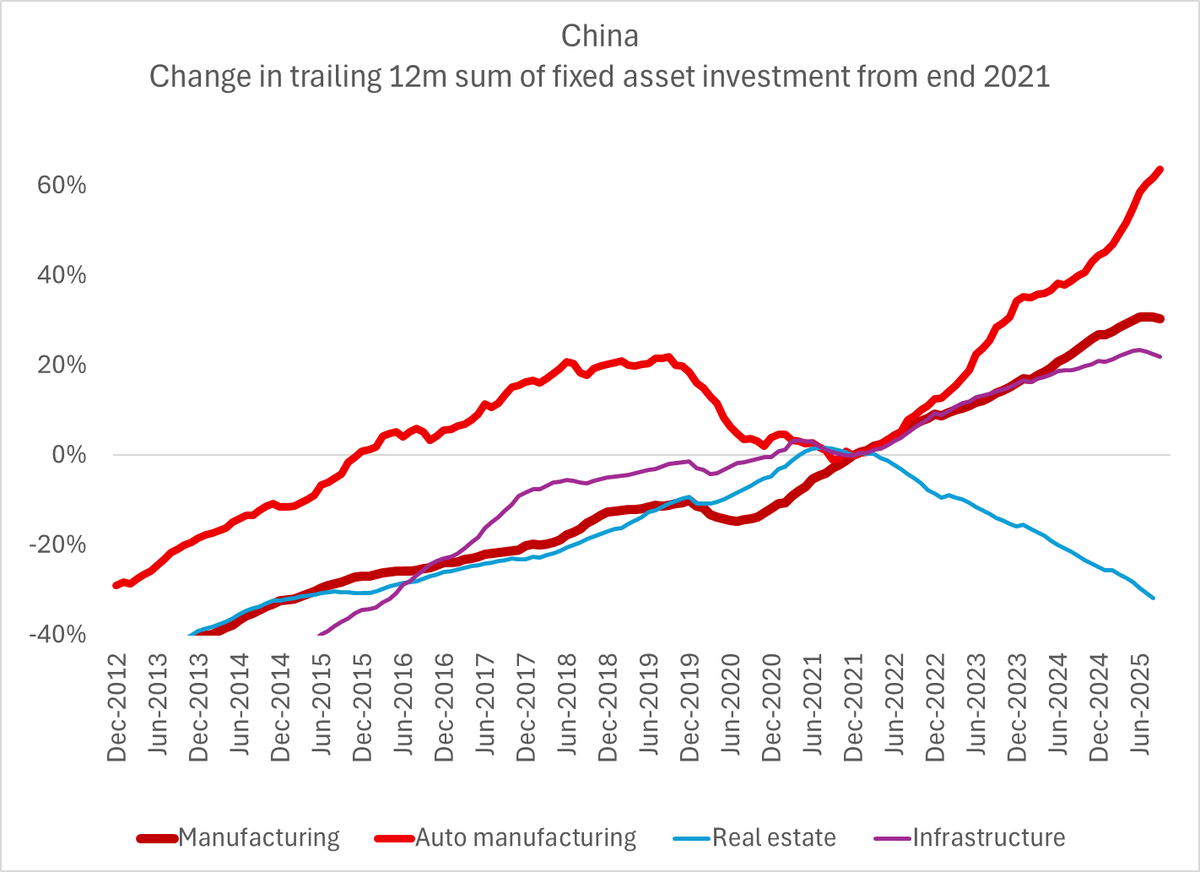

Chinese investment has stalled out in the third quarter. Real estate investment continues to fall, and infrastructure and manufacturing investment have stopped growing .... with one notable exception: autos

1/

Autos are an interesting sector for the global economy because the incremental Chinese production since 2018 has basically come from exports -- the domestic market has been around 25m cars for a while

2/

2/

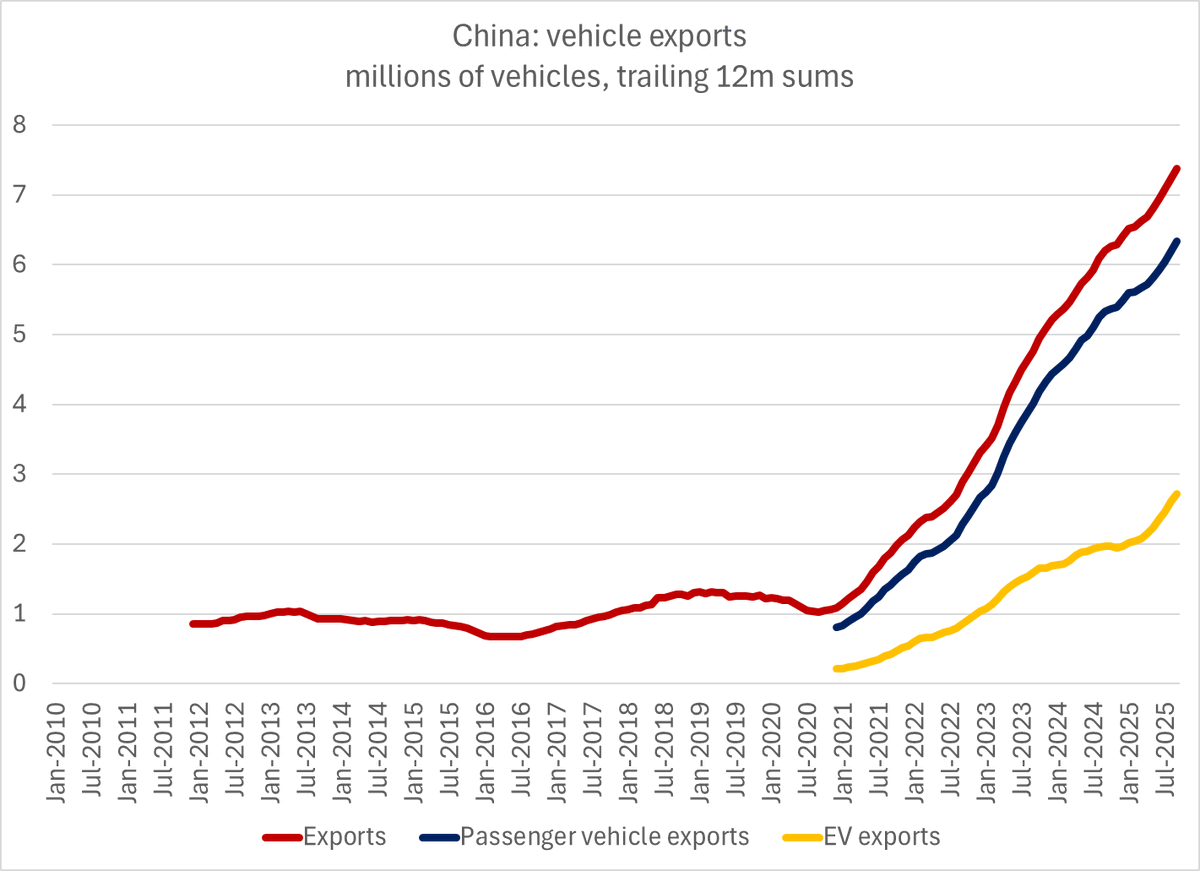

Vehicle exports will top 7.5m cars/ tracks this year -- and are on trajectory to reach 8-9m next year (massive scale) ... with a strong contribution from EVs and pug in hybrids in 2025

3/

3/

ICEs and EVs/ NEVs are basically splitting the domestic market (ICE sales have stabilized at around 12m cars), which means a lot of China's 20-25m in EV production capacity is available for export

4/

4/

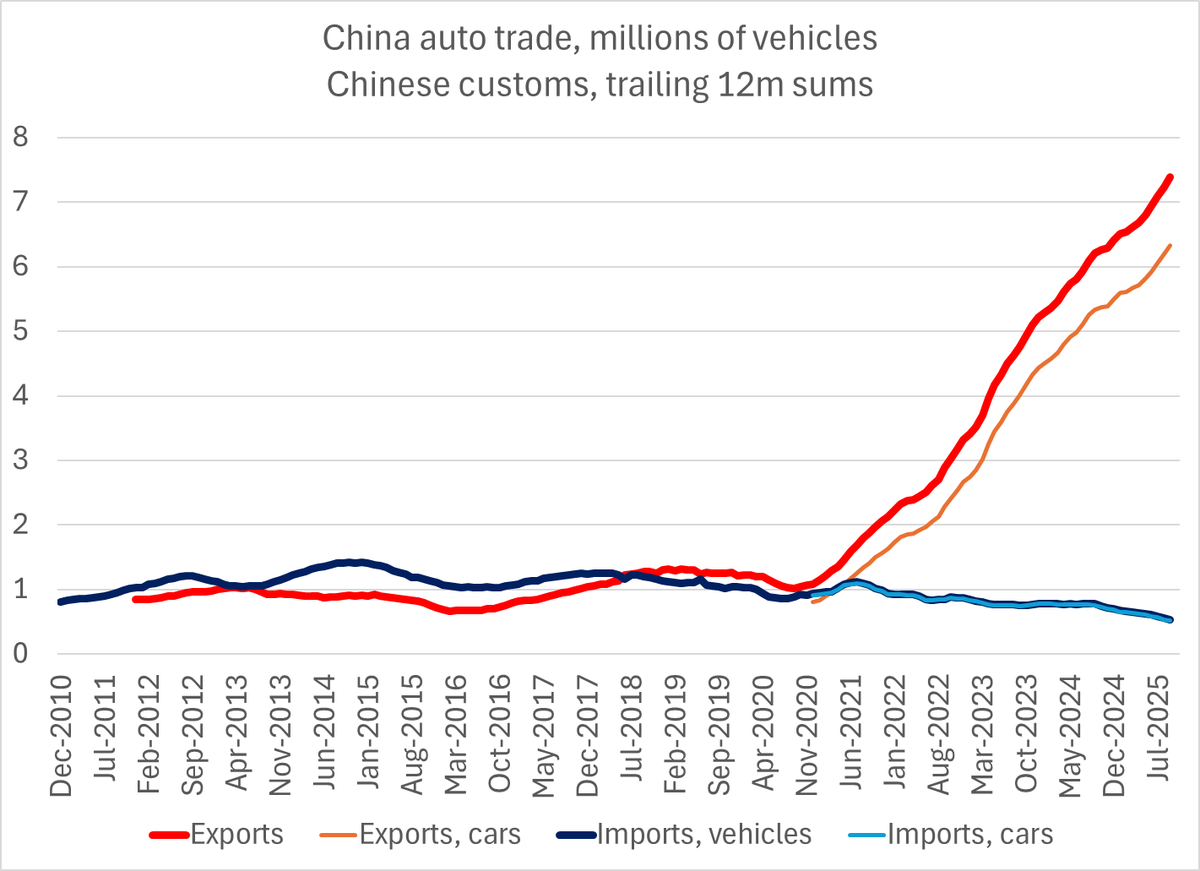

The swing in China's net exports of autos is massive -- and so big that it should on its own lead the IMF to question its view that China's external surplus is only modest in size and not a major global policy concern ...

5/

5/

And China's auto imports have basically fallen in 1/2 since 2021, and will be down to 0.5m cars this year (tiny v a domestic market of 25m cars). This chart alone explains much of Germany's current malaise ...

6/

6/

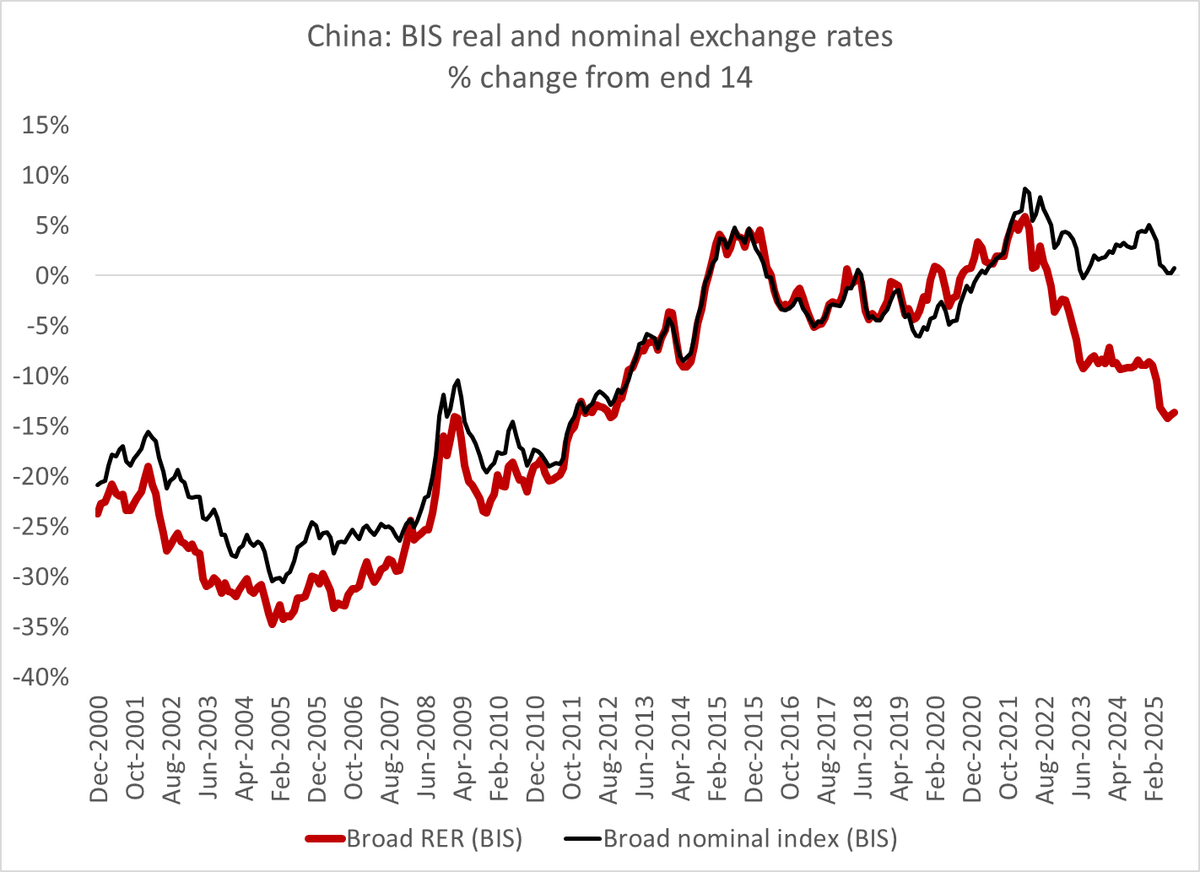

Personally don't see how more balance can be brought into global trade by adjusting sectoral Chinese policies alone (China isn't going to stop adding auto export capacity ... )

But I gather @IMFNews isn't convinced (yet) that the exchange rate needs to play a role

7/7

But I gather @IMFNews isn't convinced (yet) that the exchange rate needs to play a role

7/7

Generated by Thread Navigator

Press ⌘ + S to quick-export