A slow-motion collapse is sweeping through commercial real estate.

Office buildings are vacant, mortgages are defaulting, cities are broke.

Taxpayers are quietly being lined up to take the fall.

(a thread)

It starts with debt. Landlords borrow money to buy buildings.

Those loans get bundled and sold to investors as bonds called CMBS, or Commercial Mortgage-Backed Securities.

If rent stops flowing in, those bonds start cracking.

Those loans get bundled and sold to investors as bonds called CMBS, or Commercial Mortgage-Backed Securities.

If rent stops flowing in, those bonds start cracking.

CMBS are sliced into layers, or tranches.

Top-rated ones get paid first. Lower-rated ones take losses first.

So when landlords fall behind, the bottom slices get hit fast and that’s what’s happening right now.

Top-rated ones get paid first. Lower-rated ones take losses first.

So when landlords fall behind, the bottom slices get hit fast and that’s what’s happening right now.

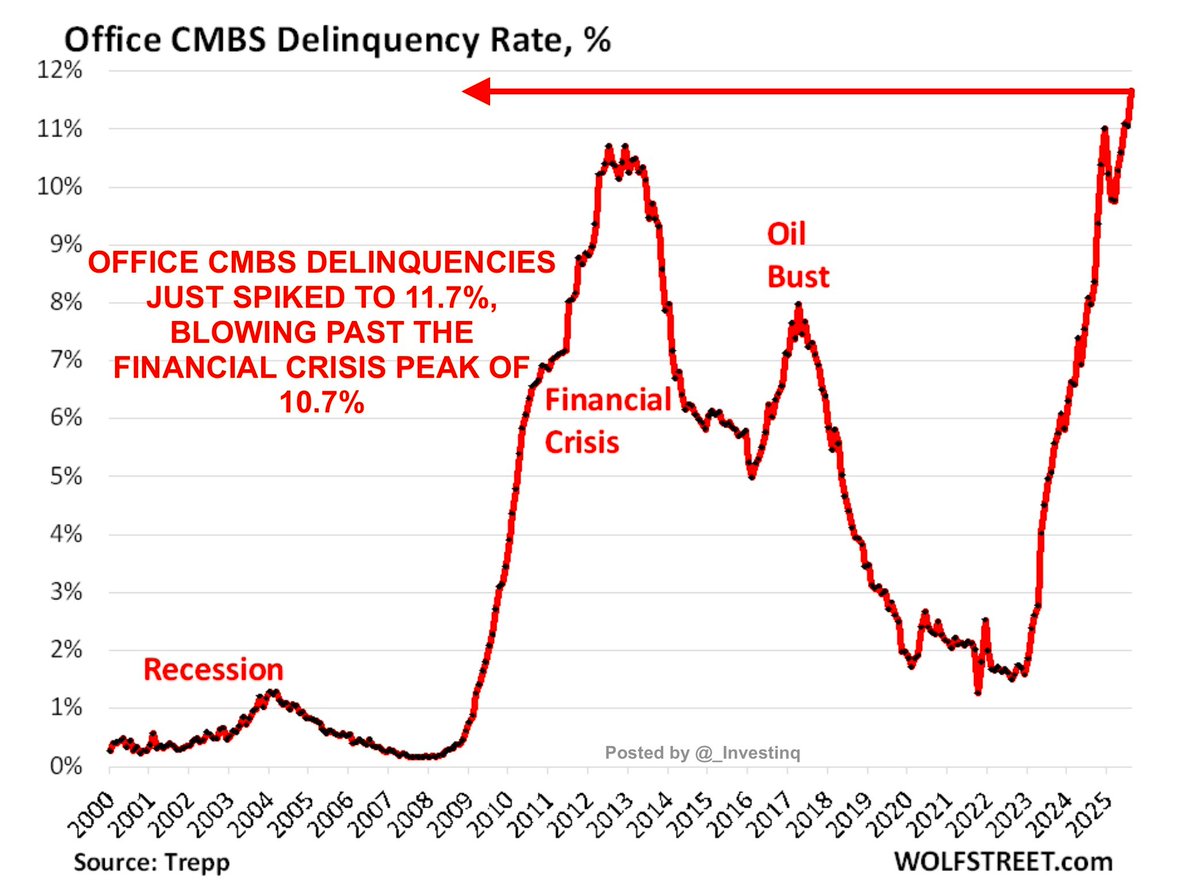

In August, 11.7% of all office CMBS loans were delinquent.

That means they’re late or not being paid at all.

It’s the highest delinquency rate ever recorded, even worse than 2008. Just 20 months ago, it was 1.6%.

That means they’re late or not being paid at all.

It’s the highest delinquency rate ever recorded, even worse than 2008. Just 20 months ago, it was 1.6%.

It’s not just small-time landlords.

Institutional giants like Brookfield and Pimco are walking away from towers. Why?

Because the math doesn’t work anymore. Too many buildings, too few tenants.

Institutional giants like Brookfield and Pimco are walking away from towers. Why?

Because the math doesn’t work anymore. Too many buildings, too few tenants.

Office demand collapsed.Vacancy rates in cities like SF, LA, and Chicago are above 30%.

Hybrid work is here to stay.

Companies realized they don’t need floors of space in downtown towers.

Hybrid work is here to stay.

Companies realized they don’t need floors of space in downtown towers.

Tenants who are leasing are upgrading. That shift is called “flight to quality.”

Newer towers steal demand from older ones.

Outdated buildings are left with no rent coming in and no buyers willing to take them on.

Newer towers steal demand from older ones.

Outdated buildings are left with no rent coming in and no buyers willing to take them on.

Interest rates are making this problem worse.

The Fed raised rates fast. Now borrowing is expensive, and buildings appraise for less.

A tower worth $500M in 2021 might only sell for $300M today. Lenders won’t refinance at that price.

The Fed raised rates fast. Now borrowing is expensive, and buildings appraise for less.

A tower worth $500M in 2021 might only sell for $300M today. Lenders won’t refinance at that price.

And we’ve hit the “maturity wall.” That’s when loans come due and need to be repaid or refinanced.

Over $2 trillion in commercial real estate loans mature by 2027. Nearly $1 trillion is due this year alone.

Most borrowers can’t roll over the debt.

Over $2 trillion in commercial real estate loans mature by 2027. Nearly $1 trillion is due this year alone.

Most borrowers can’t roll over the debt.

So what do they do? They stall. Example: 1211 Avenue of the Americas, NYC

• $1.04B mortgage

• Missed balloon payment in Aug

• Instead of foreclosing, lender gave a 3-year extension

This is called “extend and pretend.”

• $1.04B mortgage

• Missed balloon payment in Aug

• Instead of foreclosing, lender gave a 3-year extension

This is called “extend and pretend.”

Another tool: forbearance, a deal where the lender agrees not to collect payments for a while. Example: Times Square Plaza

• $335M loan

• Delinquent in 2024

• “Cured” in 2025 after the borrower injected $14M in cash and pledged $20M for repairs

• $335M loan

• Delinquent in 2024

• “Cured” in 2025 after the borrower injected $14M in cash and pledged $20M for repairs

Now it’s spreading to apartments.

Multifamily CMBS delinquencies jumped to 6.9% in August, the worst since 2015. Just two years ago, the rate was 1.8%.

These aren’t risky hotels or malls, they’re apartment buildings.

Multifamily CMBS delinquencies jumped to 6.9% in August, the worst since 2015. Just two years ago, the rate was 1.8%.

These aren’t risky hotels or malls, they’re apartment buildings.

Example: Park West Village, Manhattan

• $62M loan

• 850-unit complex

• Renovated in 2014, refinanced in 2022

• 30 days delinquent by August 2025

Even prime NYC apartments are missing payments.

• $62M loan

• 850-unit complex

• Renovated in 2014, refinanced in 2022

• 30 days delinquent by August 2025

Even prime NYC apartments are missing payments.

Delinquency leaderboard:

• Office CMBS: 11.7%

• Multifamily: 6.9%

• Lodging: 6.5%

• Retail: 6.4%

• Industrial: 0.6%

Industrial is still stable for now.

• Office CMBS: 11.7%

• Multifamily: 6.9%

• Lodging: 6.5%

• Retail: 6.4%

• Industrial: 0.6%

Industrial is still stable for now.

So who’s holding the bag? Office CMBS debt was sold off to the world.

Bond funds, insurance companies, mortgage REITs, private equity firms, they all own pieces.

Banks dumped most of it years ago.

Bond funds, insurance companies, mortgage REITs, private equity firms, they all own pieces.

Banks dumped most of it years ago.

But multifamily is different. It’s the largest part of commercial real estate, $2.2 trillion in debt.

And over half is backed by Fannie Mae, Freddie Mac, and local governments.

That means taxpayers are now exposed.

And over half is backed by Fannie Mae, Freddie Mac, and local governments.

That means taxpayers are now exposed.

Let’s break it down:

• 50%+ = government-backed

• 29% = banks & thrifts

• 12% = insurers

• 3% = CMBS or asset-backed securities

Multifamily risk is public. If defaults accelerate, the losses fall on the government and us.

• 50%+ = government-backed

• 29% = banks & thrifts

• 12% = insurers

• 3% = CMBS or asset-backed securities

Multifamily risk is public. If defaults accelerate, the losses fall on the government and us.

So no, this isn’t a banking crisis. It’s a taxpayer crisis in slow motion.

The Fed isn’t rushing to rescue it because banks aren’t holding the risk.

Investors and housing agencies are.

The Fed isn’t rushing to rescue it because banks aren’t holding the risk.

Investors and housing agencies are.

Meanwhile, cities are bleeding. Falling building values = falling property tax revenue.

That’s how cities fund basic services.

Boston is bracing for a $1.7B shortfall. San Francisco could lose $1B by 2028.

That’s how cities fund basic services.

Boston is bracing for a $1.7B shortfall. San Francisco could lose $1B by 2028.

This won’t collapse overnight but it doesn’t need to.

Every month, more loans mature. More buildings go delinquent. More cities hit budget walls.

It’s decay, one brick at a time.

Every month, more loans mature. More buildings go delinquent. More cities hit budget walls.

It’s decay, one brick at a time.

Generated by Thread Navigator

Press ⌘ + S to quick-export