@gregoryblotnick: “Everyone has the brainpower t...

“Everyone has the brainpower to make money in stocks, not everyone has the stomach.” - Peter Lynch

This post is about sizing, but specifically, the mental hurdles and various forms of cognitive dissonance that get in the way of "correct" sizing. I initially wrote this as a thread 4-5 months ago, it was sloppy, I expanded on it over the weekend and added a lot of charts and examples for improved clarity.

"Riding a Multi-Year Winner in Size"

I first wrote a lot of this material down around 2019, and the best phrase I could come up with was “riding a multi-year winner in size” in terms of what historically generates the bulk of an investor's outperformance.

Go look at the greats, study how Buffett and Munger did it, and you’ll recognize the following patterns and principles:

Theoretical Support

Munger:

Buffett:

In Practice

Sizing and Evolution of L/S

What follows is strictly my personal opinion based on what I've seen since 2009. It is probably wrong.

The L/S industry has moved in a direction where this part of the game - big, chunky, multi-year winners - has become less and less relevant.

This wasn’t always the case. Decades ago (esp. pre-crisis) managers would take much bigger swings, these 15-20%+ position sizes where a manager's name and career would be attached to a single ticker. The most recent I can think of was something like VRX, or even the HLF fiasco before that.

People forget that the entire low-net market-neutral model which is now dominant, is mostly a post-crisis phenomenon, driven by institutional flows in search of equity returns with fixed-income volatility.

Now, you really don’t see single-managers taking those kinds of swings slash career-making position sizes...and at a pod, while “am I big enough in my best ideas” is a question being asked at all levels, the top-down risk constraints plus the other leg(s) of the trade will inevitably drag on P&L.

With that in mind, what is written here is mostly food for thought and to be evaluated standalone -- I suppose it applies best for individuals/personal accounts. I say food for thought because parts of it conflict with what I’ve written earlier on risk management and sell discipline... so you’re seeing me try and hold two opposing ideas simultaneously, with it being an ongoing effort to reconcile them in a way that yields repeatable/sustainable/consistent process.

Mental Capital Redux

“The key to investing is not how much IQ you have, but how you behave when you have capital to deploy. Can you wait? Can you focus?”

Buffett

Mental capital is EVERYTHING. It comes out in not just risk management (a function of discipline) but in sizing and pressing winners. Previously we discussed it in the context of drawdowns:

https://x.com/i/status/2004984420567318554

That's defense. It also applies for on offense.

Holding a 1% position for multiple years is not hard. It puts zero pressure on you emotionally, it has minimal effect on your mental capital.

But as Buffett & Munger repeatedly show... the game is about riding multi-year winners IN SIZE.

If you’re going to be right, BE RIGHT. Percentage gains don’t matter - dollar gains do.

This was something I wrote last summer, about how you really don't see position sizing discussed much on Twitter. You see a lot of % gain. That's not the formula, it's (position % gain * position size) = contribution to P&L:

Example math:

Choice A: (50% gain) * (5% position size) = +2.5% position contribution to P&L.

Choice B: (20% gain) * (20% position size) = +4.0% position contribution to P&L.

This is why to sit around discussing individual % gain is meaningless.

The rest of what's written there, I hope has played out in these articles...as you can tell from the phrasing of "functional but dynamic risk mgmt philosophy," and how uncertain I am on that topic, it's one that I'll never write about with confidence...and the "read more non-business material" theme is one that keeps resurfacing.

A lot of that third paragraph re: great performance coming from low-beta megacaps, I actually didn't understand until much later in my career. I don't think it clicked until I saw it in action at multis - the idea that a slow-moving megacap can be equivalent, but is actually preferred.

The main reason is that the amount of capital being moved was much larger ($1B+ GMV versus a $250M single-mgr book) and so liquidity matters a lot more.

You can get in and out of a mega-cap without too much trouble, but if your best ideas are sized at $50M to $100M, trading a $2B mid-cap now means you're anywhere from 2.5% to 5% of the total shares outstanding.

At a concentrated LO or "long-term" single-mgr L/S that's one thing, but given how short-term and trading-heavy multi-mgr L/S is, plus the frequency of forced unwinds/grossdowns/top-down capital cuts from risk, you're going to have huge problems in mkt caps that small.

Does any of that apply for the reader, doubtful, it's just a clarifying point on why this whole approach is for individuals/personal accounts and probably not applicable for most of the industry as it stands today.

Patience, Discipline, Pattern Recognition, Cognitive Errors

Holding a 20%+ position for years is where your mental capital, patience, and discipline are tested.

There's also a long list of hurdles and cognitive biases that prevent investors from making the “technically-correct” play. We’ll go over some of those here.

If you sit down and look over your lifetime P&L, you will realize the same thing I realized: that out of all the overtrading, across thousands of positions... probably 80% of your P&L came from like two, three, maybe five positions.

That 20-hole punchcard theory is real. Everything written below is totally anecdotal, but I recognize the same pattern across the few ideas which moved the needle for me.

First was months if not years of familiarity before putting $ at risk. Again, people forget with Buffett that he'll "stalk" a company for years or decades before putting a dollar into it - this is patience in action.I started researching "idea A” in 2011 but it took two years before I bought my first share. For “idea B,” I was assigned it as part of a job interview in 2014. I didn’t get the job, but later that year it sold off and I made it a 20%+ position.

Over the next few years, while I was internalizing all the Buffett/Munger mindset written above, these two positions in my PA ran to 30-40% of capital as they worked...I said “fk it” and pretty much blew out of all the other ones, eventually just ending up with two 40%+ positions, cash, and hedges. Arrogant, probably, I'm just trying to extract the few discernible pieces of "good process" for the purpose of this post.

Right or wrong, at the time, I felt like I was ready to punch a few holes of the 20-hole punchcard. In hindsight, what appears to be conviction can always just be written off as sheer luck, and I’m totally open to that.

If it was 2007, I would’ve got wiped out in 2008... but it was early 2016 and the market went bonkers for the next two years. Hence the origin of the phrase:

“Never confuse brains with a bull market."

Fundamental Conviction

Both times, the same pattern occurred:

A stock gaps up 10-20% to all-time highs... the chart is nearly parabolic on all time frames.

This random chart is a pretty good example of what that would look like on a 1-year basis:

Longer-term, it looks something like this (diff ticker/chart):

As this is happening, you update your model, you check your numbers again and again and again, and you come to the following conclusion:

“The stock is up 20% today, but earnings power just went up 40%.”

You have to trust your fundamental work, because without that, you’re basically nothing.

This is why I said in a former post, all the technicals, all the arcana and sentiment-based shit, there’s no conviction to be found there... fundamentals have to drive the bus. I think that sentiment was found in this one:

https://x.com/i/status/1999494474175504711

In situations like this one above, with the chart looking crazy to the upside, your fundamental work is telling you that even though the stock is up 20%, earnings power went up 40%, thus, the technically-correct play is: “Buy the piss out of the stock until it is up 40%.”

This could be viewed as an oversimplification but really isn't. Earnings power isn't just NTM ests; earnings power is the full DCF + terminal value considerations. So however you got to that 40% from your fundamental work, you would buy until (delta in stock price % = delta in earnings power %).

These situations are actually when you have some of the highest odds of finding a market inefficiency or mispricing. The reason is that markets are razor sharp when there’s “muscle memory,” but they have problems pricing things that have NEVER HAPPENED BEFORE.

This could be a new business segment, new product, or most recently something like NVDA and AI.

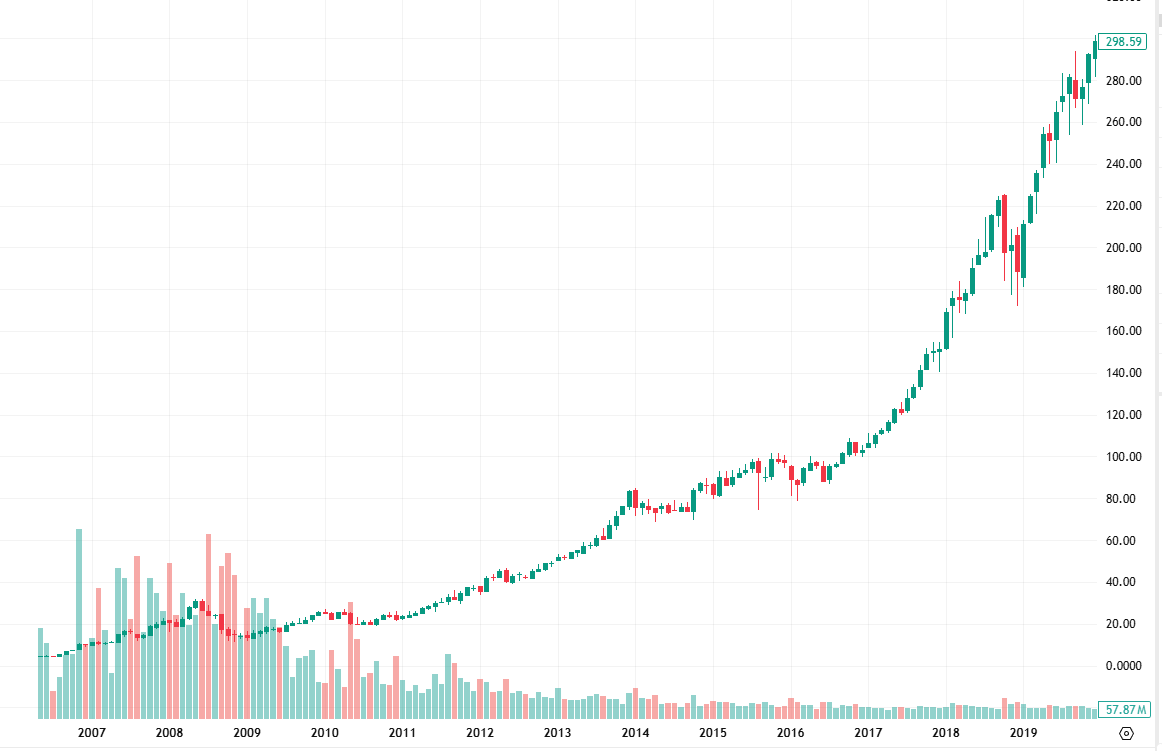

At the start of 2023 NVDA was a ~$14 stock, and despite being a widely-covered megacap, halfway through 2024 it was priced at $140 (last $186):

That's how markets can be inefficient at all levels. You're not supposed to have 18-month 10-baggers in a megacap. But when things happen that haven't happened before, markets have difficulty pricing it.

The cognitive dissonance is that a stock can go from $250 to $500, and be cheaper at $500 than it was at $250.

This is extremely important to understand so I'll move slowly.

A stock is at $100 and earns $10, for a 10x multiple.

Something changes, either secular like AI, or a new product or new segment, which boosts earnings power from $10 to $40.

The stock goes from $100 to $200.

However, even though the stock doubled, it's now cheaper than it was before.

$200 stock with $40 of earnings power = 5x multiple, down from 10x ($100 stock with $10 in earnings power).

The stock could then go from $500 to $1000, and be cheaper at $1000 than it was at $500 or even at $250. Without even looking at NVDA's estimates, something like this exact dynamic occured - I'm not a semis/TMT analyst.

However, without fundamental work, you'll never be able to "ride a multi-year winner in size." Everything will appear deceptive, the chart will look crazy. Example below - I truncated the NVDA chart so that it ends at the start of 2024:

You would have to be nuts to buy that chart. But over the next six months, it ran from $70 to $140....the people with fundamental conviction stepped in and bought, and "board man gets paid."

Other Mental Stumbling Blocks

The chart itself, parabolic, will trigger a reaction of “sell” (as with above).

This is one of the most common mental blocks. Great stocks are always making new all-time highs... the chart of a great stock is up-and-to-the-right over decades. Buying record highs was never the wrong call, every sale was technically a bad one, yet you see far more people trim than add when a new high prints.

As a random example, here's Mastercard (MA) over a 15-year timeframe - buying fresh highs consistently got you paid.

Next, the NTM multiple will appear deceptive, because it will ALWAYS look too high. This is because it’s based on numbers that are too low.

So for NVDA, again, I don't know what earnings looked like at the time, but when the stock ran from $14 to $140 over 18 months I guarantee that it looked expensive as hell the entire time on consensus numbers.

But without fundamental work, you’ll just see the chart going nuts and it will trigger an instinctual reaction of “sell.”

Social proof as a mental stumbling block: in justifying your process to others, if you were to tell someone “I’m buying/adding to XYZ here,” they’ll look at the chart and say “are you crazy??” You will be worried about how you’re perceived, a blind momo chaser or a cowboy with no risk discipline...I keep going back to this same tweet, but it applies here:

https://x.com/i/status/1991501300945830270

This is why “TRADE QUIETLY” is some of the best advice in trading...keep all that shit to yourself, don't tweet your positions, don't talk about your positions, all these things do is introduce "social proof" hurdles that can prevent you from making the technically-correct play.

Last, your P&L and sizing will look crazy. A 20%+ position that is working will end up being obnoxiously sized relative to all your other positions. You will probably violate some “max % of capital” guideline you laid out in advance.

If you had NVDA as a 10% position, and it runs from $10 to $70, the position will look absurd in a total portfolio context -- at close to 70% of capital.

What does this lead to? Non-fundamental selling...people trimming when their fundamental work says they should be PRESSING THEIR WINNERS.

Practicing Visualization

“The problem is that people who aren’t capable of rationally handling a concentrated portfolio think they are. That’s the danger.”

Munger

Do not underestimate how difficult it is to stick with a position like this on a daily basis for multiple years, or a four-stock, 25%-sized Munger-style portfolio.

Each day, you must resist the urge to take profits. The unrealized P&L attached to each position will grow as the positions work and keep printing new highs, begging you to ring the register.

Each day, the market will test you one way or the other. It doesn’t matter whether it’s red or green; your brain can fuck you up by forcing you into impulsive decisions on either color.

Both are driven not by fundamentals, but by fear.

The technically-correct decision is almost always DO NOTHING. Activity bias is real and overtrading consistently destroys P&L.

Additionally, as an investor, you will have hundreds of new ideas come across your desk over this time period. With each one you evaluate, you have to conclude “nope, the optimal portfolio is still the one I have, those four stocks.” This is hard because of shiny object syndrome where new ideas always seem more appealing than the ones you already have in the book.

If there is a broad correction, where your positions could drop 25-50%, the magnitude of the dollar losses is going to rattle you.

To continue with the NVDA example, after printing $140 in mid-2024, it retraced to $90, a drawdown of some 40%.

The challenge here is that a winning position will be sized at a level (in dollars) you aren’t accustomed to dealing with.

As total capital grows, the size of the dollar drawdowns grows with it.

The percentages don’t change, but your mind will play tricks on you as you start thinking about shit like “here’s what you can buy with that amount of money...that's a house, a car" etc.

These are NON-FUNDAMENTAL thought patterns + impulse triggers that can and will negatively impact your decision-making.

I have the same mental incongruence here as before, re: "technically-correct fundamental play" vs. process discipline, i.e. some ex ante position-level max drawdown or trailing stop framework. I don't know.

The lesson from all of this is the same: it’s not about the ideas. An idea isn't worth shit if you can’t execute on it, and your ability to execute is a function of PATIENCE AND DISCIPLINE.

You could have pitched NVDA to a billion people when it was at $14 and nailed the thesis. Most would have bought it, sold it at $20, locked in a respectable gain, and then missed the next 8-10 bags.

But that's what separates Buffett/Munger from the rest of us - the ability to RIDE A MULTI-YEAR WINNER IN SIZE.

This brings us back to the Peter Lynch quote that opened the article: "Everyone has the brainpower to make money in stocks, not everyone has the stomach.”

Everything written above is what Lynch means by “stomach.”

A single-digit position size requires no stomach. Once you hit 15-20%+ with the goal of “riding a multi-year winner in size,” that’s all stomach.

The only way to develop "stomach" is by putting capital at risk.

You don't learn shit like that from scrolling Twitter or even from reading books...or "model portfolios," or backtests, or "paper trading," none of that works. I'm not actively recommending this (most people should buy the index), but you have to actually try managing, in real-time, a 25-50 percent position through the entire life cycle of the trade. There is just no way to replicate the emotional impact without putting actual capital at risk.

You'll inevitably fuck it up a bunch of times and probably blow an account. After that, you'll humbly come to appreciate how wide the gap is between us mortals and the Buffett/Munger types, not just in terms of brainpower, but in temperament.

“If you want to avoid irrationality, it helps to understand the quirks in your own mental wiring and then you can take appropriate precautions.”

Munger

Conclusion

Once again, this post comes down to the same theme that runs through all the prior posts.

There is no right or wrong, what is "right" is what works for you, you have to KNOW YOURSELF to figure this out, and knowing yourself only comes from years of trading markets. Without self-mastery, no idea is worth a shit.

That's all I have to offer...the rest is up to you.

Hope this helps and good luck trading.

GB