The most powerful investing principles I've ever learned are counterintuitive.

That’s logical - if they were intuitive, I wouldn't need to learn them.

Here are 7 counterintuitive investing principles I had to learn the hard with (with visuals)

1: Don’t haggle

If a stock is trading at $21, I used to set a limit order for $20.50

But my orders usually didn't fill.

Haggling caused me not to BUY a few mega-winners.

Which is FAR MORE costly than slightly overpaying.

If a stock is trading at $21, I used to set a limit order for $20.50

But my orders usually didn't fill.

Haggling caused me not to BUY a few mega-winners.

Which is FAR MORE costly than slightly overpaying.

Think of it this way:

If stock checks all your boxes and goes from $20 to $200

Does it matter if you got in at $19.56 or $21.25?

If you think a stock has 10x potential from today's price, don’t haggle over pennies.

Just buy it.

If stock checks all your boxes and goes from $20 to $200

Does it matter if you got in at $19.56 or $21.25?

If you think a stock has 10x potential from today's price, don’t haggle over pennies.

Just buy it.

2: Look for stocks that have ALREADY beaten the market.

It means the business model is working, AND Wall Street recognizes that it is working

It means the business model is working, AND Wall Street recognizes that it is working

Need "proof"? Look at Buffett!

$AAPL, $KO, $MCO, $AXP....

All of these were mega-winners for years BEFORE he bought them.

Fighting anchoring bias isn't easy, but it's essential.

$AAPL, $KO, $MCO, $AXP....

All of these were mega-winners for years BEFORE he bought them.

Fighting anchoring bias isn't easy, but it's essential.

3: Watch the business, not the stock

My instinct is to focus on the share price. That's what EVERYONE pays attention to.

I’ve since learned that stock price movements are random. In the short term, they do not correlate to the business.

My instinct is to focus on the share price. That's what EVERYONE pays attention to.

I’ve since learned that stock price movements are random. In the short term, they do not correlate to the business.

In the long-term, they are 100% correlated to the business.

I now focus my time on the business, not the stock.

I now focus my time on the business, not the stock.

4: The P/E ratio IS NOT universally applicable.

When I first learned about the P/E ratio, it just made sense.

It became the yardstick by which I judged ALL companies.

When I first learned about the P/E ratio, it just made sense.

It became the yardstick by which I judged ALL companies.

I’ve since learned that the P/E ratio IS NOT a universally applicable metric.

It's A metric -- not THE ONLY metric that matters.

You need to know:

1: When it’s useful (Phase 4 & 5)

2: When IT SHOULD BE IGNORED (Phase 1, 2, 3, & 6)

It's A metric -- not THE ONLY metric that matters.

You need to know:

1: When it’s useful (Phase 4 & 5)

2: When IT SHOULD BE IGNORED (Phase 1, 2, 3, & 6)

5: If you’re right 50% of the time, you’re system is WORKING.

My instinct was that 50% of stocks beat the market and 50% lose.

Therefore, an accuracy rate of 60% was needed to outperform.

My instinct was that 50% of stocks beat the market and 50% lose.

Therefore, an accuracy rate of 60% was needed to outperform.

A JP Morgan study from 1980-2014 showed that:

✔️Only 36% of stocks beat the market

✔️Only 7% of stocks accounted for nearly ALL the index's gains

This means that the odds of picking a winner are not a coin flip - they are more like a dice roll.

✔️Only 36% of stocks beat the market

✔️Only 7% of stocks accounted for nearly ALL the index's gains

This means that the odds of picking a winner are not a coin flip - they are more like a dice roll.

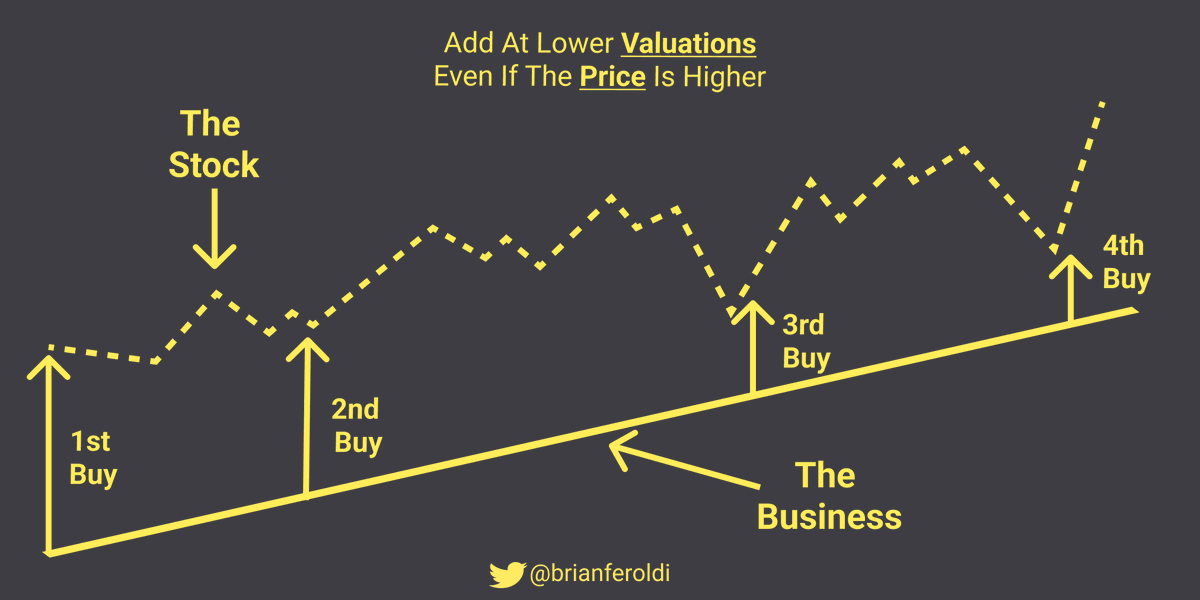

6: Add at lower VALUATIONS, not just lower PRICES

My instinct is to double down on my losers.

If I liked a stock at $20, and the price is now $10, I should buy more, right?

Not necessarily…Is the BUSINESS better or worse? That's what matters!

My instinct is to double down on my losers.

If I liked a stock at $20, and the price is now $10, I should buy more, right?

Not necessarily…Is the BUSINESS better or worse? That's what matters!

I’ve since learned that I shouldn’t try and focus on buying at lower PRICES.

I should focus on buying at lower VALUATIONS.

I should focus on buying at lower VALUATIONS.

7: Low Valuation ≠ Undervalued

High Valuation ≠ Overvalued

@morganhousel wrote an eye-opening article in 2013

He looked at the Dow stocks in 1995 and asked: What P/E ratio did you need to pay to earn an 8% CAGR by 2012?

This table summarizes the results:

High Valuation ≠ Overvalued

@morganhousel wrote an eye-opening article in 2013

He looked at the Dow stocks in 1995 and asked: What P/E ratio did you need to pay to earn an 8% CAGR by 2012?

This table summarizes the results:

@morganhousel The findings:

✔️Many high-valuation stocks were UNDERVALUED

✔️Many low-valuation stocks were OVERVALUED

This article (plus experience) has taught me:

1: High-quality businesses deserve to trade at a premium

2: Low-quality businesses deserve to trade at a discount

✔️Many high-valuation stocks were UNDERVALUED

✔️Many low-valuation stocks were OVERVALUED

This article (plus experience) has taught me:

1: High-quality businesses deserve to trade at a premium

2: Low-quality businesses deserve to trade at a discount

@morganhousel To summarize:

1: Don’t haggle

2: Find stocks that are already up big

3: Watch the business, not the stock

4: P/E isn't universally applicable

5: The odds aren't a coin flip

6: Add at better value points, not just better prices

7: Low Valuation ≠ Undervalued

1: Don’t haggle

2: Find stocks that are already up big

3: Watch the business, not the stock

4: P/E isn't universally applicable

5: The odds aren't a coin flip

6: Add at better value points, not just better prices

7: Low Valuation ≠ Undervalued

@morganhousel If this thread was helpful follow me @BrianFeroldi.

I teach investor how to analyze businesses.

Want to share it with your audience? ♻️ Retweet the first tweet below:

I teach investor how to analyze businesses.

Want to share it with your audience? ♻️ Retweet the first tweet below:

View Tweet

Generated by Thread Navigator

Press ⌘ + S to quick-export