Sizing

Brand Kit Customization

AGENCYConfigure brand assets for headers & footers

Outro Slide CTA

Customize your closing call-to-action slide

Background Pattern

Build Your Carousel

Drag and drop any post card below onto a slide, or use the quick buttons to insert content/images instantly!

> They don't use the same algorithm. They use the same thinking. Behind every profitable trader is not luck, intuition, or a mysterious black-box AI. There is concrete mathematics.

## 1. The Math Under the Hood

Most people look at a Polymarket account making $400K in a month and say: lucky bot. They're wrong.

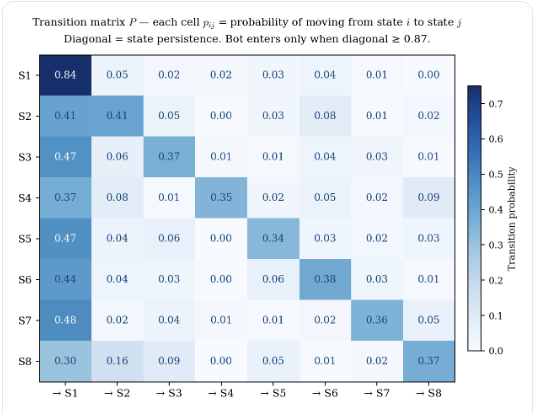

There's a mathematical framework behind every single trade - one that has been in academic literature since the 1950s and is still almost completely absent from prediction markets. It's called <b>Markov Chains</b>. The core tool is the transition matrix ( P ), where each element pijp_{ij}p_{ij} represents the probability of moving from state ( i ) to state ( j ):

The core idea is deliberately simple: you don't need to predict where price is going. You need to measure which state the market is in right now - and what the probability of the next state is. If that probability is high enough, you enter. If it is not, you wait.

No technical analysis. No news reading. No gut feeling. Just a probability table, updated every minute from live data.

The machine builds a <b>transition matrix</b> - a grid of probabilities mapping every price state to the likelihood of the next one. The diagonal of that matrix is the key: how likely the market is to <i>stay in its current state</i>. Entry happens only when that diagonal value clears <b>0.87</b>.

Transition matrix P - each diagonal cell is the state persistence value. Bot enters only when p(j*,j*) ≥ 0.87

<pre><code lang="python">Core entry filter — two conditions, both must be true def should_enter(P, current_state, market_price, tau=0.87, eps=0.05): # Enter only when gap AND persistence both clear j_star = np.argmax(P[current_state]) # optimal next state p_hat = P[current_state][j_star] # model probability persist = P[j_star][j_star] # diagonal: state persistence gap = p_hat - market_price # arbitrage gap delta (2.2) return gap >= eps and persist >= tau # eq.(2.2) AND eq.(2.3)</code></pre>

> Two conditions. Both must be true. One function is the entire decision engine - and it runs <b>once per minute, across every open window, on every asset, 24 hours a day.</b>

---

## 2. Three Accounts. One Month

Here are three bots that ran this framework on Polymarket in March–April 2026. Different assets, different entry logic, different position sizes. Same underlying principle.

These are not outlier results. They follow directly from the parameter specifications in the math. Let's look at the formal parameter table: