The Math That Made $1M+ for quant Traders in 30 Days

They don't use the same algorithm. They use the same thinking.

Behind every profitable trader is not luck, intuition, or a mysterious black-box AI. There is concrete mathematics.

1. The Math Under the Hood

Most people look at a Polymarket account making $400K in a month and say: lucky bot. They're wrong.

There's a mathematical framework behind every single trade - one that has been in academic literature since the 1950s and is still almost completely absent from prediction markets. It's called Markov Chains.

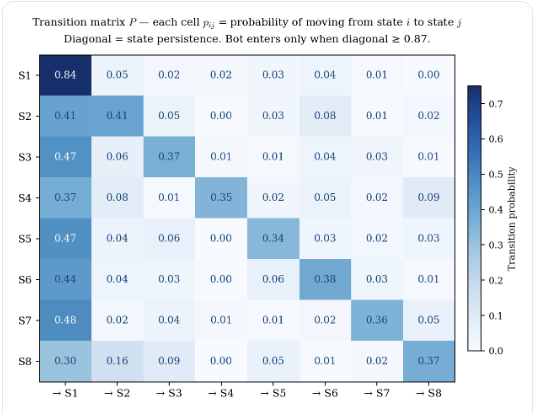

The core tool is the transition matrix ( P ), where each element pijp_{ij}p_{ij} represents the probability of moving from state ( i ) to state ( j ):

The core idea is deliberately simple: you don't need to predict where price is going. You need to measure which state the market is in right now - and what the probability of the next state is. If that probability is high enough, you enter. If it is not, you wait.

No technical analysis. No news reading. No gut feeling. Just a probability table, updated every minute from live data.

The machine builds a transition matrix - a grid of probabilities mapping every price state to the likelihood of the next one. The diagonal of that matrix is the key: how likely the market is to stay in its current state. Entry happens only when that diagonal value clears 0.87.

Transition matrix P - each diagonal cell is the state persistence value. Bot enters only when p(j*,j*) ≥ 0.87

Core entry filter — two conditions, both must be true

def should_enter(P, current_state, market_price, tau=0.87, eps=0.05):

# Enter only when gap AND persistence both clear

j_star = np.argmax(P[current_state]) # optimal next state

p_hat = P[current_state][j_star] # model probability

persist = P[j_star][j_star] # diagonal: state persistence

gap = p_hat - market_price # arbitrage gap delta (2.2)

return gap >= eps and persist >= tau # eq.(2.2) AND eq.(2.3)Two conditions. Both must be true. One function is the entire decision engine - and it runs once per minute, across every open window, on every asset, 24 hours a day.

2. Three Accounts. One Month

Here are three bots that ran this framework on Polymarket in March–April 2026. Different assets, different entry logic, different position sizes. Same underlying principle.

These are not outlier results. They follow directly from the parameter specifications in the math. Let's look at the formal parameter table:

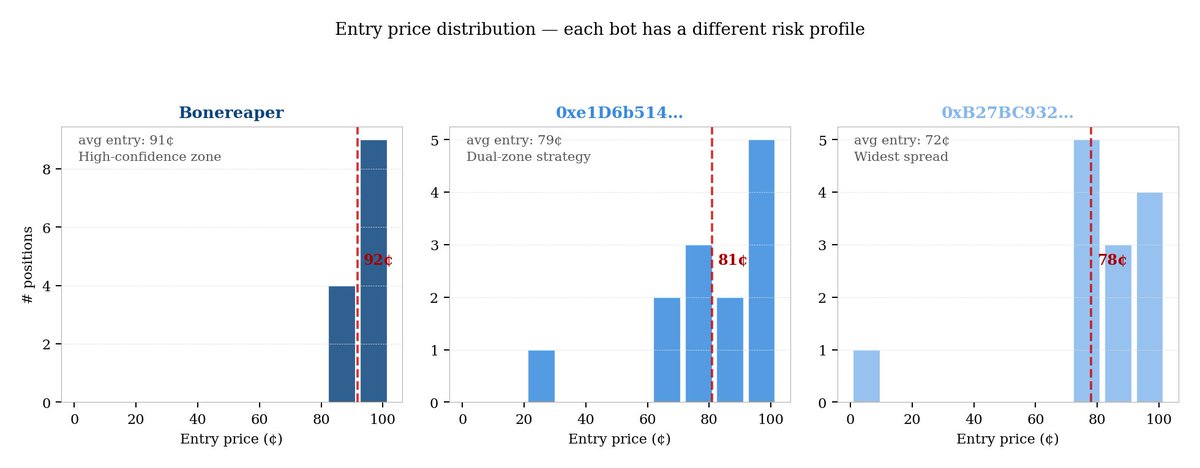

Bonereaper operates in the narrowest entry window (83–97¢), yielding the lowest variance. 0xB27BC932 accepts entries from 1–96¢, maximizing trade frequency at the cost of higher per-trade variance. Both are profitable - just different implementations of eq. (2.7).

3. How Each Bot Reads the Market

Same principle. Three completely different implementations. Here is the math that separates them.

Eq. (2.8): expected return = (1 − q) / q ≈ 10% at mean entry 91¢

Trades hourly BTC and ETH Up/Down windows at 83–97¢. The model agrees with the crowd direction but sees the market underpricing certainty. 1,500–2,900 shares per position. Collects 4–19% per resolution. Low variance.

BTC + ETH 1h windows Entry 83–97 ¢r̅ = 0.038%

Eq. (2.9): blended EV from two concurrent strategies

Directional scalps at 64–83¢ (20–54% per trade) running alongside price level locks at 99.5–99.8¢. The $42,200 best trade at 64.7¢ entry follows eq. (2.10): r = 0.353/0.647 = 54.6%.

BTC + ETH Dual strategy Entry 64–99¢ Max +54.6%

Eq. (2.11): 5 assets reduces volatility by 55% at same expected return

BTC, ETH, SOL, BNB, XRP across 5-min windows. Entry at 1.3¢ follows eq. (2.12): mark-to-market return = (0.655−0.013)/0.013 = 4876%, unrealized. Volume is the edge: 1 trade per 1.7 minutes.

5 assets 5-min windows σ reduced 55% 1 trade / 1.7 min

Lower entry = higher potential return per eq. (2.8). The tradeoff is variance. All three found their own working balance - all three profitable.

4. The Real Edge

Here is the part nobody talks about. Polymarket's crypto markets are priced by humans. And humans have a fundamental limitation: they are not online at 3AM watching a 5-minute BTC window.

When human attention drops, the market still sets prices - but those prices are lazy, stale, and exploitable. The gap M(t) from eq. (2.13) is widest precisely when nobody is watching.

The second layer is compounding. Eq. (2.14)–(2.15) show that by the law of large numbers, sample mean log-returns converge to the true expected return - making the exponential growth formula exact for large N.

Kelly criterion (eq. 2.17) explains why the bots don't blow up: f* ≈ 0.71 is high enough to compound aggressively, low enough to avoid ruin. It's not luck. It's optimal bet sizing.

5. The Closer

$1,331,821 in 30 days.

Three bots. Three strategies.

One mathematical principle.

“The market rewards people who understand probability.

Everyone else is just providing the liquidity.”

3 traders from article:

1. https://polymarket.com/profile/0xeebde7a0e019a63e6b476eb425505b7b3e6eba30?via=track

Fastest way to copy-trade them even with $10 using: http://kreo.app/@0xRicker

A perfect example of a trader from the article

polymarket.com/profile/0xe1d6…

x.com/0xRicker/statu…