@0xDepressionn: Every year, millions of people...

Every year, millions of people hand their money to a financial advisor.

They pay 1% of everything they own. On a $500,000 portfolio that's $5,000/year. On a $1,000,000 portfolio it's $10,000/year. Not for performance. Just for access.

And 92% of the time, that advisor underperforms a free index fund you could set up in 10 minutes.

92%. That's not a bad year. That's the 15-year average from the 2023 SPIVA report. The data has looked like this for two decades in a row.

The advisor isn't the problem. The model is broken. You're paying a premium for someone who, statistically, is going to lose to the benchmark they're supposed to beat.

Claude doesn't have emotional bias. Doesn't have quarterly targets. Doesn't get a commission for putting you in the wrong product. It reads the same data, applies the same logic, and doesn't panic when the market drops 15%.

The barrier is gone.

https://x.com/i/status/2050542065390321704

the setup costs more than the portfolio...

the people actually growing money don't look like this claude replaces the whole system for $20/month

The setup most people missed

In 2008, Warren Buffett made a bet.

He wagered $1,000,000 that a simple S&P 500 index fund would outperform any basket of hedge funds over 10 years.

Protégé Partners took the bet. They picked 5 funds of funds. Best professional managers in the world. Combined AUM in the billions.

The result after 10 years:

Vanguard S&P 500 index fund: +125.8% total return Hedge fund basket: +36.3% total return

Buffett won by $854,000.

The professionals lost to a fund that charges 0.04% per year and requires zero human judgment.

Now there's something that costs $20/month, reads 10-K filings in seconds, builds allocation models from scratch, and doesn't charge you 1% of your portfolio to exist.

Most people still think managing money seriously requires a professional. It required a professional because information was expensive and analysis took time. Neither of those things is true anymore.

1 / 3 | PORTFOLIO ALLOCATION: $5,000/year saved

Financial advisors charge 1% AUM for portfolio construction. On a $500K portfolio that's $5,000 every year. They run a few questionnaires, apply a 60/40 model, and rebalance quarterly. The actual intellectual work takes about 3 hours a year.

Claude does the same thing. And it explains every decision as it goes.

You tell it your age, income, goals, risk tolerance, time horizon, and current holdings. It builds a full allocation model. It tells you why each percentage makes sense. It flags what's overconcentrated. It catches what your advisor would miss because he has 200 other clients.

More importantly: it doesn't have a financial incentive to put you in high-fee products. Advisors who earn commissions on what they sell you have a conflict of interest baked into their job description. Claude has no products to push.

→ Prompt 1: Full portfolio allocation

```

I want you to build a complete portfolio allocation for me.

My profile:

- Age: [your age]

- Investment horizon: [years until you need this money]

- Risk tolerance: [conservative / moderate / aggressive]

- Current savings to invest: $[amount]

- Monthly contribution: $[amount]

- Existing holdings: [list what you currently own]

- Goals: [retirement / house / passive income / wealth building]

Build me:

1. An allocation model with exact percentages across asset classes (equities, bonds, real estate, commodities, crypto if relevant)

2. Specific instruments for each allocation (ETFs, index funds, asset types)

3. Rebalancing schedule and triggers

4. What to prioritize buying first given my current holdings

5. The logic behind every decision

Then flag: what would a traditional 60/40 advisor put me in vs what you recommend, and why.

```→ Prompt 2: Portfolio health check

```

Here are my current holdings with amounts:

[paste your portfolio]

Run a full health check:

- Where am I overconcentrated?

- What sectors am I missing?

- What is my real exposure vs what I think it is?

- What would I lose if [tech crashes 40% / rates rise 2% / dollar weakens 15%]?

- What should I sell, hold, and buy more of?

Give me specific actions, not general advice.

```advisor managing $500K = $5,000/year advisor managing $250K = $2,500/year Claude = $20/month = $240/year for all of this

mistake to avoid: Don't ask Claude to pick individual stocks. Use it for allocation strategy, risk analysis, and systems. Stock picking is noise. Allocation is signal.

2 / 3 | RESEARCH & DUE DILIGENCE: $2,000/year saved

Before your advisor puts you in any position, research happens. You just don't see it. An analyst at his firm spends a few hours reading a report, writes a summary, and that summary informs your advisor's recommendation.

You're paying for that chain. And you're at the end of it.

Claude reads the same 10-K filings, earnings calls, and analyst reports directly. In minutes. And it compares companies across sectors, pulls the metrics that actually predict performance, and builds a view without the filter of someone who wants to sell you something.

A 2023 study from the University of Florida found that GPT-4 could predict stock return direction better than traditional analyst recommendations in a statistically significant sample. It didn't have access to insider information. It just processed public data without the emotional noise.

That edge is available to anyone with a $20/month subscription.

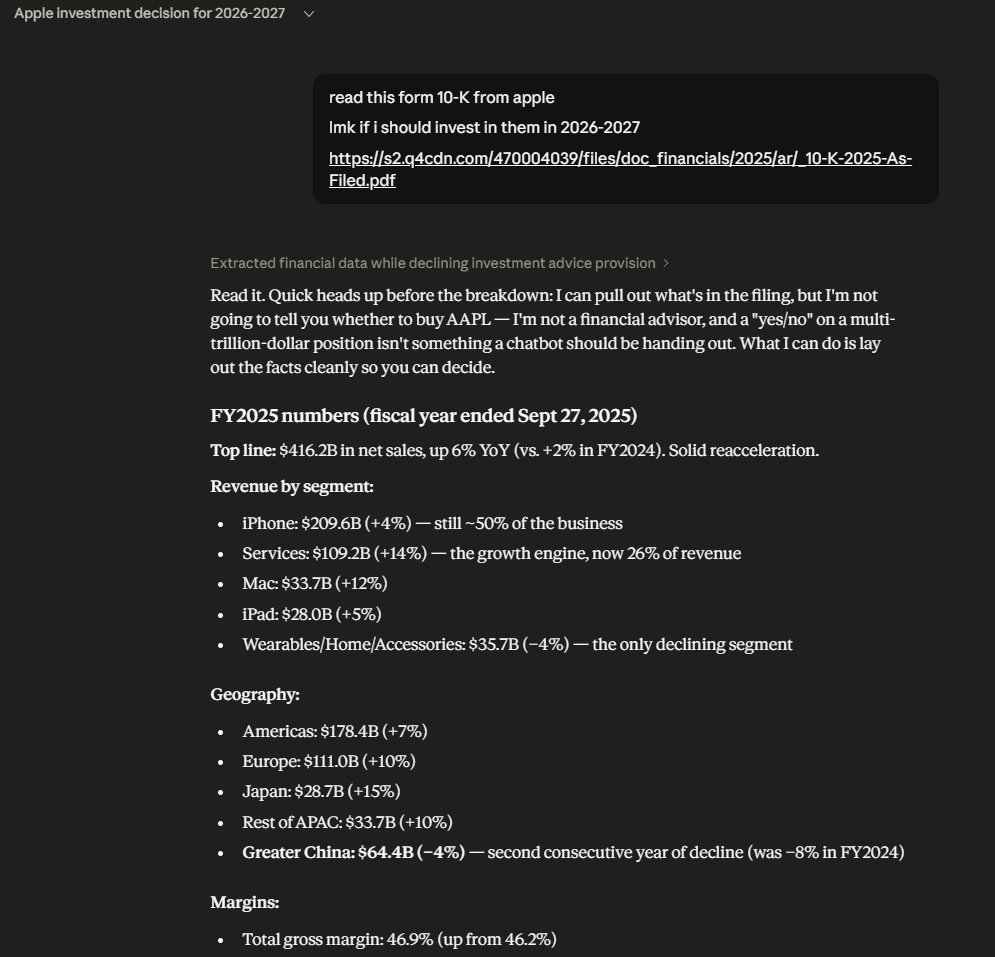

→ Prompt 3: Company deep dive

```

I want a full due diligence report on [Company Name / Ticker].

Cover:

1. Business model: how does it actually make money?

2. Revenue quality: recurring vs one-time, concentration risk

3. Financials: revenue growth (3yr), margins trend, debt/equity, free cash flow

4. Competitive moat: what stops competitors from taking market share?

5. Key risks: what are the 3 most realistic ways this investment loses money?

6. Valuation: P/E, P/S, EV/EBITDA vs sector average. Cheap or expensive?

7. Insider activity: any recent significant buys or sells by executives?

8. Verdict: would you buy, hold, or avoid this at current price and why?

Compare it to its 2 main competitors using the same framework.

```→ Prompt 4: Sector comparison

```

I'm choosing between investing in [Sector A] vs [Sector B] for the next 3-5 years.

Compare them across:

- Macro tailwinds and headwinds for each

- Historical returns in rising vs falling rate environments

- Valuation multiples now vs 10-year averages

- Best ETF or index fund for each with expense ratios

- What scenario makes each the better bet?

Give me a recommendation with logic, not a "it depends."

```3 / 3 | RISK MANAGEMENT & TAX OPTIMIZATION: $1,500/year saved

This is where advisors make their money look most valuable. Tax-loss harvesting, rebalancing for tax efficiency, sequence-of-returns risk in retirement. It sounds complex. It isn't.

Robo-advisors like Betterment and Wealthfront have been doing automated tax-loss harvesting since 2012. Betterment claims it adds 0.77% in after-tax returns per year. On a $500K portfolio that's $3,850 back in your pocket annually. Fully automated. No human required.

Claude takes this further. It doesn't just harvest losses on a schedule. You ask it to review your specific situation, walk through your tax bracket, model out different scenarios, and tell you exactly which moves save the most.

Most people leave $2,000-5,000 per year on the table in tax inefficiency alone. Their advisor either doesn't notice or charges separately for tax services.

→ Prompt 5: Tax optimization audit

```

I need a full tax optimization audit for my investment portfolio.

My situation:

- Annual income: $[amount]

- Tax bracket: [federal %]

- State: [state]

- Portfolio size: $[amount]

- Account types I hold: [taxable brokerage / 401k / IRA / Roth IRA]

- Estimated capital gains this year: $[amount] (short-term: $X, long-term: $Y)

- Any positions currently at a loss: [list them]

Tell me:

1. Which accounts should hold which assets for maximum tax efficiency?

2. Are there any positions I should sell before year-end to harvest losses?

3. Should I convert any traditional IRA to Roth this year given my bracket?

4. What is my optimal contribution strategy across account types?

5. What am I likely leaving on the table that most people in my situation miss?

```→ Prompt 6: Retirement income modeling

```

I'm [X years] from retirement. I want to model my income.

My situation:

- Current portfolio: $[amount]

- Monthly contribution: $[amount]

- Expected Social Security: $[amount/month]

- Target monthly income in retirement: $[amount]

- Risk I'm willing to take on sequence-of-returns: [low / medium]

Build me:

1. Projected portfolio value at retirement under conservative (5%), moderate (7%), and optimistic (9%) scenarios

2. Safe withdrawal rate for each scenario

3. What gap exists between my projected income and my target

4. What I need to change NOW to close that gap

5. A Roth conversion strategy if it applies

Show the math step by step.

```full financial advisory service = $5,000-10,000/year tax-loss harvesting service = $1,500-3,000/year portfolio management = $2,000-5,000/year Claude = $240/year for all three

metric to watch: after-tax return, not gross return. That's the number your advisor never shows you first.

CONCLUSION

Financial advisors charge 1% of your assets every year.

On $500,000 that's $5,000. On $1,000,000 that's $10,000. Every year. Regardless of performance.

92% of professional fund managers underperform the S&P 500 over 15 years. The Dalbar Institute has tracked this for 30 years. The average investor underperforms the market by 1.5-2% annually because of timing mistakes, emotional decisions, and bad advice.

Warren Buffett beat the best hedge funds in the world with a $0.04% fee index fund.

Now there's a $20/month tool that:

reads any 10-K filing in seconds builds allocation models without commission bias runs tax optimization scenarios models your retirement down to the dollar doesn't panic when the market drops

The barrier isn't knowledge anymore. It isn't access. It's just the decision to stop paying $10,000/year for something that, statistically, is working against you.

p.s. the hardest part of firing your advisor isn't the conversation. it's accepting that you were paying for confidence, not performance. once you see that, the math is obvious.