Statistical Arbitrage is the strategy Ed Thorpe used to grow his net worth to $800 million.

Here's how to build a stat arb trading strategy with factor adjustments (Python code):

1. Select Assets and Gather Data

Choose a basket of correlated assets (e.g., financial stocks) and collect their price data, plus a market index (e.g., S&P 500) as the factor.

Choose a basket of correlated assets (e.g., financial stocks) and collect their price data, plus a market index (e.g., S&P 500) as the factor.

2. Estimate Factor Exposures (Betas)

Run a rolling regression for each stock against the market to calculate its beta, representing its sensitivity to the market factor.

Run a rolling regression for each stock against the market to calculate its beta, representing its sensitivity to the market factor.

3. Adjust for Factor Exposure

Subtract the market’s contribution (beta × market return) from each stock’s return to isolate idiosyncratic (residual) returns, then compute z-scores.

Subtract the market’s contribution (beta × market return) from each stock’s return to isolate idiosyncratic (residual) returns, then compute z-scores.

4. Generate Trading Signals

Identify mispricings by comparing each stock’s residual z-score to the portfolio value. Trade when deviations exceed thresholds.

Identify mispricings by comparing each stock’s residual z-score to the portfolio value. Trade when deviations exceed thresholds.

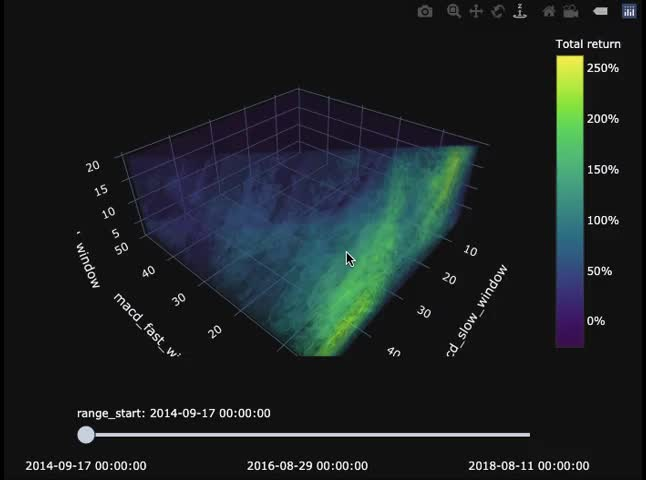

5. Backtest and Deploy

Calculate strategy returns using the original stock returns (since trades are on stocks, not residuals), then evaluate and deploy.

Calculate strategy returns using the original stock returns (since trades are on stocks, not residuals), then evaluate and deploy.

6. Want to learn how to get started with algorithmic trading with Python?

Then join us on March 5th for a live webinar, how to Build Algorithmic Trading Strategies (that actually get results)

Register here (780+ registered): learn.quantscience.io/qs-register

Then join us on March 5th for a live webinar, how to Build Algorithmic Trading Strategies (that actually get results)

Register here (780+ registered): learn.quantscience.io/qs-register

Generated by Thread Navigator

Press ⌘ + S to quick-export