Thread Truncated (Cap Enforced)

Only the first 20 tweets are unrolled into slides to ensure reliable PDF exporting and high server performance.

Canvas & Ratio

Choose your destination platform format

Layout Template

Choose a content structure for your slides

Preset Themes

Typography & Sizing

Brand Kit Customization

AGENCYConfigure brand assets for headers & footers

Outro Slide CTA

Customize your closing call-to-action slide

Background Pattern

Build Your Carousel

Drag and drop any post card below onto a slide, or use the quick buttons to insert content/images instantly!

It’s happening AGAIN Buckle up. A thread 🧵

2/ A $54 trillion asset class has been bouncing back now This is happening after a crash as violent as during the pandemic and the Financial Crisis Today, a record 60% of US households have stock market exposure The big question now is: can this rally really last?

3/ To answer that, we’re going to dig into hard historical data But first, let’s outline the 3 potential paths ahead: 1) A sharp V-shape recovery back to all-time highs 2) A deeper pullback breaking the April 7th low 3) A choppy consolidation before another leg higher

4/ Let’s start with the V-shaped recovery For that to happen, we’d need a dramatic shift in the economic outlook Basically, all the fears priced in earlier this year would need to vanish soon That’s a big ask, but it’s not impossible Some are pointing to the US-China trade deal as a reason to be optimistic

5/ And we’ve seen V-shaped rebounds before The most recent example was 2020 When stocks crashed 35% from COVID only to snap back to ATHs in almost a straight line

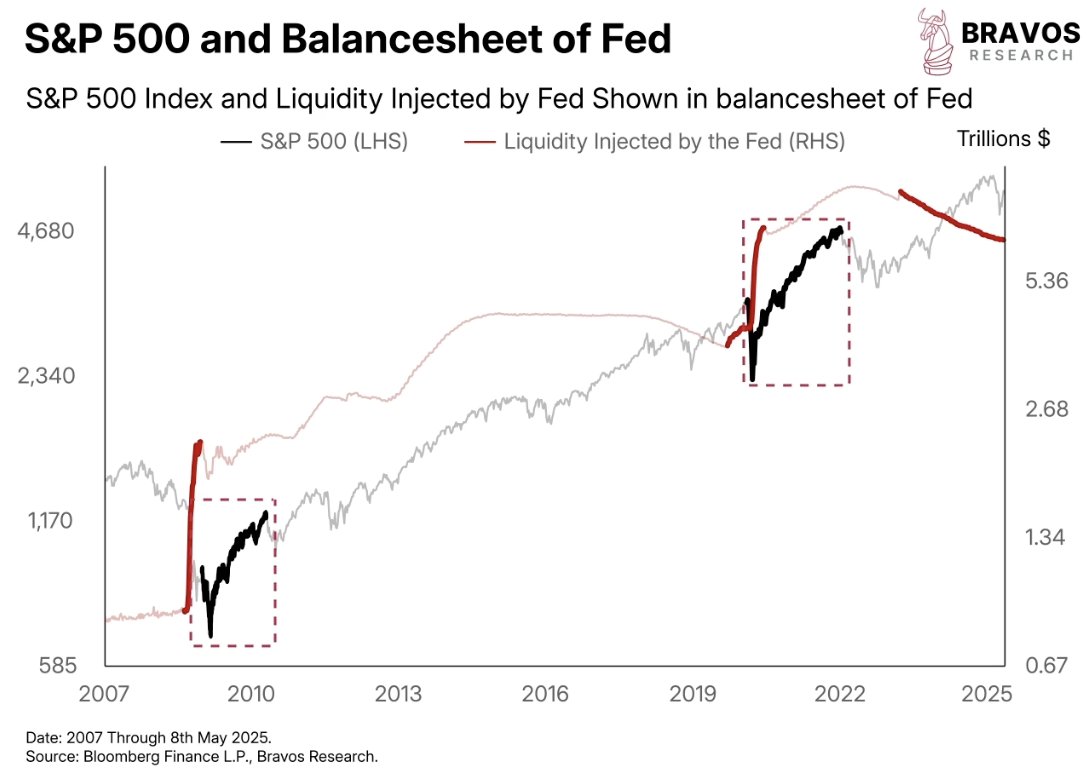

6/ Another example is late 2008 Investors went from fearing a total collapse to pricing in a strong rebound But both of these rallies had something huge behind them: Massive liquidity injections from the Fed

7/ We can see this by looking at the Fed’s balance sheet The biggest liquidity jumps in history came right before those V-shaped rallies Today, we’re not seeing the same setup Still, not everything is working against a V-shape recovery

8/ For one, corporate earnings have held up well Despite the 20% market drop, S&P 500 earnings estimates are actually higher now than they were in Jan And that strength is being driven by a few important tailwinds

9/ A weaker dollar is boosting international revenues Lower gas prices are helping consumers stay afloat And the Fed’s rate cuts over the past year may finally be filtering through the economy These are all supportive for earnings and growth

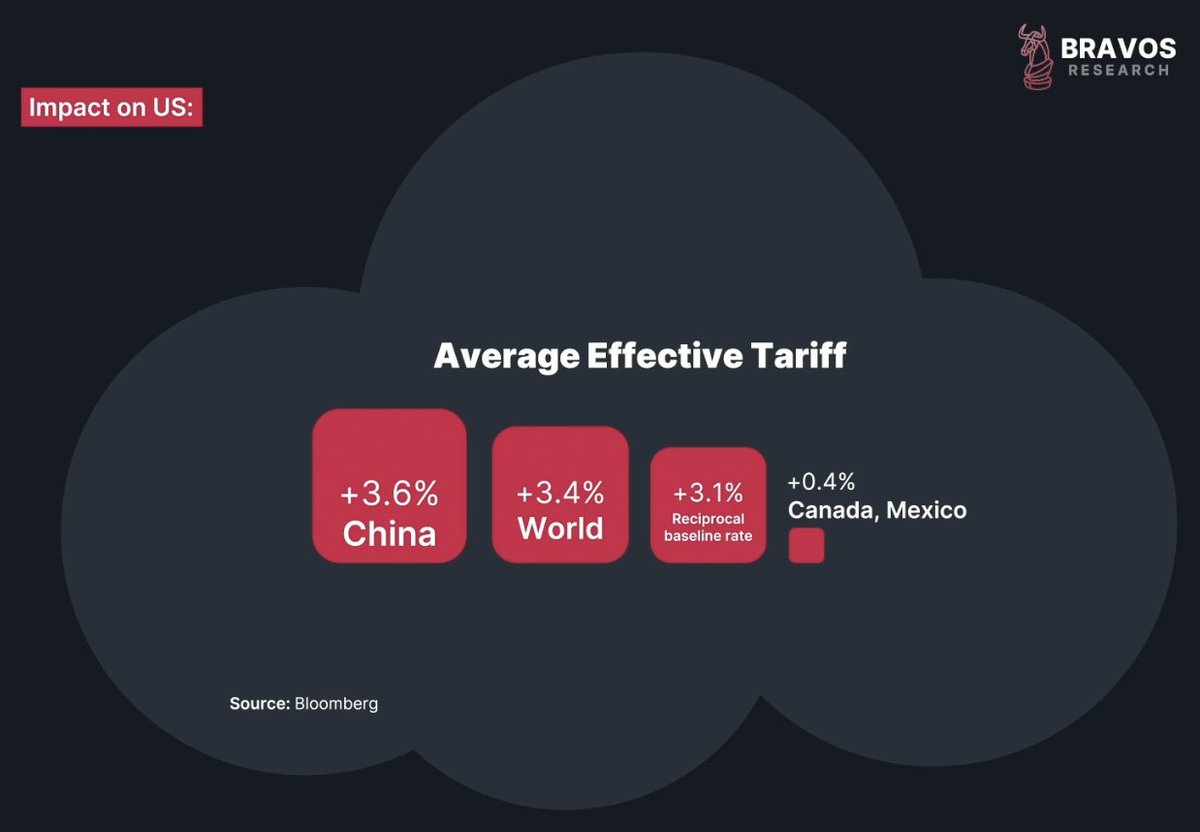

10/ We've been flagging these tailwinds for months and help explain the market’s resilience But above all of this looms one big storm: Tariffs The US has just imposed a 3.6% average tariff on China, a brand-new number post-negotiation

11/ Treasury officials say this 3.6% rate is just the floor We’re also looking at a 3.4% average global tariff, a 3.1% reciprocal baseline, and an extra 0.4% specifically on Canada and Mexico

12/ Yes, those numbers are lower than what many feared, but they still affect $2 trillion in trade That could shave off 1.5% from GDP For comparison, GDP fell by 3% during the Financial Crisis Tariffs may not cause a full-blown recession, but they’ll slow things down In our opinion, this reduces the odds of the V-shape recovery

13/ Just because a V-shape is unlikely doesn’t mean we’re going bearish At Bravos Research, we’ve been putting capital to work Our trades in BYD, gold, NRG, & ADMA have delivered double-digit gains recently Get real-time Trade Alerts at: <a target="_blank" href="https://go.bravosresearch.com/X" color="blue">go.bravosresearch.com/X</a>

14/ So if not a V-shaped recovery, does that mean we’re headed for a deeper drop? For that to happen, things need to get worse - economically or geopolitically History shows this kind of post-bounce breakdown has happened many times before

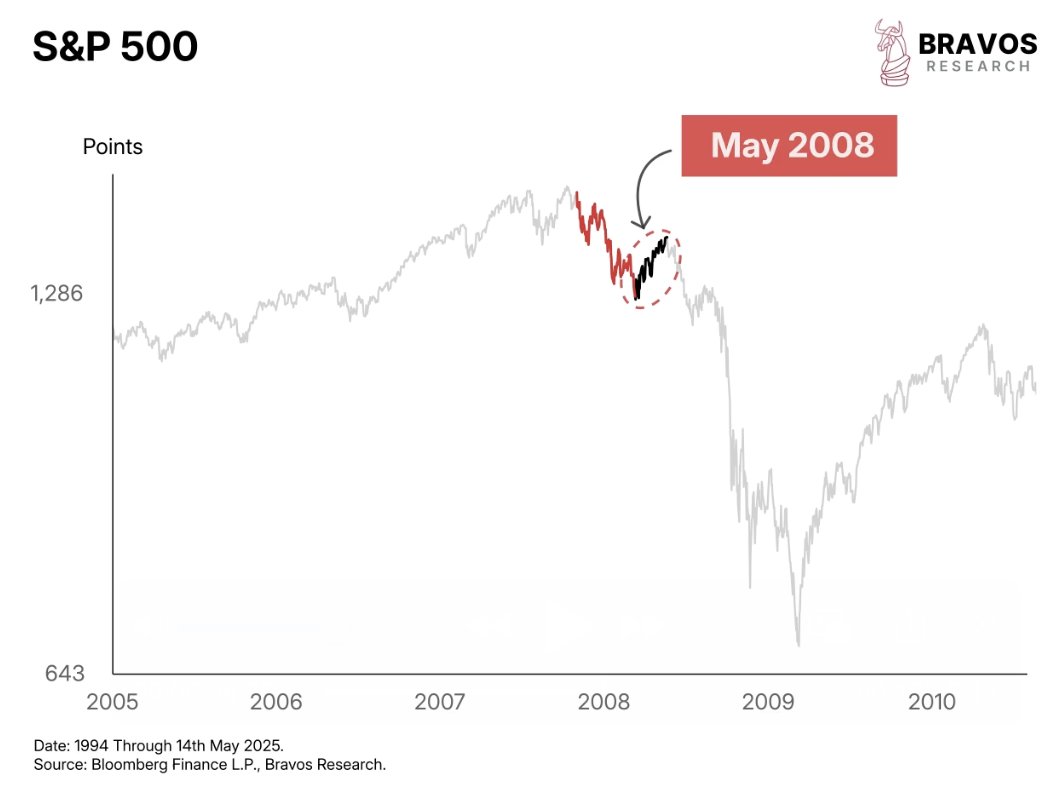

15/ In May 2008, stocks staged a rally after a sharp correction, but it didn’t last The market eventually broke to new lows and fell much further Similar failed rallies played out multiple times in 2001 as well

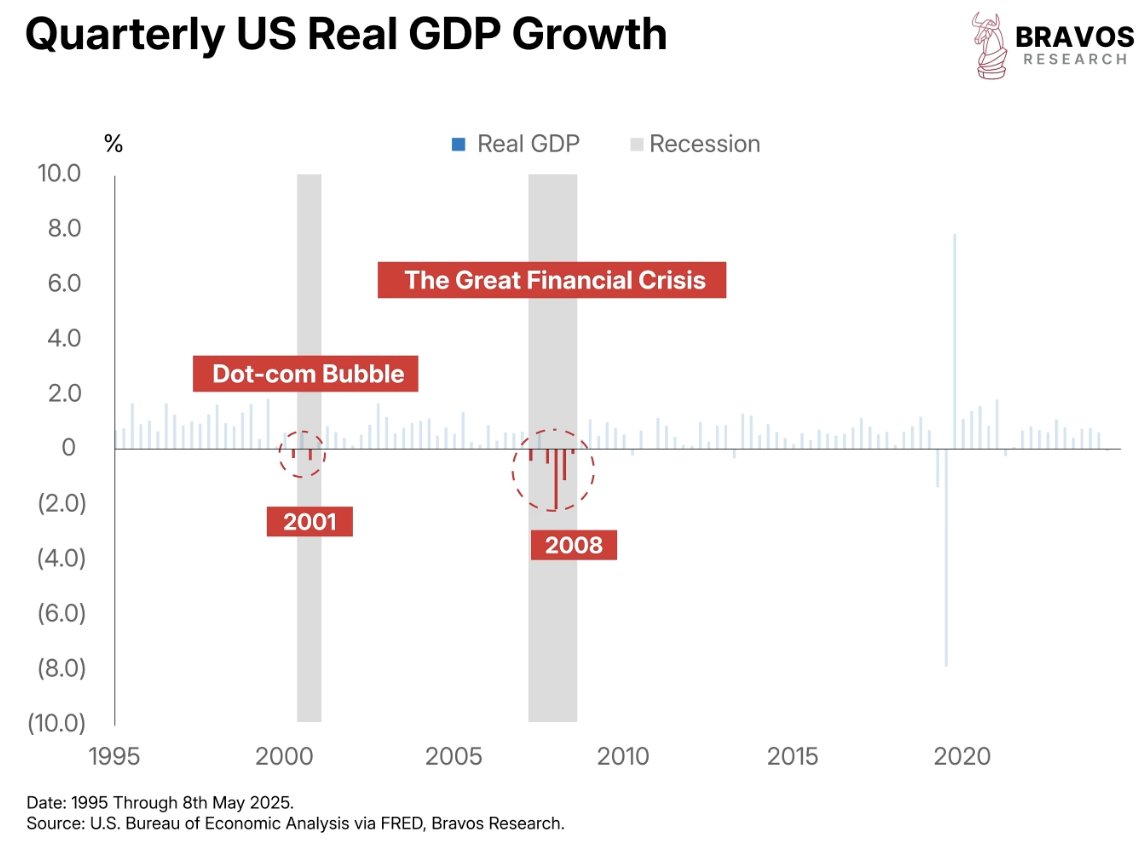

16/ If that happens again today, most people already know what that means It’s what everyone has been warning about since tariffs made headlines And the first red flag is already here: Q1 2025 posted a negative GDP print

17/ That’s exactly how things started in 2008 and 2001, both of which went on to become full-blown recessions In each case, the initial GDP contraction was followed by further contraction

18/ In both of those recessions, stocks dropped over 50% So if GDP keeps contracting, there’s a real risk that this year’s drawdown could just be the beginning of something bigger

19/ But we’ve also seen single-quarter GDP declines that didn’t lead to recessions Like we saw in 2022, 2014, and 2011 All were temporary slowdowns that turned into strong buying opportunities

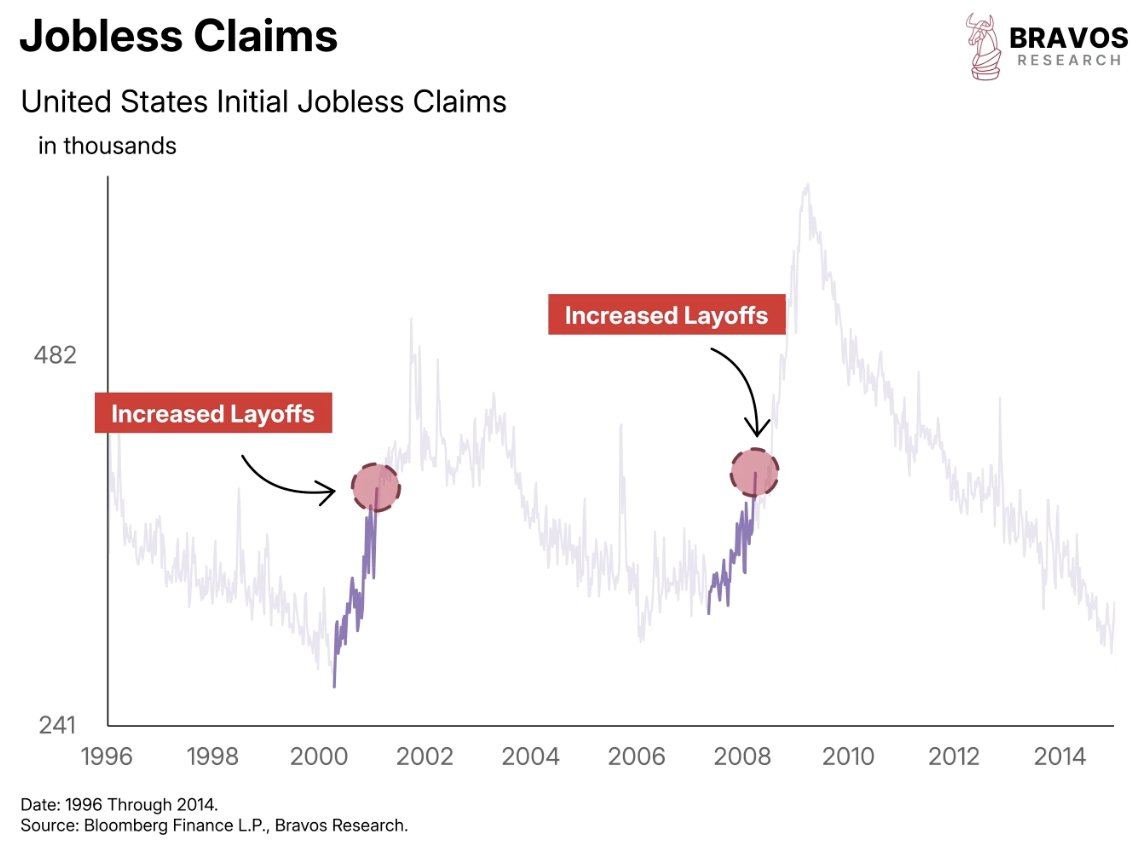

20/ What was the key difference between those isolated contractions and full-blown recessions? It was none other than the labor market In 2001 and 2008, initial jobless claims surged alongside the negative GDP prints Layoffs were clearly accelerating