@rohanpaul_ai: ARK Invest just released 2026 ...

@rohanpaul_ai

115 views

Jan 27, 2026

1

ARK Invest just released 2026 big ideas: The great acceleration and AI.

Global markets are entering an unprecedented phase of technology funding.

- Data center systems investment could reach ~$1.4T by 2030 as inference costs collapse >99% and API demand surges.

- Nvidia leads large model throughput, AMD and Google rival it for small models, and custom ASICs should keep gaining share.

- Foundation models are becoming a consumer operating system, moving interactions to agents that plan, compare, and transact.

- Purchasing agents compress checkout to ~90 seconds and could mediate ~25% of online spend by 2030.

- AI search may reach 65% of queries by 2030 and push ad budgets toward AI interfaces.

- Companies recoup the cost of an AI subscription in about 0.5 day, then as those tools boost output, total software spending could grow to $3.4T to $13T.

Example, if a $30 per user tool saves 1 hour worth $60 on day 1, it has paid for itself. Over a month, the extra saved hours justify buying more AI apps.

- AI plus multiomics could cut drug development to ~8 years (instead of the usual ~12 to 15 years.) with ~4x lower costs and enable high value cures, including a ~$2.8T US TAM for ASCVD.

- Reusable rockets are driving launch costs toward <$100 per kg, expanding satellite connectivity, and opening a path to space AI compute (pages 80 to 82).

- Robotics, distributed energy, robotaxis, and autonomous logistics will lower transport, power, and delivery costs at global scale.

Global markets are entering an unprecedented phase of technology funding.

- Data center systems investment could reach ~$1.4T by 2030 as inference costs collapse >99% and API demand surges.

- Nvidia leads large model throughput, AMD and Google rival it for small models, and custom ASICs should keep gaining share.

- Foundation models are becoming a consumer operating system, moving interactions to agents that plan, compare, and transact.

- Purchasing agents compress checkout to ~90 seconds and could mediate ~25% of online spend by 2030.

- AI search may reach 65% of queries by 2030 and push ad budgets toward AI interfaces.

- Companies recoup the cost of an AI subscription in about 0.5 day, then as those tools boost output, total software spending could grow to $3.4T to $13T.

Example, if a $30 per user tool saves 1 hour worth $60 on day 1, it has paid for itself. Over a month, the extra saved hours justify buying more AI apps.

- AI plus multiomics could cut drug development to ~8 years (instead of the usual ~12 to 15 years.) with ~4x lower costs and enable high value cures, including a ~$2.8T US TAM for ASCVD.

- Reusable rockets are driving launch costs toward <$100 per kg, expanding satellite connectivity, and opening a path to space AI compute (pages 80 to 82).

- Robotics, distributed energy, robotaxis, and autonomous logistics will lower transport, power, and delivery costs at global scale.

2

A household humanoid robot could add ~$62,000 to GDP each year by converting unpaid chores into market activity and freeing time for paid work, net of costs.

At 90M homes, impact approaches ~$6T, lifting US GDP growth toward 5%–6%.

At 90M homes, impact approaches ~$6T, lifting US GDP growth toward 5%–6%.

3

Past tech shifts raised long run GDP growth, and ARK expects another step up this decade with AI.

They argue new capital in robotaxis, AI data centers, and enterprise AI agents could add about 1.9 percentage points to annual real growth.

By 2030, ARK forecasts global real GDP growth near 7.3%, versus IMF at 3.1%.

They argue new capital in robotaxis, AI data centers, and enterprise AI agents could add about 1.9 percentage points to annual real growth.

By 2030, ARK forecasts global real GDP growth near 7.3%, versus IMF at 3.1%.

4

Quantum’s progress is too slow to be disruptive soon, per ARK

Even with faster scaling, cracking RSA-2048 and hitting compelling economics likely waits until the 2040s to 2060s.

Qubit counts and error rates would need to double and drop every 2 to 4 years, today’s pace is roughly every 4 years, so useful impact is decades out.

Even with faster scaling, cracking RSA-2048 and hitting compelling economics likely waits until the 2040s to 2060s.

Qubit counts and error rates would need to double and drop every 2 to 4 years, today’s pace is roughly every 4 years, so useful impact is decades out.

5

Inference price for strong models fell >99% from about $30 per 1M tokens in late 2024 to about $0.10 by mid 2025, with multiple releases pushing costs down each month.

As costs collapsed, usage exploded. Tokens served on OpenRouter rose roughly 25x from Dec 2024 to Jan 2026, showing surging developer and enterprise demand.

As costs collapsed, usage exploded. Tokens served on OpenRouter rose roughly 25x from Dec 2024 to Jan 2026, showing surging developer and enterprise demand.

6

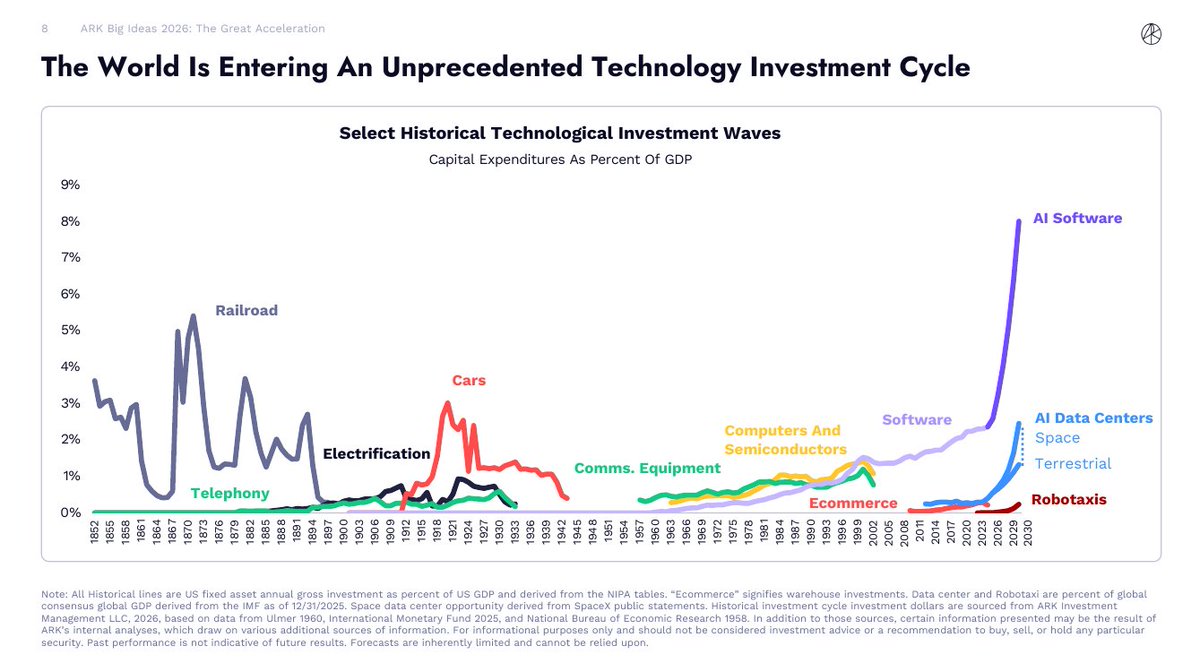

Data center systems spending inflected after late 2022 i.e. after ChatGPT moment.

Annual investment reached ~$500B in 2025, nearly 2.5x the 2012–2023 average, and growth accelerated from a 5% CAGR to 29% CAGR.

ARK expects this curve to continue, with investment potentially tripling to ~$1.4T by 2030 as AI demand drives more buildout.

Annual investment reached ~$500B in 2025, nearly 2.5x the 2012–2023 average, and growth accelerated from a 5% CAGR to 29% CAGR.

ARK expects this curve to continue, with investment potentially tripling to ~$1.4T by 2030 as AI demand drives more buildout.

7

Hyperscalers are set to spend >$500B on capex in 2026, nearly 3x 2021, pushing tech and telecom capex as % of GDP to highs not seen since 1998.

Unlike the dot-com era, valuations are far lower, the big tech cohort sits well below the late 1990s P/E peaks, so spending is elevated while multiples are restrained.

Unlike the dot-com era, valuations are far lower, the big tech cohort sits well below the late 1990s P/E peaks, so spending is elevated while multiples are restrained.

8

Nvidia absolutely leads large model inference, GB200 shows the highest tokens per TCO dollar (total cost of ownership.), while AMD lags on big models.

For small models, AMD MI355X delivers more tokens per TCO dollar than Nvidia B200, so cost efficiency favors AMD in that segment.

Ship dates and specs matter. Nvidia H200 and B200 shipped in 2024 to 2025, GB200 in 2025, AMD MI300 in 2023, MI355 in 2025, MI455 in 2026, TPU v7 in 2025. Memory ranges 141GB to 432GB, power 700W to 1400W, and hourly costs span ~$1.13 to ~$2.21, with TPU v7 near ~$1.28.

For small models, AMD MI355X delivers more tokens per TCO dollar than Nvidia B200, so cost efficiency favors AMD in that segment.

Ship dates and specs matter. Nvidia H200 and B200 shipped in 2024 to 2025, GB200 in 2025, AMD MI300 in 2023, MI355 in 2025, MI455 in 2026, TPU v7 in 2025. Memory ranges 141GB to 432GB, power 700W to 1400W, and hourly costs span ~$1.13 to ~$2.21, with TPU v7 near ~$1.28.

9

AI workloads are pushing data center investment toward ~$1.4T by 2030, growing ~30% CAGR, with compute the largest slice and networking plus storage rising alongside.

Server mix shifting from traditional CPUs to accelerators, GPUs dominate near term then ASICs take growing share by 2030 as large buyers seek lower cost per inference.

Server mix shifting from traditional CPUs to accelerators, GPUs dominate near term then ASICs take growing share by 2030 as large buyers seek lower cost per inference.

10

AI agents are becoming the primary interface, so users rely less on individual apps and more on goal based prompts.

Adoption is much faster than the early internet, AI chatbot penetration among smartphone users reached ~18% by year 3 versus PCs at ~3% in their year 3.

This marks a shift from command, to web, to mobile, to an agentic era.

Adoption is much faster than the early internet, AI chatbot penetration among smartphone users reached ~18% by year 3 versus PCs at ~3% in their year 3.

This marks a shift from command, to web, to mobile, to an agentic era.

11

AI purchasing agents are compressing the funnel of Consumer Transactions by doing discovery, comparison, and decisioning upfront, so shoppers arrive at checkout already convinced.

Personalization becomeing the moat because 95% of the journey happens before the click.

Transaction time fell from ~60 minutes pre-internet to ~90 seconds in the agentic era, so purchase velocity and conversion rates rise while ad wastes shrink.

Personalization becomeing the moat because 95% of the journey happens before the click.

Transaction time fell from ~60 minutes pre-internet to ~90 seconds in the agentic era, so purchase velocity and conversion rates rise while ad wastes shrink.

12

Agent protocols are standardizing how AI agents are accessing data and executing purchases across retailers, so messy one off integrations are giving way to a clean agentic stack.

Anthropic’s MCP is enabling agents to pull real time context, and OpenAI’s ACP plus Google’s A2A and AP2 are enabling secure payments, fulfillment, and transaction execution.

Retailers are exposing back end systems through APIs, an agentic AI layer is brokering context and settlement, and consumer interfaces are shifting to voice, chat, and wearables, so digital commerce is becoming simpler and faster.

Anthropic’s MCP is enabling agents to pull real time context, and OpenAI’s ACP plus Google’s A2A and AP2 are enabling secure payments, fulfillment, and transaction execution.

Retailers are exposing back end systems through APIs, an agentic AI layer is brokering context and settlement, and consumer interfaces are shifting to voice, chat, and wearables, so digital commerce is becoming simpler and faster.

13

AI agents are scanning catalogs, videos, and reviews continuously, surfacing in spec items without keyword hunting.

They are comparing attributes across sellers, filtering counterfeits, clustering reviews by theme, and simulating price plus promotion combos based on a user’s budget and preferences.

They are completing checkout with saved payments and tracking, so AI facilitated online spend is rising from ~2% in 2025 to ~25% by 2030, or >$8T.

They are comparing attributes across sellers, filtering counterfeits, clustering reviews by theme, and simulating price plus promotion combos based on a user’s budget and preferences.

They are completing checkout with saved payments and tracking, so AI facilitated online spend is rising from ~2% in 2025 to ~25% by 2030, or >$8T.

14

AI search is rising from ~10% of global queries in 2025 to ~65% by 2030, so traditional search is losing share.

Advertisers are shifting budgets, AI search ad spend is growing at ~50% per year and is reaching roughly $200B by 2030 with overall search ads still expanding.

Monetization is following usage with an estimated ~2 year lag, so revenue mix is tilting toward AI results.

Advertisers are shifting budgets, AI search ad spend is growing at ~50% per year and is reaching roughly $200B by 2030 with overall search ads still expanding.

Monetization is following usage with an estimated ~2 year lag, so revenue mix is tilting toward AI results.

15

AI mediated consumer revenue is growing ~105% per year from ~$20B in 2025 and is reaching ~$900B in 2030.

Lead generation and advertising are contributing most of the growth, subscriptions are staying smaller.

AI agents are transforming digital commerce and are directing spend toward ad and lead flows that they are controlling.

Lead generation and advertising are contributing most of the growth, subscriptions are staying smaller.

AI agents are transforming digital commerce and are directing spend toward ad and lead flows that they are controlling.

16

Models are gaining reasoning, tool use, and context, so agents are reliably completing longer tasks, rising from 6 minutes to 31 minutes during 2025 at 80% success.

Workers are reporting ~50 minutes saved per day, which is valuing at ~$47 using a $56.5 hourly wage, so a $20 monthly subscription is paying back in ~0.5 day.

Workers are reporting ~50 minutes saved per day, which is valuing at ~$47 using a $56.5 hourly wage, so a $20 monthly subscription is paying back in ~0.5 day.

17

Costs for capable models are collapsing across domains, often falling 90% to 99% on major benchmarks.

Software development with strong coding models is dropping from ~$3.50 to ~$0.32 per 1M tokens between Apr 2025 and Dec 2025.

Newer reasoning models like DeepSeek V3.2 are pushing blended costs toward ~$0.32 per 1M tokens, so teams are scaling usage without blowing budgets.

Software development with strong coding models is dropping from ~$3.50 to ~$0.32 per 1M tokens between Apr 2025 and Dec 2025.

Newer reasoning models like DeepSeek V3.2 are pushing blended costs toward ~$0.32 per 1M tokens, so teams are scaling usage without blowing budgets.

18

US frontier models are maintaining a roughly 6 month lead in capability, while China is catching up fast and is dominating open weight releases.

TSMC is producing far more advanced chips each day, about 135B transistors, while China's SMIC is producing about 3.5B, so capacity is about 38x larger on TSMC’s side.

meaning US aligned firms are getting supply first, since TSMC is fabricating the newest nodes at volume, so hardware scarcity is hurting China more.

In practice, that 38x edge is compounding, because more compute is creating better models, better models are attracting more users and money, and more money is buying even more TSMC capacity.

So China will need much more access to cutting edge compute to close the remaining gap.

TSMC is producing far more advanced chips each day, about 135B transistors, while China's SMIC is producing about 3.5B, so capacity is about 38x larger on TSMC’s side.

meaning US aligned firms are getting supply first, since TSMC is fabricating the newest nodes at volume, so hardware scarcity is hurting China more.

In practice, that 38x edge is compounding, because more compute is creating better models, better models are attracting more users and money, and more money is buying even more TSMC capacity.

So China will need much more access to cutting edge compute to close the remaining gap.

19

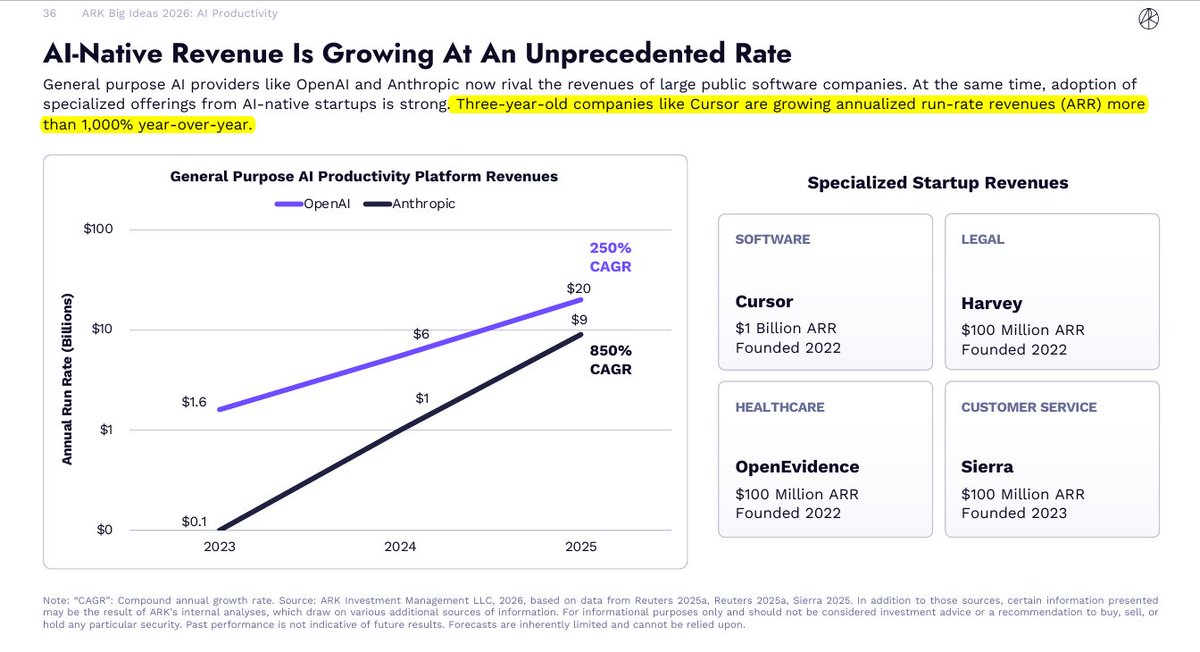

OpenAI and Anthropic are scaling revenues to levels rivaling large software firms, with implied 2025 run rates near $20B and $9B.

AI native startups are exploding, companies like Cursor, Harvey, OpenEvidence, and Sierra are hitting $100M to $1B ARR within ~2 to 3 years, and some are growing >1,000% year over year, showing demand is accelerating across verticals.

AI native startups are exploding, companies like Cursor, Harvey, OpenEvidence, and Sierra are hitting $100M to $1B ARR within ~2 to 3 years, and some are growing >1,000% year over year, showing demand is accelerating across verticals.

20

Software’s share of spend is rising as AI is augmenting knowledge workers.

Under modest adoption, global software spend will grow to ~$3.4T at 19% CAGR, unlocking ~$22T in surplus while employment is growing 6.3%.

Under accelerated adoption, spend will reach ~$7T at 37% CAGR, unlocking ~$57T, with more automation and some hour reduction.

Under rapid mass adoption, spend will reach ~$13T at 56% CAGR, unlocking ~$117T, with 81% of tasks automating and average hours dropping 20%, while long term unemployment is not rising.

Under modest adoption, global software spend will grow to ~$3.4T at 19% CAGR, unlocking ~$22T in surplus while employment is growing 6.3%.

Under accelerated adoption, spend will reach ~$7T at 37% CAGR, unlocking ~$57T, with more automation and some hour reduction.

Under rapid mass adoption, spend will reach ~$13T at 56% CAGR, unlocking ~$117T, with 81% of tasks automating and average hours dropping 20%, while long term unemployment is not rising.

21

Multiomics tools are cutting DNA read costs ~10x and are generating more data, so AI models are improving faster and are guiding better experiments.

Multiomics is integration of DNA, RNA, proteins, cells, and clinical data, powering AI driven discovery and diagnostics.

AI diagnostics are increasing data volume ~10x and are raising AI enabled test adoption ~5x, so patients are being identified earlier and more precisely.

AI drug design is shortening time to market ~1.6x and is cutting development cost ~4x, so smaller diseases are becoming economical to treat.

Cures targeting root causes are carrying ~20x the value of standard care and ~2.4x best in class precision drugs, so the flywheel is compounding by 2030.

Multiomics is integration of DNA, RNA, proteins, cells, and clinical data, powering AI driven discovery and diagnostics.

AI diagnostics are increasing data volume ~10x and are raising AI enabled test adoption ~5x, so patients are being identified earlier and more precisely.

AI drug design is shortening time to market ~1.6x and is cutting development cost ~4x, so smaller diseases are becoming economical to treat.

Cures targeting root causes are carrying ~20x the value of standard care and ~2.4x best in class precision drugs, so the flywheel is compounding by 2030.

22

Sequencing and multiomics test costs are collapsing, so far more data is becoming affordable.

By 2030, whole genome sequencing will drop roughly 10x to about $10, and other modalities are showing similar step downs.

Lower costs are enabling richer datasets, so diagnostic precision is improving.

By 2030, whole genome sequencing will drop roughly 10x to about $10, and other modalities are showing similar step downs.

Lower costs are enabling richer datasets, so diagnostic precision is improving.

23

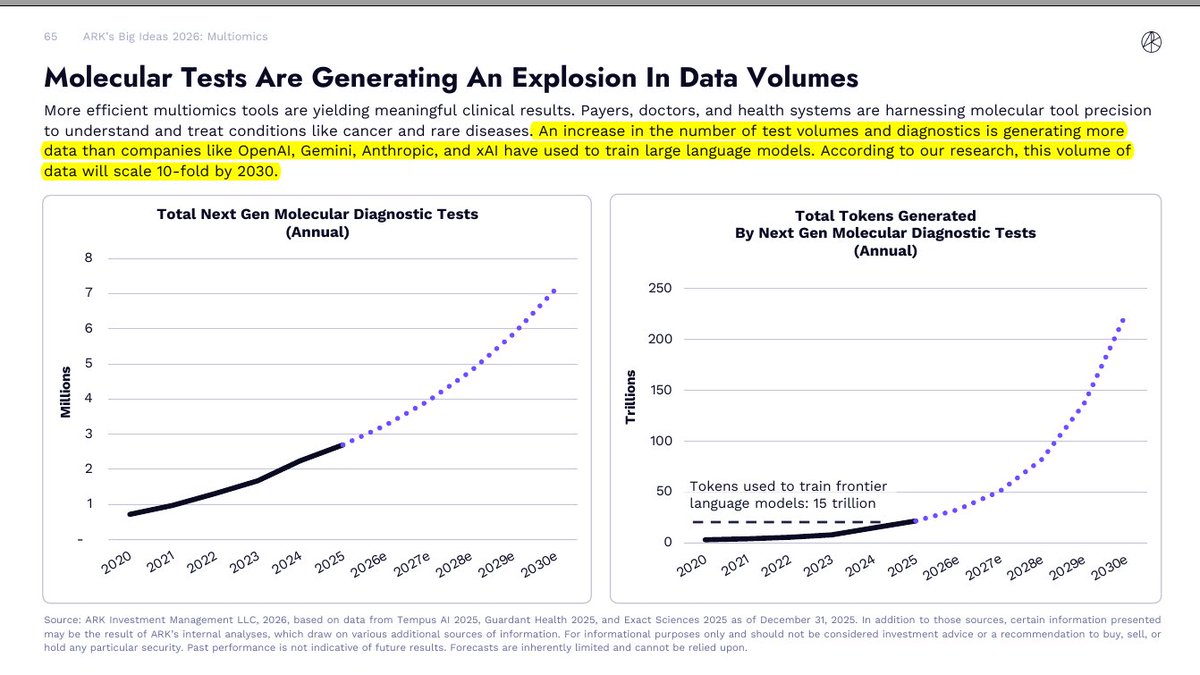

Molecular diagnostics are scaling rapidly, so annual next gen test volumes are rising from ~2M to ~7M by 2030.

Those tests are generating trillions of biological “tokens,” and by late decade they are exceeding the ~15T tokens used to train frontier LLMs.

This exploding data supply is feeding AI models, so precision and discovery are improving faster.

Those tests are generating trillions of biological “tokens,” and by late decade they are exceeding the ~15T tokens used to train frontier LLMs.

This exploding data supply is feeding AI models, so precision and discovery are improving faster.

24

AI enabled diagnostics are rising from near 0% of FDA approvals to ~10% after 2022, then are trending toward ~30% by 2030.

Big data and better models are lifting success rates for AI powered tests and devices, so more submissions are clearing.

Examples like Tempus AI’s ECG AF are identifying high risk patients earlier, so intervention is scaling.

Big data and better models are lifting success rates for AI powered tests and devices, so more submissions are clearing.

Examples like Tempus AI’s ECG AF are identifying high risk patients earlier, so intervention is scaling.

25

AI is reshaping drug R&D economics by cutting failures earlier and speeding decisions across target discovery, preclinical, and trials.

Today’s drug-development industry is spending about $2.4B per drug over ~13 years, and is averaging ~7.6 failed human trials along the way.

Early AI programs are already lowering waste, they are spending about $1.7B per drug over ~11 years, and are averaging ~3.2 failed trials.

AI is cutting failures earlier by finding better targets, selecting better patients, and stopping weak drugs sooner, so timelines are shortening and capital at risk is dropping.

Future AI driven design is targeting ~$0.7B total cost, ~8 years to market, and ~1.9 failures, so capital needs are shrinking and success odds are rising.

Today’s drug-development industry is spending about $2.4B per drug over ~13 years, and is averaging ~7.6 failed human trials along the way.

Early AI programs are already lowering waste, they are spending about $1.7B per drug over ~11 years, and are averaging ~3.2 failed trials.

AI is cutting failures earlier by finding better targets, selecting better patients, and stopping weak drugs sooner, so timelines are shortening and capital at risk is dropping.

Future AI driven design is targeting ~$0.7B total cost, ~8 years to market, and ~1.9 failures, so capital needs are shrinking and success odds are rising.

26

AI designed drugs are reaching market sooner, so more patent years are remaining at launch and cash flow is compounding longer.

Current AI methods are accelerating time to market by 2 to 3 years, lifting IP value by 30% to 50%, while emerging methods are targeting 4 to 5 years faster and 70% to 80% higher IP value.

Over 30 years, an average AI designed drug is generating about $4B cumulative cash flow versus about $1B for a traditional drug, and is crossing breakeven sooner.

Current AI methods are accelerating time to market by 2 to 3 years, lifting IP value by 30% to 50%, while emerging methods are targeting 4 to 5 years faster and 70% to 80% higher IP value.

Over 30 years, an average AI designed drug is generating about $4B cumulative cash flow versus about $1B for a traditional drug, and is crossing breakeven sooner.

27

Companies are pricing one time cures high and are generating more revenue than chronic drugs.

Patients or payers are paying once, often via insurers or government programs, not paying small amounts for years.

Cures are front loading revenue on dose 1, avoiding years of competition and adherence risk, and are capturing lifetime value upfront.

Because cash is arriving upfront and patents are still long, the modeled value to the company is jumping, about 20x vs a typical drug and about 2.4x vs a chronic treatment for the same disease.

For consumers, the promise is fewer ongoing bills and better health, but the single invoice is large and is usually handled by payers, outcomes contracts, or financing.

Patients or payers are paying once, often via insurers or government programs, not paying small amounts for years.

Cures are front loading revenue on dose 1, avoiding years of competition and adherence risk, and are capturing lifetime value upfront.

Because cash is arriving upfront and patents are still long, the modeled value to the company is jumping, about 20x vs a typical drug and about 2.4x vs a chronic treatment for the same disease.

For consumers, the promise is fewer ongoing bills and better health, but the single invoice is large and is usually handled by payers, outcomes contracts, or financing.

28

They are saying a one time heart risk fix is pricing around $165,000 per person.

They are counting about 17mn Americans who are still having high bad cholesterol.

multiplying those two numbers and you get about $2.8T of possible sales in the US.

They are comparing it to Lipitor and are saying this market is about 12x bigger.

They are counting about 17mn Americans who are still having high bad cholesterol.

multiplying those two numbers and you get about $2.8T of possible sales in the US.

They are comparing it to Lipitor and are saying this market is about 12x bigger.

29

Returns are improving when AI and cures are combining.

Traditional drugs are barely covering capital until late stages, so early assets are carrying low value.

When teams are cutting time to market and failures with AI, asset value at each stage is rising.

When the product is a cure, returns are jumping hugely with AI.

For a typical drug just starting Phase 1, expected value is near $0 because the chance of success is low and costs ahead are high.

For a cure that AI is accelerating, they are assigning much higher odds and faster timelines, so investors are valuing it around $2.3B to $2.5B at Phase 1.

Traditional drugs are barely covering capital until late stages, so early assets are carrying low value.

When teams are cutting time to market and failures with AI, asset value at each stage is rising.

When the product is a cure, returns are jumping hugely with AI.

For a typical drug just starting Phase 1, expected value is near $0 because the chance of success is low and costs ahead are high.

For a cure that AI is accelerating, they are assigning much higher odds and faster timelines, so investors are valuing it around $2.3B to $2.5B at Phase 1.

30

Longevity is shifting from treating diseases to targeting aging itself.

Life expectancy has risen from ~46.5 years in 1950 to ~73 years in 2023, while most deaths are concentrating at older ages.

Measures of aging are evolving too, starting with simple vitals, moving to functional tests, then to DNA methylation clocks, proteomic clocks, and wearable based activity measures that are quantifying biological age.

By measuring aging more precisely, researchers are identifying earlier risks and are testing therapies that are slowing biological aging, so healthy lifespan is potentially extending further.

Life expectancy has risen from ~46.5 years in 1950 to ~73 years in 2023, while most deaths are concentrating at older ages.

Measures of aging are evolving too, starting with simple vitals, moving to functional tests, then to DNA methylation clocks, proteomic clocks, and wearable based activity measures that are quantifying biological age.

By measuring aging more precisely, researchers are identifying earlier risks and are testing therapies that are slowing biological aging, so healthy lifespan is potentially extending further.

31

Medicine targeting disease and aging is doubling America’s “healthy years,” not just adding years lived.

By putting a dollar value on each healthy year, the chart is showing a giant, ~$1.2 Quadrillion opportunity that is dwarfing today’s biotech market.

In short, health systems investing in delaying disease and disability are unlocking massive societal and economic value.

By putting a dollar value on each healthy year, the chart is showing a giant, ~$1.2 Quadrillion opportunity that is dwarfing today’s biotech market.

In short, health systems investing in delaying disease and disability are unlocking massive societal and economic value.

32

Reusable rockets are turning space into a high throughput transport system, not a rare event.

SpaceX is lifting annual mass to orbit to new highs, so total payload is exploding compared to the pre Starlink era.

Starlink satellites are dominating the sky, so SpaceX is accounting for ~66% of all active satellites and is accelerating space based services.

SpaceX is lifting annual mass to orbit to new highs, so total payload is exploding compared to the pre Starlink era.

Starlink satellites are dominating the sky, so SpaceX is accounting for ~66% of all active satellites and is accelerating space based services.

33

Rocket Launch costs are falling exponentially as reuse is scaling.

SpaceX is cutting cost from ~$15,600/kg in 2008 to under ~$1,000/kg, and Starship at scale is targeting <$100/kg.

Wright’s Law is applying, every doubling of mass to orbit is dropping cost by ~17%, so cheaper access is enabling many more space uses.

SpaceX is cutting cost from ~$15,600/kg in 2008 to under ~$1,000/kg, and Starship at scale is targeting <$100/kg.

Wright’s Law is applying, every doubling of mass to orbit is dropping cost by ~17%, so cheaper access is enabling many more space uses.

34

Cheaper, reusable launches are making mega constellations viable, so satellite internet capacity is scaling fast.

As bandwidth is rising toward tens of thousands of Tbps, annual satellite connectivity revenue is approaching ~$160B.

By 2035, satellite will contribute ~0.2% of global GDP communications spend, so space is becoming a meaningful part of telecom.

As bandwidth is rising toward tens of thousands of Tbps, annual satellite connectivity revenue is approaching ~$160B.

By 2035, satellite will contribute ~0.2% of global GDP communications spend, so space is becoming a meaningful part of telecom.

35

Technology is raising output per worker while people are working fewer hours.

Productivity is climbing, so each hour is becoming more valuable and living standards are continuing to rise.

Productivity is climbing, so each hour is becoming more valuable and living standards are continuing to rise.

36

Robot use is still early, even in heavy industries.

Amazon is showing what higher robot density looks like, it is running ~6,427 robots per 10,000 workers in 2025, while top automotive and manufacturing sectors are sitting around 1,100 to 1,500.

As robots are becoming more general and cheaper, other industries are following, creating new kinds of jobs alongside automation.

Amazon is showing what higher robot density looks like, it is running ~6,427 robots per 10,000 workers in 2025, while top automotive and manufacturing sectors are sitting around 1,100 to 1,500.

As robots are becoming more general and cheaper, other industries are following, creating new kinds of jobs alongside automation.

37

General purpose automation is unlocking a ~$26T annual market across factories and homes.

Manufacturing robots are scaling, and new platforms like quadrupeds and humanoids are beginning to spread beyond fixed tasks.

Robots are doubling labor productivity in manufacturing, yielding a ~$13T provider opportunity.

Unpaid household work, valuing a slice of that time, and projecting another ~$13T opportunity as home robots are taking chores.

Manufacturing robots are scaling, and new platforms like quadrupeds and humanoids are beginning to spread beyond fixed tasks.

Robots are doubling labor productivity in manufacturing, yielding a ~$13T provider opportunity.

Unpaid household work, valuing a slice of that time, and projecting another ~$13T opportunity as home robots are taking chores.