Canvas & Ratio

Choose your destination platform format

Layout Template

Choose a content structure for your slides

Preset Themes

Typography & Sizing

Brand Kit Customization

AGENCYConfigure brand assets for headers & footers

Outro Slide CTA

Customize your closing call-to-action slide

Background Pattern

Build Your Carousel

Drag and drop any post card below onto a slide, or use the quick buttons to insert content/images instantly!

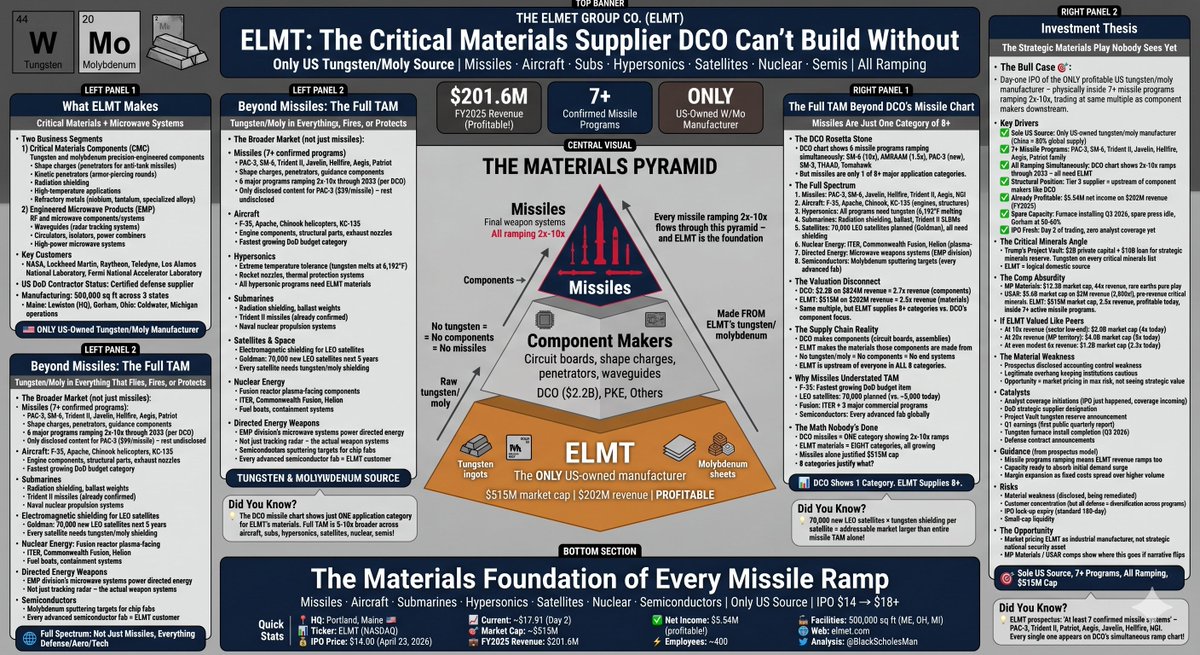

Most of you degens bought $ELMT on the IPO hoping for a quick flip and sold when it didn't happen. I actually took the time to understand the company and how it just became a critical national security player. Here's what you missed 🧵

What does $ELMT make? CMC division: ONLY U.S. vertically integrated maker of engineered tungsten & molybdenum. Raw powder to multiple DOD programs. Zero Chinese supply chain. EMP division: Radar waveguides, directed energy, fusion reactor components. Up to 60 MEGAWATTS output.

China controls 80% of global tungsten and has been weaponizing it since Feb 2025. Friday China blacklisted 7 European defense firms from receiving Chinese dual-use materials. $ELMT's entire supply chain sits outside China. That's not a competitive advantage. That's a national security asset.

$ELMT's tungsten & moly goes into virtually everything that flies, fires, or protects: Missiles, Aircraft, Submarines, Hypersonics, Directed energy, Satellites, Nuclear reactors, Semiconductor fabs 6 major missile programs alone are ramping 2x–10x through 2033. They only disclosed content for ONE of 7+ missile systems in their prospectus. They never disclose any other programs.

No analyst is modeling this The income statement they IPO'd on was built on PRE-RAMP rates. At IPO date: New tungsten furnace not installed yet (Q3 2026) Spare extrusion press sitting IDLE in storage EMP running at 50–60% capacity Defense backlog just surged 76% YoY The revenue is a lagging indicator. The ramp hasn't hit the P&L yet.

The math when the ramp hits: Fixed OpEx ~$29M. Barely moves as revenue scales. Every incremental dollar to $0.20 to operating income. 2027E bull case: Revenue: $350MNet income: ~$40–45M Current market cap: $515M That's a 12x forward PE on a sole-source defense materials manufacturer with zero non-China competition.

$USAR trades at $5.6B market cap on $2M revenue. Pre-revenue. $MP trades at 44x sales. Also not profitable. $ELMT trades at 2.6x sales. Profitable. In 7+ active missile systems. The catalyst isn't financial. It's narrative. The moment one analyst calls this a critical minerals play instead of an industrial manufacturer the multiple re-rates overnight. That coverage hasn't started yet.