US banks liquidity preferences can derail QT.

FED rate hiking cycle + regional bank deterioration have changed banks’ overnight liquidity preferences which will force the FED to keep a larger BS than intended.

3 reasons banks are currently demanding ⬆️o/n liquidity.

A 🧵

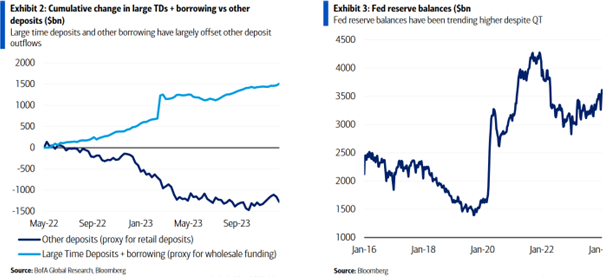

Banks have opted to hold more liquidity by tapping expensive funds (time deposits, CDs, other termed borrowing). This means that FED will be unable to shrink its BS much further. As RRP declines & reserve balances trend higher, Fed will proceed carefully with QT & liquidity drain

Reason 1:

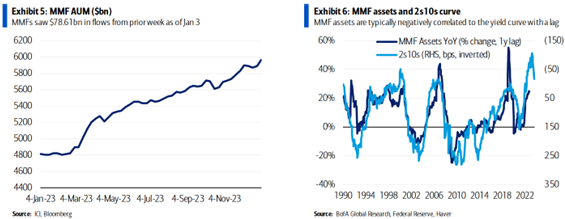

Deposit exodus from banks to MMFs has weakened regional banks. Best antidote is holding lots of overnight liquidity. Over week of Jan 5 MMF AUM increased $44bn with inflows primarily into govt & prime retail MMFs. Expect ongoing MMF inflows with an inverted yield curve.

Deposit exodus from banks to MMFs has weakened regional banks. Best antidote is holding lots of overnight liquidity. Over week of Jan 5 MMF AUM increased $44bn with inflows primarily into govt & prime retail MMFs. Expect ongoing MMF inflows with an inverted yield curve.

Reason 2:

Banks are still sitting on unrealized losses on treasury and mortgage bonds. Recent rate rally has helped but issue isn't gone. Best way to fight this is to hold cash because banks can say: don't worry about the 2.5% mortgage, I don’t have to sell for liquidity purposes

Banks are still sitting on unrealized losses on treasury and mortgage bonds. Recent rate rally has helped but issue isn't gone. Best way to fight this is to hold cash because banks can say: don't worry about the 2.5% mortgage, I don’t have to sell for liquidity purposes

Reason 3:

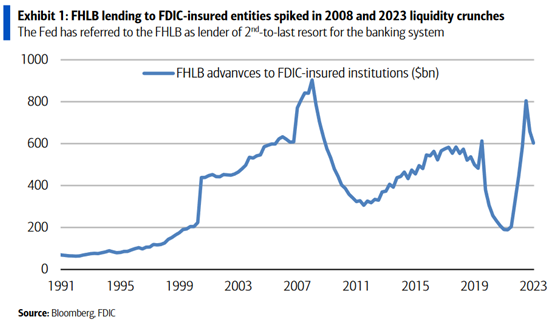

Banks perceive that some rules of liquidity management (role of Federal Home Loan Banks). Regulators will take steps to ⬆️preparedness for discount window usage. FHLB usage can decline as regulators attempt to limit the bank’s dependence on FHLB as a liquidity provider.

Banks perceive that some rules of liquidity management (role of Federal Home Loan Banks). Regulators will take steps to ⬆️preparedness for discount window usage. FHLB usage can decline as regulators attempt to limit the bank’s dependence on FHLB as a liquidity provider.

The question is: will the FED slow down or stop QT in time to accommodate overnight liquidity needs, or will they risk another funding market sharp jump like the incident seen during September 2019?

Generated by Thread Navigator

Press ⌘ + S to quick-export