The housing market has never been this unaffordable in U.S. history.

With inflation-adjusted home prices setting a record over the last three years.

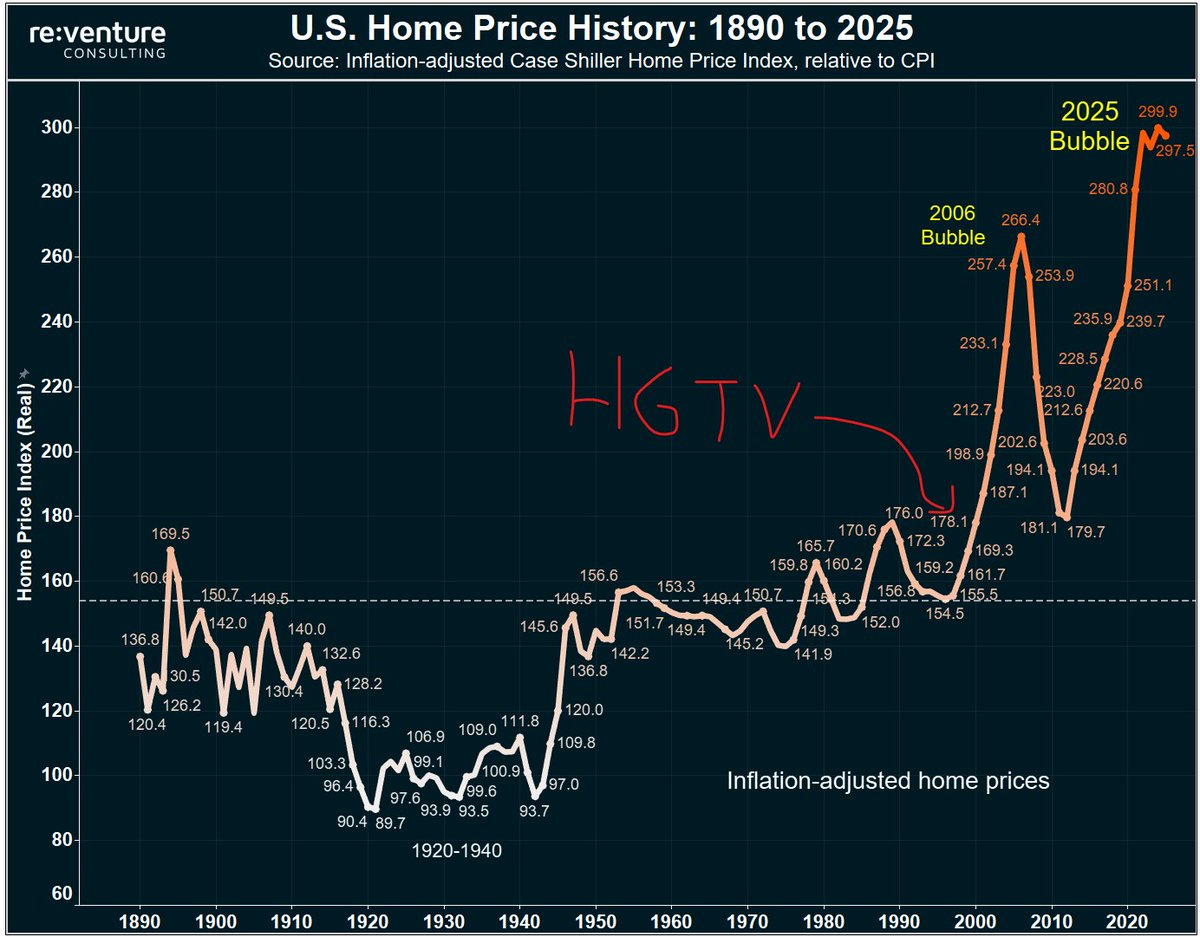

We're now in the biggest housing bubble of all-time, and the only period that came close was 2006, before the big crash.

Many people like to tell you "home values will never drop". But those people conveniently don't show you this graph.

There is no historical precedent for how expensive today's housing market it is.

And homebuyers know it.

1) What's extremely interesting is that home prices, for a very long time, simply tracked the rate of inflation.

More specifically, from 1890 to 1990, over 100 years, inflation-adjusted prices never went more than 15% above their long-term trend line.

More specifically, from 1890 to 1990, over 100 years, inflation-adjusted prices never went more than 15% above their long-term trend line.

2) The housing market in this era was stable and predictable. Prices never really boomed, outside of two inflation-driven episodes after WW2 and in the 1970s.

Meanwhile, prices never crashed, because values never became detached from the fundamentals.

Meanwhile, prices never crashed, because values never became detached from the fundamentals.

3) And it was in this period that many of the common narratives about the housing market were established.

"It's a good, stable investment".

"It grows at 3% per year".

"Buy a house as your nest egg".

All these things were true from 1890 to 1990.

But sometime in the mid-1990s, things changed.

"It's a good, stable investment".

"It grows at 3% per year".

"Buy a house as your nest egg".

All these things were true from 1890 to 1990.

But sometime in the mid-1990s, things changed.

4) The commoditization of the housing market started in this period, what I call the "HGTV-ification" of U.S. real estate.

Everyone suddenly wanted to become a home flipper and real estate investor.

And the idea of owning multiple homes and making a career out of real estate permeated the minds of working Americans for the first time.

Everyone suddenly wanted to become a home flipper and real estate investor.

And the idea of owning multiple homes and making a career out of real estate permeated the minds of working Americans for the first time.

5) So all of a sudden speculation took off.

And in the late 1990s, you saw the first real detachment of home prices from the rate of inflation.

Leading up to the 2006 housing bubble, where inflation-adjusted prices peaked at about 70% above the long-term historical average.

And in the late 1990s, you saw the first real detachment of home prices from the rate of inflation.

Leading up to the 2006 housing bubble, where inflation-adjusted prices peaked at about 70% above the long-term historical average.

6) Then you all know what happened next.

Prices crashed. They went down 25% in nominal terms across the U.S., and in certain markets prices dropped 60% during the big bust from 2007-12.

All in all, inflation-adjusted values declined by 33% over a six-year period.

Prices crashed. They went down 25% in nominal terms across the U.S., and in certain markets prices dropped 60% during the big bust from 2007-12.

All in all, inflation-adjusted values declined by 33% over a six-year period.

7) Some people like to blame bad mortgages for the bust that happened from 2007-12.

But the real culprit was the Federal Reserve.

In the early 2000s, they lowered the Fed Funds rate to 1.0%.

An unprecedentedly low level for peacetime. Dubbed the "Greenspan put", after then-Fed-chair Alan Greenspan, this aggressive rate-cutting set the stage for the next 20 years of Fed intervention in the U.S. economy and housing market.

But the real culprit was the Federal Reserve.

In the early 2000s, they lowered the Fed Funds rate to 1.0%.

An unprecedentedly low level for peacetime. Dubbed the "Greenspan put", after then-Fed-chair Alan Greenspan, this aggressive rate-cutting set the stage for the next 20 years of Fed intervention in the U.S. economy and housing market.

8) HGTV watchers used the low interest rate environment set by the Fed in the early 2000s to start buying up homes.

2nd homes, investment properties, and flip homes.

As many Americans started envisioning themselves making a career in real estate.

2nd homes, investment properties, and flip homes.

As many Americans started envisioning themselves making a career in real estate.

9) They of course used cheap and risky mortgages to fuel the bubble, and by 2006, prices were as much as 30-40% overvalued in many parts of the US Housing Market.

In a place like Florida, home values reached 30% overvaluation in March 2006, near the bubble peak.

A clear warning of what was to come.

In a place like Florida, home values reached 30% overvaluation in March 2006, near the bubble peak.

A clear warning of what was to come.

10) Nominal home prices in Florida then dropped by an astounding 50% from 2007-2012.

Meaning that a $300,000 house at peak became a $150,000 house.

Many people who bought near the peak lost everything, and most of the state went underwater on their mortgages.

Meaning that a $300,000 house at peak became a $150,000 house.

Many people who bought near the peak lost everything, and most of the state went underwater on their mortgages.

11) A similar story played out in states like Nevada, Arizona, California, Illinois, and Michigan.

Prices in these states all dropped by more than 30% in nominal terms during the last crash.

Prices in these states all dropped by more than 30% in nominal terms during the last crash.

12) Now many people in the housing market today try to claim another crash is impossible.

They say that the last downturn was purely a result of "bad mortgages".

And that strong underwriting standards today means a significant national downturn in home prices is impossible.

They say that the last downturn was purely a result of "bad mortgages".

And that strong underwriting standards today means a significant national downturn in home prices is impossible.

13) But if those people are right, it means that we're going to have a frozen housing market for the next decade, with extremely low buyer demand.

Because that's how long it's going to take for inflation and income growth to restore affordability, and make homebuyers feel like they can actually afford a house.

Because that's how long it's going to take for inflation and income growth to restore affordability, and make homebuyers feel like they can actually afford a house.

14) What makes a lot more intuitive sense to me is that we're going to see a national price correction.

Probably on the order of 15%.

Where homes get cheaper. This improved affordability will allow more homebuyers to step into the market.

Probably on the order of 15%.

Where homes get cheaper. This improved affordability will allow more homebuyers to step into the market.

15) At the same time, over multiple years, income and inflation will grow.

Making houses feel less expensive in relative terms.

Making houses feel less expensive in relative terms.

16) And that's ultimately the cocktail that is needed to restore this insane housing market to normalcy.

Homebuyers are boycotting, and on the sidelines.

They're not coming back until prices drop.

Homebuyers are boycotting, and on the sidelines.

They're not coming back until prices drop.

17) Of course, significant market-by-market variations exist.

Prices are already dropping in many parts of the U.S., and will drop further over the next 12 months.

To access my price forecasts for your area, go to my website reventure.app and sign up for a premium plan to see the areas I think are most exposed to a price downturn this year.

Prices are already dropping in many parts of the U.S., and will drop further over the next 12 months.

To access my price forecasts for your area, go to my website reventure.app and sign up for a premium plan to see the areas I think are most exposed to a price downturn this year.

Generated by Thread Navigator

Press ⌘ + S to quick-export