Get ready for a wild day:

A massive $4.7 TRILLION worth of options are expiring today, based on notional value.

This includes a whopping $2.8 trillion of S&P 500 options and $645 billion of single stock options.

What does it mean? Let us explain.

(a thread)

Total notional value refers to the to the combined value of all underlying assets that a set of options contracts controls.

Some estimates put it as high as $4.7 TRILLION today.

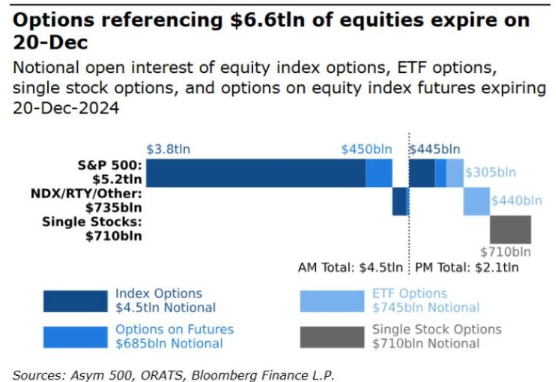

This is the biggest OpEx since December 20, when $6.6 trillion of options expired, as seen below.

Some estimates put it as high as $4.7 TRILLION today.

This is the biggest OpEx since December 20, when $6.6 trillion of options expired, as seen below.

Here's a breakdown of the distribution in strike price for the S&P 500 options.

This represents $2.8 trillion of options with a spot value of 5675.

The sheer volume of these options is expected to cause significant volatility in the index over the course of today's session.

This represents $2.8 trillion of options with a spot value of 5675.

The sheer volume of these options is expected to cause significant volatility in the index over the course of today's session.

Options expiring today represent a notional value that is equal to 8.2% of the Russell 3000's market cap.

While not as large as the ~9.3% seen in December 2024, it's the second largest since June 2024.

This also comes at a time where market volatility has been elevated.

While not as large as the ~9.3% seen in December 2024, it's the second largest since June 2024.

This also comes at a time where market volatility has been elevated.

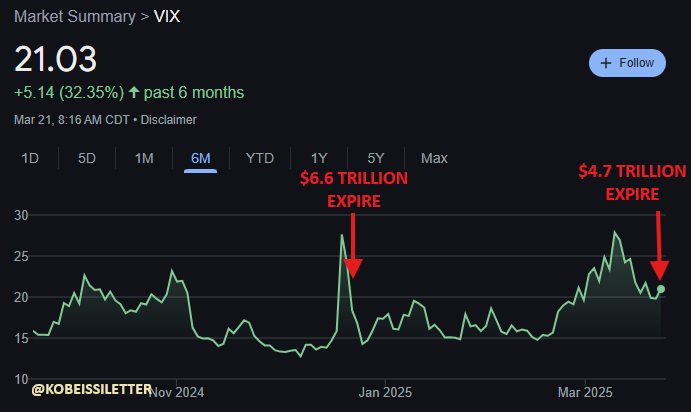

As seen below, we also saw a large runup in the Volatility Index, $VIX, in the lead up to the December 20th $6.6T expiration.

This came amid the fading "Santa Claus" rally as stocks pulled back into year-end.

Again, we see the $VIX rising today and remaining elevated.

This came amid the fading "Santa Claus" rally as stocks pulled back into year-end.

Again, we see the $VIX rising today and remaining elevated.

Take a look at the distribution of puts vs calls in today's OpEx, per SpotGamma.

We generally see more put exposure across the board.

Single stocks options are ~54% puts and S&P 500 options are ~68% puts.

Could this ultimately lead to a short squeeze into the close?

We generally see more put exposure across the board.

Single stocks options are ~54% puts and S&P 500 options are ~68% puts.

Could this ultimately lead to a short squeeze into the close?

Interestingly, this is COMPLETELY different than what we saw in December 2024.

Leading into the December 20th OpEx, the call to put ratio was 10 to 1.

However, the S&P 500 ended up closing +1.1% higher on December 20th.

Therefore, polarized positioning doesn't always flip.

Leading into the December 20th OpEx, the call to put ratio was 10 to 1.

However, the S&P 500 ended up closing +1.1% higher on December 20th.

Therefore, polarized positioning doesn't always flip.

Today is also a "triple witching day" which means options linked to stocks will expire alongside major stock index futures contracts.

As seen below, triple witching days over the last 10 years have generally seen negative returns.

More reason to expect heightened volatility.

As seen below, triple witching days over the last 10 years have generally seen negative returns.

More reason to expect heightened volatility.

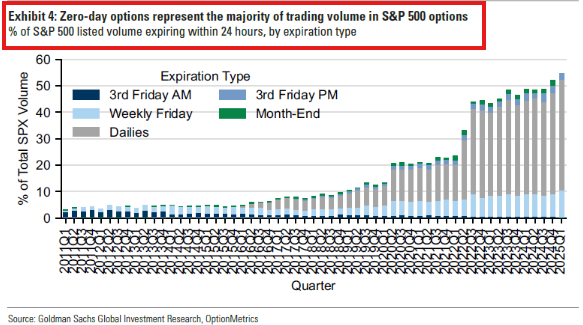

Lastly, today's OpEx comes at a time where total options volume has exploded.

We are now seeing close to 70 million contracts traded on a 5-day average.

Prior to 2020, we had never seen this metric break above 35 million, or half of the levels markets are seeing now.

We are now seeing close to 70 million contracts traded on a 5-day average.

Prior to 2020, we had never seen this metric break above 35 million, or half of the levels markets are seeing now.

The continued volatility in this market is a gift to traders.

We continue to capitalize on the large swings and trend reversals.

Want to see how we are trading it?

Subscribe now at the link below to access our premium analysis and alerts:

thekobeissiletter.com/subscribe

We continue to capitalize on the large swings and trend reversals.

Want to see how we are trading it?

Subscribe now at the link below to access our premium analysis and alerts:

thekobeissiletter.com/subscribe

According to Goldman Sachs, 0DTE options now reflect 55% of all option volume.

In other words, the MAJORITY of options are now expiring the same day they are purchased.

Prepare for significant volatility.

Follow us @KobeissiLetter for real time analysis as this develops.

In other words, the MAJORITY of options are now expiring the same day they are purchased.

Prepare for significant volatility.

Follow us @KobeissiLetter for real time analysis as this develops.

Generated by Thread Navigator

Press ⌘ + S to quick-export