Thread Truncated (Cap Enforced)

Only the first 20 tweets are unrolled into slides to ensure reliable PDF exporting and high server performance.

Canvas & Ratio

Choose your destination platform format

Layout Template

Choose a content structure for your slides

Preset Themes

Typography & Sizing

Brand Kit Customization

AGENCYConfigure brand assets for headers & footers

Outro Slide CTA

Customize your closing call-to-action slide

Background Pattern

Build Your Carousel

Drag and drop any post card below onto a slide, or use the quick buttons to insert content/images instantly!

🚨 The U.S. Treasury just changed the game. Trillions in short-term debt. Long-end buybacks. Crypto soaking up supply. This is the quietest move toward Yield Curve Control we’ve ever seen. (Save this thread)

To fund its operations, the U.S. government borrows money by issuing Treasuries, IOUs it sells to investors. There are 3 main types: • T-bills: Mature in under 1 year • Notes: Mature in 2–10 years • Bonds: Mature in 20–30 years The longer the maturity, the more stable the debt.

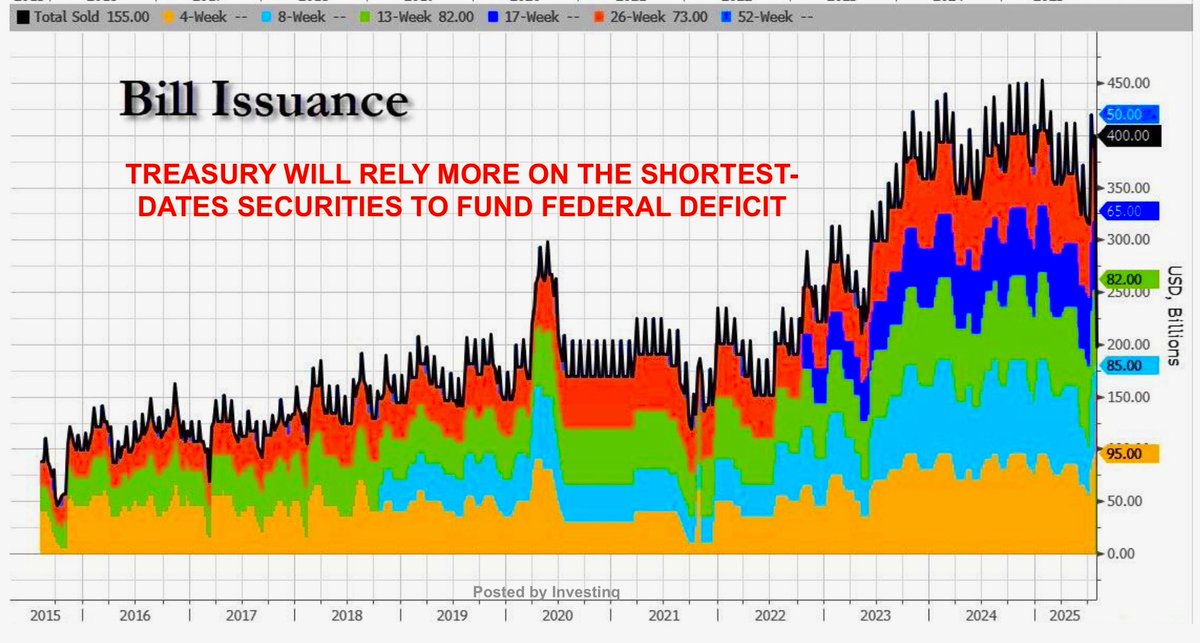

Traditionally, Treasury spreads borrowing across all three: short, medium, and long-term. but not anymore. The U.S. is now loading up on T-bills, the shortest-term, lowest-commitment debt. It’s the fiscal equivalent of taking out payday loans.

Why borrow short-term? Because it costs less today. But there’s a catch: it exposes the government to interest rate risk. If rates rise, we’ll have to refinance trillions of dollars at much higher costs over and over again.

It’s like getting a mortgage that resets every 3 months. When rates are low, it’s cheap but if they spike, you’re stuck paying way more. And that’s exactly the position the U.S. is now in.

Right now, the Fed’s benchmark interest rate, the federal funds rate is about 4.25%–4.5%. That’s one of the highest it’s been in nearly 20 years. And because T-bills follow this rate, borrowing short-term isn’t exactly cheap.

In fact, interest payments on U.S. debt have nearly tripled since 2020. This year, we’ll spend over $1 trillion just on interest more than on Medicare, and possibly more than on defense. It’s the fastest-growing item in the federal budget.

So why didn’t the U.S. issue long-term bonds when interest rates were near zero in 2020–2021? Answer: we missed the window. Instead of locking in 30-year loans at 1%, we’re now forced to borrow at over 4%. A painful strategic blunder.

Treasury Secretary Scott Bessent admitted this mistake. Now, he’s making a bet: Keep issuing cheap short-term debt and wait for interest rates to fall. But if rates stay high or rise? That bet backfires fast.

There’s another twist: The Treasury has started buying back long-term bonds something it hasn’t done in meaningful size for decades. It’s using money raised from short-term debt (T-bills) to buy back bonds that mature in 10–30 years.

Why do this? Because when the government reduces the supply of long-term bonds, it pushes their prices up and interest rates (yields) down. It’s a way to keep long-term borrowing costs low without the Fed needing to step in.

It’s very similar to Quantitative Easing (QE), a policy where the Fed buys bonds to lower interest rates and stimulate the economy. But in this case, it’s not the Fed doing it. It’s the Treasury. Some are calling it "Shadow QE."

And it’s not just QE, it’s also a form of Yield Curve Control (YCC). That’s when a government tries to control interest rates across the curve, short-term and long-term by actively managing debt issuance and bond supply.

Let’s define the yield curve: It’s a graph showing interest rates on Treasuries, from 1-month all the way to 30 years. Normally, it slopes upward longer loans should have higher interest. But now? It’s basically flat.

Why is the curve flat? Because the Treasury is flooding the market with short-term debt (which pushes those yields up) And buying back long-term bonds (which keeps those yields down). It’s creating a manufactured balance.

But for this strategy to work, you need a constant stream of people willing to buy T-bills. So who’s buying? The answer might surprise you: • Money market funds • Stablecoins (like USDT, USDC) • Banks and financial institutions

Let’s talk about money market funds. They manage over $7.4 trillion in cash. In 2025, many shifted away from Fed-backed reverse repos and into T-bills, which offer the same yield and more flexibility. This helped absorb the short-term debt flood.

Now here’s the wild part: crypto is helping fund the U.S. government. Stablecoins, cryptos that are pegged to the dollar are required to hold reserves, usually in the form of T-bills. That means every time someone mints USDC or USDT, it boosts demand for T-bills.

As of mid-2025, stablecoins held over $160 billion in short-term Treasuries. That’s a massive pool of demand coming from outside the traditional banking system. Even Treasury officials have acknowledged how important crypto demand has become.

But this brings new risks. If a stablecoin is shut down, hacked, or frozen by regulators, it may be forced to sell billions in T-bills quickly. That could spike short-term yields and create chaos tying government finance to crypto stability.