RSI for AI: Truth, Fiction and Economics

Introduction

The concept of recursive self-improvement (RSI) for AI has been a polarizing topic in the technology industry since Irving John Good explored it in his 1966 paper, Speculations Concerning the First Ultraintelligent Machine (Good, I.J., 1966). For much of the time since then, RSI has been a more appropriate topic for science fiction rather than a serious issue for technology business leaders or economists to consider; indeed, Good is also famous for being the technology consultant (along with Marvin Minsky) for Stanley Kubrick during the production of 2001: A Space Odyssey. The science-fiction value of the concept was certainly clear.

Given the rapid pace of AI development and the fact that some of the frontier labs have explicitly defined automated AI researchers as a goal (OpenAI, 2026), it seems appropriate to explore RSI as a real possibility. In particular, the potential impact of RSI on the AI industry’s competitive landscape and the broader economy will likely be top of mind as we progress through 2026. Whether or not the reader believes in the possibility of RSI, it’s important to understand the concept to decipher the research directions of the frontier labs and potential considerations of policy makers.

"...when I look at all the publicly available information I reluctantly come to the view that there’s a likely chance (60% +) that no-human-involved AI R&D – an AI system powerful enough that it could plausibly autonomously build its own successor – happens by the end of 2028.”

--Jack Clark, Co-founder of Anthropic, May 2026 (Clark, J., 2026)

Some key takeaways from this paper are as follows:

What is RSI?

“Edison said that genius is 1% inspiration and 99% perspiration. But we see perspiration becoming increasingly automated. It’s becoming clear that much of what advances the frontier [of AI] is automatable.”

--Anthropic, June 2026

RSI can best be defined as “AI improving AI”, but the definition is often stretched in popular discourse. Some shout “RSI” when code autocompletes, and others argue it’s synonymous with superintelligence. This paper adopts a narrow definition: nothing merits the label “RSI” until the research loop closes. More specifically, this means an AI system that can ideate, build, evaluate, deploy, and iterate improvements without a human in the loop. A loop that requires a human to close it is not recursive; it’s human-directed acceleration.

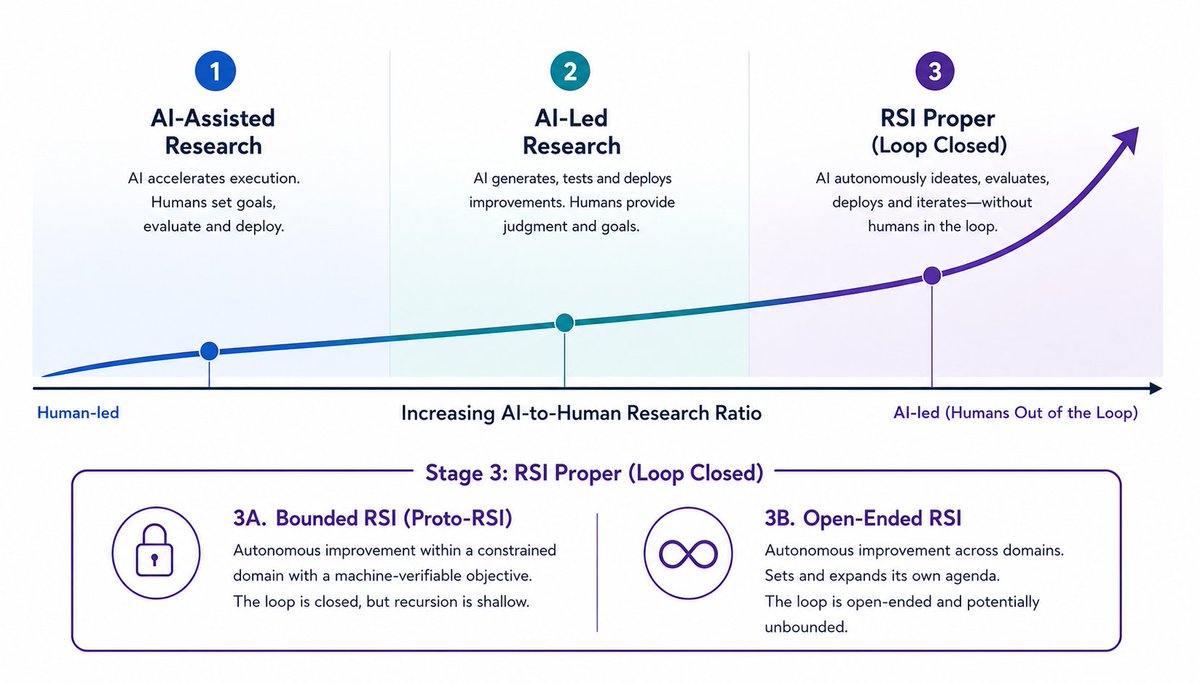

With that said, AI augmentation of research is powerful, and we’re beginning to see the benefits. As such, this paper defines augmentation as part of the ladder to RSI, and it remains debatable when or if we reach the ultimate destination. The ladder to RSI is segmented into three stages, with each increment increasing the AI-to-Human research ratio.

Stage 1: AI-Assisted Research

The earliest forms of AI-assisted research involve AI systems that improve themselves in niche domains, though autonomy is limited because humans are critical for defining goals and enforcing guardrails. In other words, AI accelerates execution, but humans own ideation, evaluation, and deployment. The coding agents that began to take the world by storm in late 2025 belong in this category; they automated Edison’s perspiration within tasks that humans specified, iteration by iteration. The technological consequence of AI-assisted research is faster, more efficient AI model and agent development, and the economic consequence is partial relief from the scarcity and cost of human software developer time. If automation had halted at this level, RSI would remain a minor topic of interest for business and technology leaders.

Stage 2: AI-Led Research

The next phase of AI research is when AI can increasingly generate, test, and deploy improvements in AI software and hardware design. Still, human researchers remain important for high-level decisions, novel research ideas, and goal setting. The industry is arguably approaching this realm in 2026, both in hardware and software. A recent example is Broadcom and OpenAI’s Jalapeño inference chip, where OpenAI’s own models accelerated the design and optimization process; the result was that AI assistance allowed the chip to go from “initial design to manufacturing tape-out in just nine months” (OpenAI, 2026).

On the software side, Anthropic recently noted that “as of May 2026, more than 80% of the code we merge into Anthropic’s codebase was authored by Claude,” enabling their engineers to ship 8x more code per day compared to a 2024 baseline (Anthropic, 2026). Over time, this level of automation in software and hardware research holds the promise of further accelerating AI progress, and the economic consequence is a technology wave that introduces new products and disrupts legacy segments faster than any cycle we have experienced thus far. The defining feature of AI-led research is that the human role has narrowed to judgment. Humans still choose which problems matter and which results to trust. Anthropic has identified this as “research taste,” and in Edison’s parlance, the perspiration is increasingly automated but the inspiration is not. The key to Stage 2 is that humans are beginning to become a bottleneck, as they can no longer review code as quickly as AI generates it. When the constraint on the pace of AI progress becomes the human gate itself, the economic and competitive pressure to remove that gate becomes ever larger. That pressure is the bridge to Stage 3.

Stage 3: RSI Proper

In stage 3, the loop closes: ideation, evaluation, deployment, and persistent iteration run autonomously. This is the form that many researchers are referring to when discussing “RSI”, with the implication that everything before wasn’t really RSI at all. Nevertheless, it’s helpful to refine this definition by splitting Stage 3 into two forms, as the first has already been demonstrated in embryonic form.

Bounded RSI. This is an autonomous improvement loop that is confined to a constrained domain with a fixed, machine-verifiable objective. Strictly speaking, we could call this “proto-RSI” or “Stage 2.9.” DeepMind’s AlphaEvolve project presents a seed of how RSI could work (Novikov, A., 2025). AlphaEvolve is essentially an agentic framework that leverages the probabilistic nature of LLMs for “creativity”, and candidate suggestions are tested with deterministic processes; it essentially runs a dynamic curriculum without human intervention and sets the bar higher for each attempt. AlphaEvolve hasn’t proven it can solve open-ended problems. Still, it discovered a 4x4 complex-valued matrix multiplication algorithm using only 48 multiplications, marking the first improvement in this task in over 56 years. Google has also used AlphaEvolve to produce novel improvements in its circuit design for its TPUs. In addition, Andrei Karpathy’s autoresearch project, released in March 2026, is arguably a bounded RSI loop. It runs a fully autonomous modify, measure, keep-or-revert cycle overnight, with memory and rollback via git. The key with bounded RSI is that the loop is closed, but the recursion is shallow. In other words, the gains don’t compound into the improving system itself, which limits the real-world impact.

Open-ended RSI. The strongest form of RSI would likely need to solve both the perspiration and inspiration components of the Edison construct, and with full autonomy. This is a system that sets and expands its own research agenda and improves itself across domains. This is where most of the science fiction and ASI explorations focus their attention, and for good reason: RSI would be completely autonomous and could allow AI to rapidly improve itself with an extreme, hyper-exponential impact on the economy and humanity. Open-ended RSI remains unproven and possibly unreachable. Nevertheless, as we saw with the Jack Clark quote at the start of this paper, this is no longer dismissed as fantasy by the people building the systems. As a result, the barriers to its arrival and its potential impact deserve attention.

Figure 1: The Progression Ladder to RSI

In the Industrialization of Intelligence, I argued that the agentic AI revolution was on a path that mirrors progress in self-driving vehicles (Shope, B., 2026). This framework can also elucidate the path to RSI. The AI industry is currently running the AI-research equivalent of Level 3 autonomy; the system does the work and the human supervises. With fully autonomous driving, the leap from supervised to unsupervised autonomy is proving to be the most difficult, most contentious, and most consequential transition. The path to RSI is similar. With RSI, the signal to monitor is not necessarily model benchmarks; it’s the human gate.

RSI Mile Markers

“Our internal belief is that by March of 2028 we may have a significant fraction of our research being done by AI systems in tandem with our own researchers.”

--Sam Altman and Jakub Pachocki, June 2026

In the Industrialization of Intelligence, I also discussed the possibility of mechanisms that would allow frontier model development to enter a phase transition from power-law rules to continuous exponential improvements. RSI is one such mechanism (perhaps the most important), and I believe that progress in the following areas could serve as milestones in the development of RSI.

Automated software engineering. When coding agents can code as well as the best human, a core component of progress towards RSI is in place. So far, 2026 has been a banner year for the capabilities of coding agents, with some leading engineers publicly stating they no longer write code themselves (Lichtenberg, N., 2026). Of all the mile markers for RSI development, coding agents meeting or exceeding the capabilities of most engineers seems to have the clearest line of sight.

Automated chip and kernel design. As discussed, OpenAI recently cited LLM-assisted design as a key factor in the speed of its Jalapeño chip from design to tape-out. The same trend is occurring across the GPU, TPU, and ASIC complex. And in terms of kernel development, the demand for automation is only rising as the human talent for kernel development becomes increasingly scarce and expensive. As I discuss later in this paper, hardware development automation may offer the most bang for the buck from an economic perspective, and the seeds of a rapid takeoff in this arena seem to be in place. Better chips drive better models, and if better models can produce better chips, a powerful feedback loop will emerge.

Frontier mathematical capabilities. The nature of LLM progress is inherently mathematical, with calculus and linear algebra as the primary tools for both training and inference. It stands to reason that more rapid leaps or entirely new paradigms for foundation models (potentially beyond LLMs themselves) will require deep mathematical knowledge and insights. Over the past year, several notable mathematical problems have been solved by AI, though it remains debatable if AI can produce novel mathematical insights. Nevertheless, recently, computer scientist Omri Weinstein had been skeptical of LLMs doing general math research, but he noted recent harness development from researchers at Columbia University had challenged this skepticism (Balko, M., 2026); Weinstein noted that, “using a clever ‘prover-verifier’ LLM loop, this harness solved 9 substantial open problems in Theoretical CS, including one that kept me up at night for 2 years” (Weinstein, O., 2026). Math is highly verifiable, so we may pass this mile marker quickly.

Task length improvements. The ability for models to stay on task for long periods of time is not only critical for high-ROI agentic applications but also an important pre-requisite for strong RSI. As discussed in The Battle for The Agentic Enterprise (Shope, B., 2026), task-length progress, as measured by METR, suggests performance on this metric is on a rapid exponential trend (Figure 2). Indeed, Epoch AI noted that current “AI models can complete certain software engineering tasks that are estimated to take humans weeks or longer" (Epoch AI, 2026).

Figure 2: METR Suggests Task-Length Improvement is on a Sharp Exponential Trend

Barriers to RSI

While RSI has certainly transitioned from the realm of science fiction to a real area of research at frontier model labs, it’s important to recognize the potential barriers to its development. These barriers could serve as a progress wall or merely a delay, but they should be explored. In researching this paper, a June 2026 DeepMind paper, From AGI to ASI (Genewein, T., 2026), provided the most comprehensive discussion of progress bottlenecks, some of which are included in the points below:

The data wall. Model training and test-time compute require ever-growing amounts of high-quality data. While synthetic data, real-world interactions, and paradigm shifts in data efficiency could counter this barrier, it is reasonable to worry that recursive training on self-generated data could degrade model capability.

Compute, energy, and capital scarcity. If RSI follows current scaling laws, resource limitations could prove insurmountable. The capital intensity of AI is already far beyond any expectations from the start of the Gen AI boom, and RSI could greatly amplify this. Of course, if novel training frameworks are developed or AI moves beyond its current LLM-centricity, the resources required for model improvements could be lower than current scaling laws suggest.

The “low-hanging fruit” problem. As research continues to advance, incremental discovery may require more complex experiments and resources, making progress more difficult. This sparseness of new ideas concept could, of course, be countered by sharp improvements in AI research efficiency from automation, but it’s not a certainty.

The challenges of verifying open-ended problems. Many theoretical RSI loops depend on verifying if a proposed improvement is actually better (i.e., AlphaEvolve). Open-ended science, architecture design, and real-world deployment could be difficult to verify. It seems clear that the path to RSI will require substantial improvements in verification and evaluation methodologies.

Political and societal constraints. As we have seen with recent model releases from OpenAI and Anthropic, the risks of new frontier model capabilities can trigger immediate and consequential government restrictions. One could imagine that far more capable models, and certainly self-improving AI, would amplify perceived risks, and that moratoriums or restrictive licensing regimes could emerge to slow progress.

This paper doesn’t address the desirability or moral implications of RSI. As such, the reader can decide whether the barriers to RSI’s emergence are positive or negative from a societal perspective. Regardless, real barriers exist, and they are critical in any forecast of RSI’s potential and timeline.

Economic Implications of RSI

Aside from vacillating between predictions of utopia or disaster, popular discourse on RSI often lacks rigorous economic analyses of its implications. Nevertheless, economists have studied the implications of automation since the early 1800s, and recent work has examined AI-driven automation and RSI specifically. We explore some of this work in this section, focusing on both the bull and bear cases. Readers should note that these frameworks are based on economic models with particular calibrations; they are not forecasts.

The Increasing Returns Bull Case

“By considering the interconnected roles of hardware, software, and general technological progress, we show that automation of research and development could generate feedback effects leading to explosive growth.”

--Davidson, Halperin, et.al., April 2026 (Davidson, T., 2026)

A quantitative bull case for AI automation’s impact on economic growth was thoroughly explored in an April 2026 working paper from researchers at Columbia University, the University of Virginia, and Forethought. The paper, When Does Automating AI Research Produce Explosive Growth?, explores how technological and economic feedback loops can counter diminishing returns and bottlenecks that normally keep economic growth range bound. The key takeaways from their framework are as follows:

Hypergrowth doesn’t follow RSI unless diminishing returns are countered. In contrast to frameworks from prior academics such as Irving John Good, the researchers note that diminishing returns limit the economic potential of RSI, as ideas become harder to find over time and dampen any exponential growth.

But innovation spillovers can counter these diminishing returns. If ideas can spillover from one discipline to another, such that software helps hardware progress, hardware helps software progress, and both software and hardware can help other research sectors, then a network of spillovers can have a similar effect to increasing returns within any one technology category. If these cross-feedback loops can exceed the drag of diminishing returns, the resulting economic growth can become hyperbolic.

Economic feedback loops amplify spillover effects. If improved technology from RSI increases economic output, that output can fund more capital and research, which, in turn, improves technology. This is particularly important given the capital intensity of current AI systems (driven by scaling laws), as the economic feedback loop directly addresses resource constraints.

Automation itself creates new loops by turning labor tasks into capital tasks. Starting with the baseline that labor does not automatically scale with GDP (i.e., economic growth doesn’t necessarily produce more AI researchers), the authors directly tie AI-driven automation with economic feedback loops. Since machine labor can scale with capital, automation itself enhances feedback loops and further counters diminishing returns and bottlenecks.

Hardware research is the strongest lever. The paper argues that hardware research has a greater impact than software or general research. As such, automation of just 20% of hardware research can cross the diminishing returns threshold and produce economic hypergrowth. The paper’s math also suggests that 13% automation across software, hardware, and general research is enough to push the economy into explosive growth.

The paper’s framework doesn’t identify a specific level of GDP growth but instead focuses on the math that produces exponential acceleration in GDP growth. In other words, in the first year of takeoff, you may have 4% growth, but that could progress to double digits the year after and so on. The key takeaway for studying the economic impact of RSI is that the authors present a case in which AI is not a “normal” technology wave. A typical technology can raise productivity in one sector, and a general-purpose technology can raise productivity across many sectors; AI with RSI, on the other hand, can raise the productivity of the process that creates productivity improvements.

Figure 3: The Theoretical Path to Economic Hypergrowth from RSI

Furthermore, if productivity increases faster than money supply growth, RSI-driven hypergrowth could be deflationary in nature, holding monetary policy factors constant. This, of course, has both positives and negatives, but it certainly highlights the power of RSI to challenge normal economic rules of thumb.

Capital Formation, Bottlenecks, and the Consumption Bear Case

“Over time and under the right conditions, supply reduces demand, leaving everyone worse off in the long-run.”

--Benzell et al., October 2018 (Benzell, S., 2018)

The most defensible bear case for RSI’s effect on the economy isn’t the common “fewer jobs mean a weaker economy” argument; instead, the downsides stem from economic models in which automation erodes the link between technological progress and improved prosperity. In fact, the simulation in the Benzell et al. paper shows a scenario where “national income rises several percent, peaking at 7.8 percent above baseline ... but it ultimately declines, ending up 4.2 percent below its initial steady-state value.”

There are three pathways to consider for the bear case, and I touch on each below. Finally, I include a closing discussion of the core tension between the bull and bear cases and where I believe the balance tilts.

Automation breaks the savings flywheel

In the Robots Are Us paper, Benzell, Kotlikoff, LaGarda, and Sachs provide a framework for thinking of AI as durable “code” that accumulates over time and increasingly substitutes for the work of human engineers. Importantly, their framework allows for a boom-and-bust cycle that mirrors many historical general-purpose technologies. They assume that in the midst of a tech boom, there is growing demand for new types of code and human engineers that can create it; today’s related proof would be the increase in demand for engineers to manage coding agents and build agentic harnesses, despite the increased automation of code generation (Flight, F., 2026).

Benzell et al. then argue that this positive development is potentially followed by a downside as the supply of “code” increases, eventually compressing demand and wages for labor, particularly for the young. For this paper’s discussion, a translation of this would say that greater coding automation eventually drives down the demand for human engineers as the AI buildout progresses. This, and the automation of non-engineering sectors, eventually reduce the savings of displaced or distressed labor, which in turn decreases capital available in the future, slowing growth.

The argument produces several concrete claims. First, labor’s share of income rises, then rolls over, leading to a decline in total labor income and reduced savings and investment. Second, tech booms are followed by tech busts, as we have seen historically. And third, current economic output grows increasingly dependent on past software investment.

The other side of the argument is that apparently obvious policy remedies can backfire. For example, regulatory restrictions on labor supply to prop up individual wages during the bust phase can still shrink total labor income, thereby amplifying the savings flywheel problem. This leads us to the core bottleneck: income distribution.

The income distribution challenge

A critical component of the bear case rests on the mechanism of income distribution. Human jobs serve as the primary mechanism for distributing income to human laborers. If that pipeline breaks down or becomes less effective, consumption can decline as rapidly as automation increases. In this case, GDP can still rise while many groups end up worse off (Korinek, A., 2017). Furthermore, if income is shifting from labor to capital and capital owners have a lower marginal propensity to consume (i.e., the rich save a larger share of each additional dollar), aggregate demand suffers (Mian, A. 2021).

The policy response could include broad capital ownership, sovereign wealth-style models, targeted taxation, and public investment, but these redistribution mechanisms must scale faster than automation breaks the paycheck channel. Fortunately, economists have also argued that the emergence of new, labor-intensive tasks has repeatedly countered past automation of tasks (Acemoglu, 2019).

Baumol’s cost disease and the automation bottleneck

The strongest case against explosive economic growth from AI rests on its limitations, or areas where digital labor can’t be utilized. Economist William Baumol made the argument that wages rise in areas even where productivity doesn’t. This has been termed “Baumol’s Cost Disease,” and it focuses on the fact that wages for historically low-productivity-growth services rise even when technology or industrial waves have little impact on these services (e.g., live entertainment, education, etc.). Economists Aghion, Jones, and Jones further this argument by showing that as automation makes certain segments cheap and abundant, spending migrates to areas that are hard to automate (Aghion, P., 2017). These bottleneck segments influence the overall economic growth rate, just as a supply chain is only as efficient as its slowest component. If automation can’t reach the slowest tasks, growth can be dampened. The Davidson-style spillovers discussed in the bull-case section offer specific mechanisms for countering Baumol’s bottlenecks. Still, the bears would argue this is true only if AI eventually reaches the bottleneck tasks.

Balancing the Bull and Bear Economic Cases

Neither the economic bull nor bear cases discussed thus far are forecasts; rather, each touches on economic frameworks that are constrained and amplified by modeling assumptions. I tend to land on the more optimistic case for several reasons. First, none of the bear cases fully refute the hypergrowth case from Davidson et al., which explicitly does not require mass labor displacement to achieve a growth takeoff. Furthermore, Benzell’s cautious path is admittedly countered by sufficient savings rates and targeted fiscal policy. History supports the idea that automation waves have repeatedly been offset by new, labor-intensive tasks for humans; more specifically, Acemoglu and Restrepo argue: “…automation technology also increases productivity, and via this channel, which we call ‘the productivity effect’, it contributes to the demand for labor in non-automated tasks.” We may be seeing this today, with human engineers increasingly serving as orchestrators of agent teams or even FDEs (forward-deployed engineers) as agentic AI increases demand for these new roles.

Whether the reader leans toward the positive or negative, it is clear that AI automation outcomes could be far more dependent on policy than prior technology cycles. This makes logical sense when considering a core argument from The Industrialization of Intelligence: prior technology cycles have been about new tools for humans, and agentic AI is about producing new digital labor. In addition, the bull and bear cases agree on similar puzzles. As digital labor emerges, the winners’ gains must be reinvested into capital formation, purchasing power, or both, for the aggregate economic outcome to be positive.

Implications for the Competitive Landscape

In The Battle for The Agentic Enterprise, I discussed how RSI could influence the competitive dynamics for frontier labs versus each other and versus incumbents and AI startups. In the battle for control of the agentic platform in the enterprise, RSI could clearly tilt the dynamic toward frontier labs, particularly if RSI allowed them to design better agentic architectures (i.e., “harnesses”) than competitors. The most interesting question, however, will likely be whether one lab enjoys the benefits of RSI well before the other labs. There are three considerations when pondering potential competitive outcomes, and I discuss each below.

The Red Queen Effect and winner-take-most dynamics

The Red Queen Effect was outlined in a recent preprint paper by economists from Chinese universities, and it shows how in frontier lab competition “a market leader experiences rapid economic depreciation if it fails to keep pace with frontier growth” (Zhang, Y., 2026). In other words, if one lab were to maintain a substantial capability lead over competitors and the Red Queen Effect makes the leader’s pace structurally unmatchable, winner-take-most outcomes become possible.

This is a particularly notable factor to consider when analyzing RSI outcomes. If one lab were to achieve RSI before its competitors, the resulting pace of innovation and cost efficiencies could dramatically and permanently shift the competitive momentum towards the leading lab. This is a surprising potential outcome when the current consensus tends to comfortably assume frontier lab business models are commoditizing.

Harness dynamism is the tie between RSI and durable share

The Red Queen Effect explains why an RSI leader’s pace could become unassailable, but pace is not necessarily a moat. The moat, driven by switching costs, depends on harness-model fit. In The Battle for The Agentic Enterprise, I argued that the frontier labs enjoy a zero-day advantage in harness model fit: the lab that trains the model understands its jagged capabilities before any third party, and every new release forces the rest of the ecosystem into a costly cycle of harness re-engineering. This is even more of a challenge for smaller, agentic startups than for larger incumbents. RSI can supercharge this dynamic by accelerating the frontier lab release cadence.

This can extend the Red Queen Effect because the leader’s cadence doesn’t just compress rivals’ model capital; it also depreciates every tuned prompt, context management strategy, and orchestration investment built against the prior frontier. The harness refactoring tax potentially compounds with each RSI-driven cycle.

Adversarial distillation is the fulcrum issue

Knowledge distillation for AI is when a teacher model “trains” a student model via the inference path. Basically, the student model asks the teacher model a large number of questions via prompts and uses the answers to improve its capabilities. This is an old concept in machine learning dating back to the early 2000s, and it can be a cost-efficient way for model providers to spin up lower-cost, lower-latency models from larger models. In fact, it’s relatively common for AI labs to do this to create specialized models from their primary models; Google reportedly did this with Gemini as a teacher model and Gemma models as students.

Nevertheless, when a competitor uses distillation to “copy” knowledge from another lab’s larger model, things can become problematic. Indeed, the economic and geopolitical ramifications of adversarial distillation are becoming an increasingly hot topic, as US frontier labs have alleged that Chinese labs are distilling their frontier models (Anthropic, 2026).

Surprisingly, the economic framework for adversarial distillation was formally modeled before the existence of frontier labs. The same Robots Are Us paper cited in the preceding economic bear case also focuses on what happens when “code” (i.e., model capability) is “non-rival” (the use of model capability doesn’t prevent another’s simultaneous use). This leaves us with the key variable for the competitive landscape: economic “excludability.”

Barriers to distillation exist (non-rival and excludable). This scenario mirrors pharmaceutical economics. A generic drug manufacturer cannot reverse-engineer and sell a patented drug while the patent on the formula is still active. In the case of AI, barriers to distillation allow for the Red Queen effect and winner-take-most dynamics for the labs. Long-run capability investment is funded and the ROI path is clearer. The downside is a concentration problem, as the industry could tilt toward oligopoly or monopoly at the intelligence layer.

Barriers to distillation are not present (non-rival, non-excludable). The pharma analog here is patent expiration. Now, a generic manufacturer can reverse-engineer the drug at a fraction of the original R&D cost. For AI, this leads to lower-cost inputs (tokens) at the application layer (agentic AI) and likely supports a highly competitive marketplace, particularly for AI natives and software incumbents. The harness dynamism component arguably offers some buffer against the distillation threat if harness-model fit remains excludable, but I assume model capability is a far greater lever. Benzell et al. note that the non-excludable model would appeal to governments “concerned about the concentration of power in the hands of a small number of superstar technology companies.” The downside is that frontier lab ROI is potentially compressed and frontier research compensation declines. I’d add that the market may follow highly cyclical commodity economics due to the capital-intensive nature of frontier development. An open question in this scenario is whether the economic reality would slow frontier capability research over time.

This debate becomes even more challenging when the dual-use nature of AI is taken into account. If we assume that national frontier AI capabilities are a critical component of geopolitical dynamics in the future, then governments must weigh the advantage of promoting AI “national champions” while weakening nation-state rivals versus allowing rival-state access and reducing domestic market concentration.

There is no clear “right” answer

Unless one can make the claim that AI does not pose safety issues or that it is not a dual-use technology, the popular debate over adversarial distillation and foreign open-source models has been overly simplistic thus far. This is particularly true when RSI is added to the mix. The Red Queen Effect and adversarial distillation are clearly opposing forces; at the same time, the “more competition is good” mantra doesn’t sit well with the debates over geopolitics or safety. In the end, distillation, a once-niche machine-learning technique from the early 2000s, may evolve into one of the most heated economic and policy debates of the AI era.

Conclusion

Recursive self-improvement was once confined to science fiction, but it is now a serious consideration for leading AI researchers. While the “this time is different” tone of the discourse around the topic appropriately triggers skepticism from battle-tested capital allocators and business leaders, even skeptics should understand how it is influencing AI builders and geopolitical debates. Achievable or not, RSI has the potential to reshape our understanding of technological progress and its economic implications. In addition, RSI is bound to become an increasingly important component of debates around open-source and adversarial distillation, which is top of mind amidst the recent backlash to “Tokenmaxxing” and the broader effort to increase the ROI of the agentic AI application space.

Sources

Good, I.J. (1966). Speculations Concerning the First Ultraintelligent Machine. Advances in Computers, Elsevier, Volume 6.

OpenAI (2026, June 8). Built to benefit everyone: our plan.

Clark, J. (2026, May 4). AI systems are about to start building themselves. Import AI 455. Substack.

OpenAI (2026, June 24). OpenAI and Broadcom unveil LLM-optimized inference chip.

Anthropic (2026, June). When AI builds itself. Our progress toward recursive self-improvement, and its implications.

Novikov, A., Vu, N., Eisenberger, M., et. al. (2025, June 16). AlphaEvolve: A coding agent for scientific and algorithmic discovery. arXiv.

Shope, B. (2026, January 30). The Industrialization of Intelligence, From Software to Digital Labor. The AI Wave. Substack.

Lichtenberg, N. (2026, June 11). The head of Claude Code hasn’t ‘written a line of code by hand’ in 8 months. Fortune.

Balko, M., Grebik, J., Hubacek, P. (2026, April 24). Bolzano: Case Studies in LLM-Assisted Mathematical Research. arXiv.

Weinstein, O. (2026, June 30). @WeinsteinOmri. x.com

Shope, B. (2026, June 17). The Battle for The Agentic Enterprise. The AI Wave. Substack.

Epoch AI (2026, June). Mirror Code: What’s the largest software project AI can complete on its own? Epoch.ai.

Genewein, T., Franklin, M., Lerchner, A. (2026, June 10). From AGI to ASI. arXiv.

Davidson, T., Halperin, B., Houlden, T. (2026, April). When Does Automating AI Research Produce Explosive Growth? Feedback Loops in Innovation Networks. Working Paper. NBER.

Benzell, S., Kotlikoff, L., LaGarda, G., Sachs, J. (2018, October, revised). Robots Are Us: Some Economics of Human Replacement. Working Paper. NBER.

Flight, F. (2026, February 24). The 2026 Global Intelligence Crisis. Citadel Securities.

Korinek, A., Stiglitz, J. (2017, December). Artificial Intelligence and Its Implications for Income Distribution and Unemployment. Working Paper. NBER.

Mian, A., Straub, L., Sufi, A. (2021, February). The Saving Glut of the Rich. NBER.

Acemoglu, D., Restrepo, P. (2019, Spring). Automation and New Tasks: How Technology Displaces and Reinstates Labor. The Journal of Economic Perspectives.

Baumol, W. (1967, June). Macroeconomics of Unbalanced Growth: The Anatomy of Urban Crisis. The American Economic Review, vol. 57.

Aghion, P., Jones, B., Jones, C. (2017, October). Artificial Intelligence and Economic Growth. Working Paper. NBER.

Zhang, Y., Tianyang, Z. (2026, January 18). The Economics of Digital Intelligence Capital: Endogenous Depreciation and the Structural Jevons Paradox. arXiv.

Anthropic (2026, February 23). Detecting and preventing distillation attacks.

Disclaimer: The views and opinions expressed in this article are solely my own and do not represent the views of my employer or its affiliates. This article is provided for general discussion purposes only, has not been prepared as investment research, and does not constitute investment advice, a recommendation, an offer or solicitation to buy or sell any securities or financial instruments.