Thread Truncated (Cap Enforced)

Only the first 20 tweets are unrolled into slides to ensure reliable PDF exporting and high server performance.

Canvas & Ratio

Choose your destination platform format

Layout Template

Choose a content structure for your slides

Preset Themes

Typography & Sizing

Brand Kit Customization

AGENCYConfigure brand assets for headers & footers

Outro Slide CTA

Customize your closing call-to-action slide

Background Pattern

Build Your Carousel

Drag and drop any post card below onto a slide, or use the quick buttons to insert content/images instantly!

A MAJOR fundamental flaw in crypto is starting to emerge. It's the #1 reason why altcoins are underperforming this cycle. And currently, there seems to be no fix. I just dug through all the data (what I found was shocking). 🧵: How altcoin dispersion is killing crypto.👇

The objective of this thread is to give you more insight into crypto's biggest issue. It will explain exactly how we got here, why prices are behaving the way they are, and the path forward.

Let me take you back to 2021. The market was in a frenzy. New liquidity was rapidly pouring into the market, mainly being driven by fresh retail. The bull market seemed unstoppable, and risk appetite was at its highest.

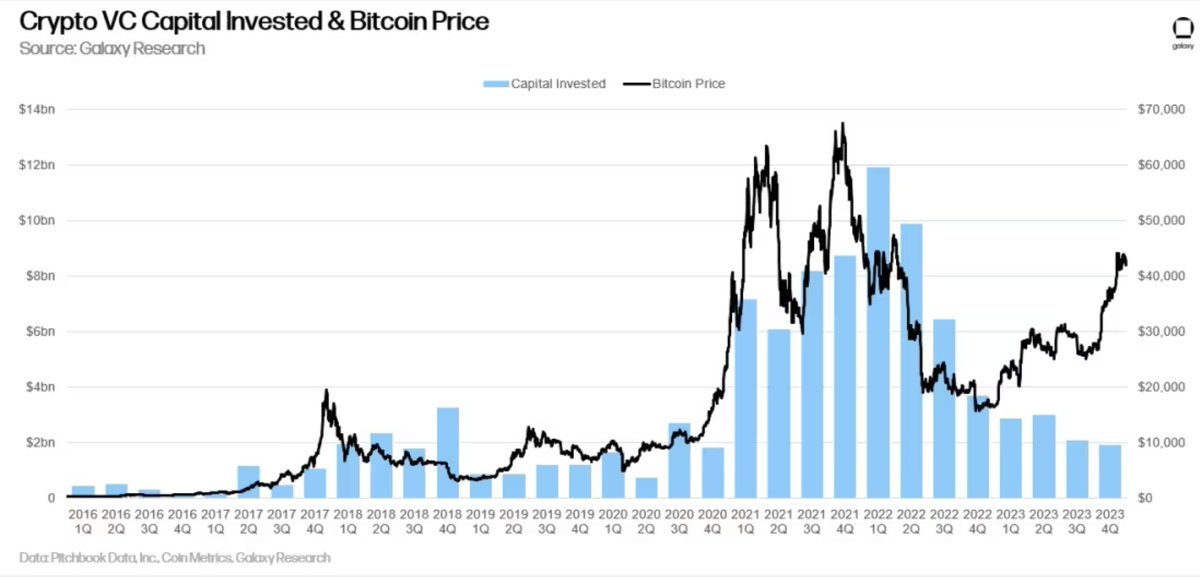

During this time, VCs started pouring unprecedented amounts of capital into the space. Founders & VCs are just like retail - they're opportunists. The uptick in investment was a natural capitalistic response to market conditions.

For those who don't understand private markets, put simply, a VC will invest capital into a project at an early stage (typically 6 months - 2 years prior to launch), at a typically lower valuation (with vesting attached).

This investment helps fund the project with capital to develop, with VCs also often providing other services/connections to help get a project off the ground.

Interestingly, the largest quarter EVER for VC funding ($12b) was Q1 2022. This marked the beginning of the bear (yes, VCs timed the top).

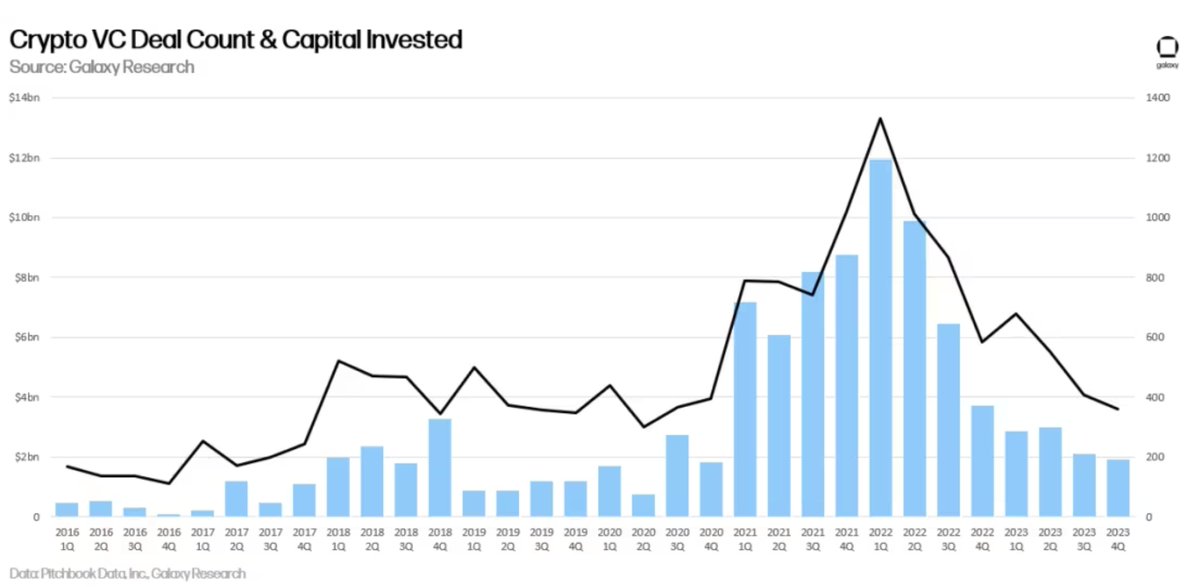

But remember, VCs are only investors. Increased deal count volume also comes from an increase in the amount of projects being created.

The low barriers to entry, combined with the high upside crypto presented in the bull market, made web3 a breeding ground for new startups. New tokens were popping up left right and centre, resulting in the total crypto token count tripling between 2021-2022.

But shortly after, the party stopped. A cascade of contagion, starting with LUNA, and ending with FTX, completely decimated the market.

So what did the projects do, that raised all that money earlier in the year? They delayed. And delayed. And delayed.

Launching a project in the midst of a bear is a death sentence. Low liquidity + bad sentiment + lack of interest means many new bear market launches were dead on arrival. So founders decided to wait for a reversal.

It took a while, but eventually - in Q4 2023, they got it. (remember, the biggest spike in VC funding was in Q1 2022, 18 months prior).

After months and months of delaying, they could FINALLY launch their tokens in better conditions. So they did. It started with one. And another, and another, and another.

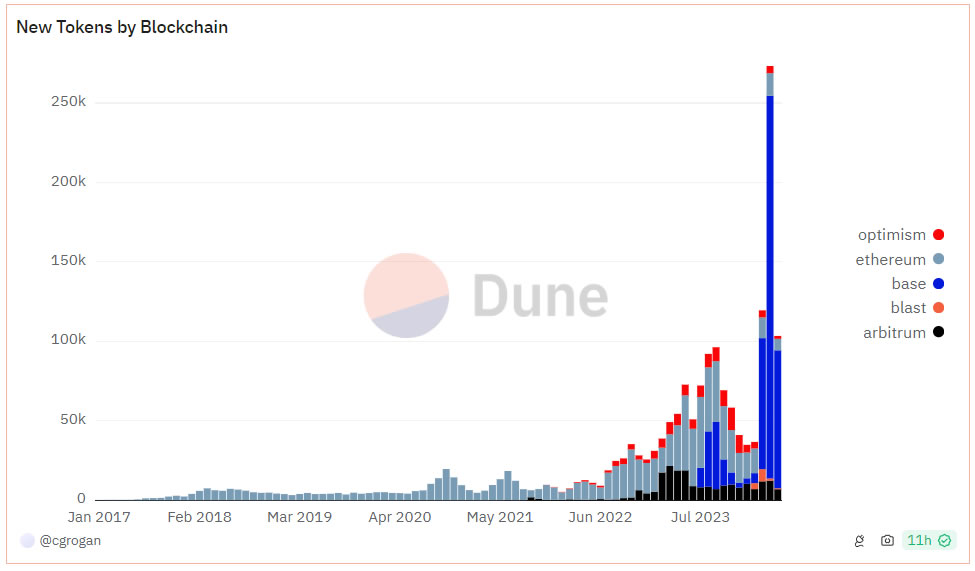

And it wasn't just the OLD projects deciding to launch. Many new players saw the new bullish conditions as an opportunity to launch a project and make a quick buck. As a result, 2024 has seen a historic number of new launches.

Here are the stats. They're crazy. Over 1 million new crypto tokens have been launched since April alone. (half of which are meme coins created on the Solana network).

You could argue that these numbers are inflated by the ease of deploying a meme on-chain. And that's true, yes. But it's still an insane figure. For a more accurate number, see the image below from CoinGecko, which excludes many of the smaller memes.

We now have 5.7 times the amount of crypto tokens than we did during peak bull in 2021.

This is a big problem. And is one of the major reasons why crypto has been struggling this year, despite $BTC hitting new ATHs. Why?

The more tokens that launch, the more cumulative supply pressure on the market. And this supply pressure "stacks". Many projects from 2021 are still unlocking, with supply "stacking" across every subsequent year (2022, 2023, 2024).