@Brad_Setser: The latest IMF analysis of Chi...

@Brad_Setser

21 views

Feb 28, 2026

1

The latest IMF analysis of China (The staff report/ Article IV) highlights that China's export driven growth has come at the expense of its trading partners.

That is welcome, and very necessary message

1/many

That is welcome, and very necessary message

1/many

2

James Mayger and Jorgelina Do Rosario of Bloomberg reminded me that the 2024 staff report didn't mention external imbalances at all -- so there has been an important evolution in the IMF's thinking in the last couple of years

2/

bloomberg.com/news/articles/…

2/

bloomberg.com/news/articles/…

3

The IMF's fiscal policy advice has also shifted. back in the summer of 2024, the Fund was pushing for the rapid initiation of a big fiscal consolidation. Not anymore

3/

3/

4

It is subtle, but the IMF also caveated its continued call for monetary easing in an important way in para 35:

"monetary loosening should be considered only as a part of a broader policy package that ensures a reduction in both the domestic and external imbalances and reflates the economy. Monetary easing in isolation could result in unwarranted further real exchange rate depreciation"

4/

"monetary loosening should be considered only as a part of a broader policy package that ensures a reduction in both the domestic and external imbalances and reflates the economy. Monetary easing in isolation could result in unwarranted further real exchange rate depreciation"

4/

5

I very much appreciate this shift; back in 2024 the IMF's policy advice was basically to use monetary easing and net exports (via a weaker exchange rate) to offset fiscal consolidation. It has recognized that this advice needs to evolve.

5/

5/

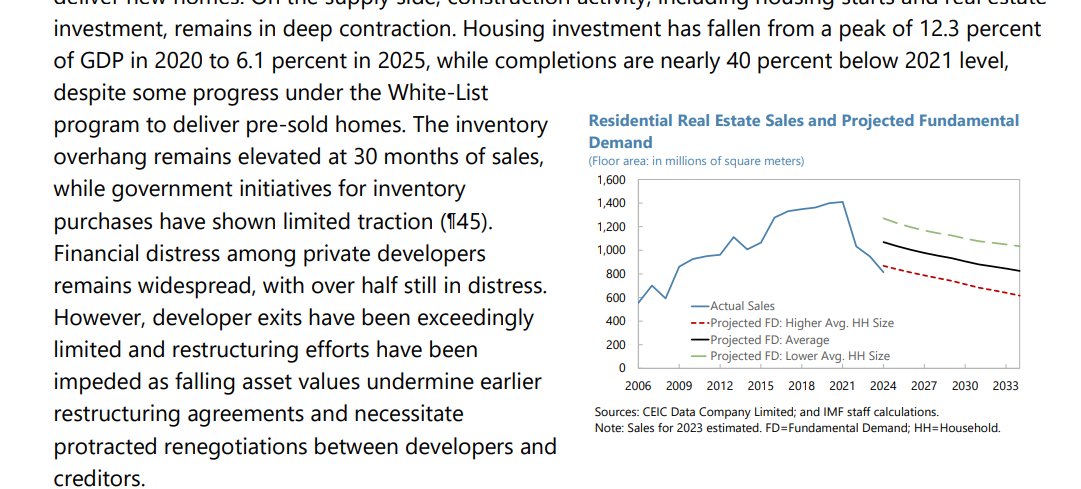

6

The IMF's analysis of the property sector and developer distress continues to be very strong

6/

6/

7

Paragraph 12 also effectively shows how LIMITED fiscal support for consumption has been --

7/

7/

8

And the IMF's recommendations for how China can do more to support consumption (and lower the insane rate of household savings) were on point. I particularly appreciated the renewed attention to the very regressive structure of taxation in China

8/

imf.org/en/news/articl…

8/

imf.org/en/news/articl…

9

The staff report also notes that the gap between China's current account norm and the reported current account surplus hsa widened, and thus the real exchange is not substantially undervalued (12-21%)

9/

imf.org/en/news/articl…

9/

imf.org/en/news/articl…

10

Those calculations were based on the Fund's expectation that the 2025 surplus would be 3.3% of GDP. The actual number was 3.7% of GDP (Q4 exceeded expectations) so Fund's methodology actually implies a bigger undervaluation than in the staff report

10/

bloomberg.com/news/articles/…

10/

bloomberg.com/news/articles/…

11

The Fund's argument around external imbalances though would be stronger if the IMF addressed some remaining gaps in its analysis, and if demonstrated a bit more expertise in China's balance of payments.

Let me highlight three gaps.

11/

Let me highlight three gaps.

11/

12

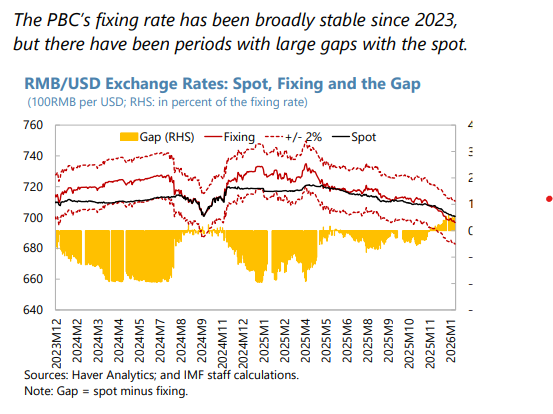

First, and most inexcusable, the IMF's analysis of China's exchange rate management remains thin -- this chart emphasizes the wrong variable (spot v the fix) and there is no analysis of the role of the state banks in fx management

12/

12/

13

If I were a part of the Treasury's fx/ China team I would be asking for a substantial raise, as the IMF's higher paid staff are FAR behind the Treasury in their analysis of exchange rate issues ...

13/

home.treasury.gov/news/press-rel…

13/

home.treasury.gov/news/press-rel…

14

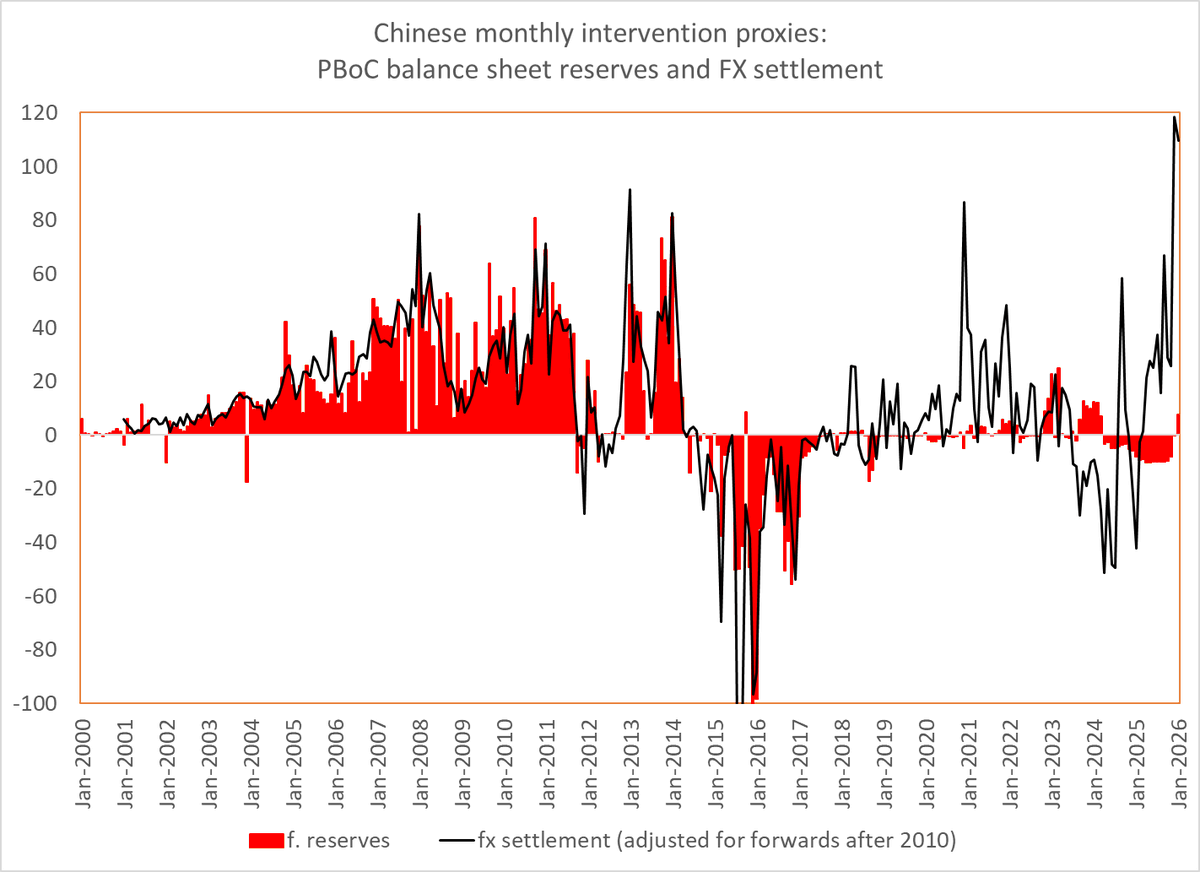

And with settlement now chalking in at $100b a month (give or take), it is just isn't plausible to ignore backdoor intervention. More generally, the Fund needs to recognize that China can and does target the exchange; it isn't just a derivative of monetary policy

14/

14/

15

Second, the Fund in no way hinted that China's reported current account surplus is understated, and that it would be substantially larger if China used its pre-2022 balance of payments methodology and had a plausible investment income line

15/

15/

16

Saying that China's reported BoP goods number (after the 2022 methodology change) is "adequate for surveillance" lets China off the hook, and basically gives a China a free pass for data changes that wiped a percentage point off the reported CA surplus

16/

16/

17

Third, the IMF continues to get an F at current account forecasting. China's current account surplus is not poised to fall in 2026 & 2027

17/

("the trade surplus is projected to contract, with the current account surplus declining from a projected 3.3 percent of GDP in 2025 to 2.8 percent of GDP by 2027. Over the medium term, the current account surplus is projected to gradually decline to around 2 percent of GDP")

17/

("the trade surplus is projected to contract, with the current account surplus declining from a projected 3.3 percent of GDP in 2025 to 2.8 percent of GDP by 2027. Over the medium term, the current account surplus is projected to gradually decline to around 2 percent of GDP")

18

I hardly know where to begin with all the things that are wrong with this forecast. It is clearly at odds with the 4.5% of GDP surplus in q4, which led Goldman to increase its 2026 surplus ... It is also at odds with the IMF's growth forecast

18/

18/

19

To state the obvious, the IMF cannot simultaneously forecast that net exports will add a percentage point to China's growth over the next two years and also forecast that the external surplus will fall by a half a point

19/

19/

20

The reduction in the current account surplus is also at odds with the depreciation in the real effective exchange rate in 2025 (which will impact the 26 and 27 numbers) and the quite undervalued level of the RMB

20/

20/

21

And there is nothing in the IMF's underlying analysis that suggests a cyclical recovery in demand in the near-term -- the IMF, for example, clearly doesn't think the real estate downturn is over

21/

21/

22

And last I checked the IMF didn't think the current elevated level of manufacturing investment was sustainable, and also doesn't think China is doing enough to support household consumption/ reduce savings

22/

22/

23

And in fact the high frequency indicators of investment suggest a new cyclical downturn in investment in q4 --

23/

23/

24

Finally, there are some uber-technical factors (the surge in the foreign assets of the state banks, which are only consistent with low reported errors with a higher reported surplus) that point to a higher reported surplus in 2026

24/

24/

25

Bottom line is that the IMF's current account forecast is at odds with its overall message -- if the CA surplus will naturally fall under 2 percent of GDP without real exchange rate adjustment & without pro consumption policies, there is no urgent need for a new growth model

25/

25/

26

So a much improved staff report --

But the IMF still needs to go much further

And it is being let down, strangely, by weaknesses in its technical BoP work

26/26

imf.org/-/media/files/…

But the IMF still needs to go much further

And it is being let down, strangely, by weaknesses in its technical BoP work

26/26

imf.org/-/media/files/…

27

Tweet 9 should be the exchange rate is NOW substantially undervalued; hopefully clear in context